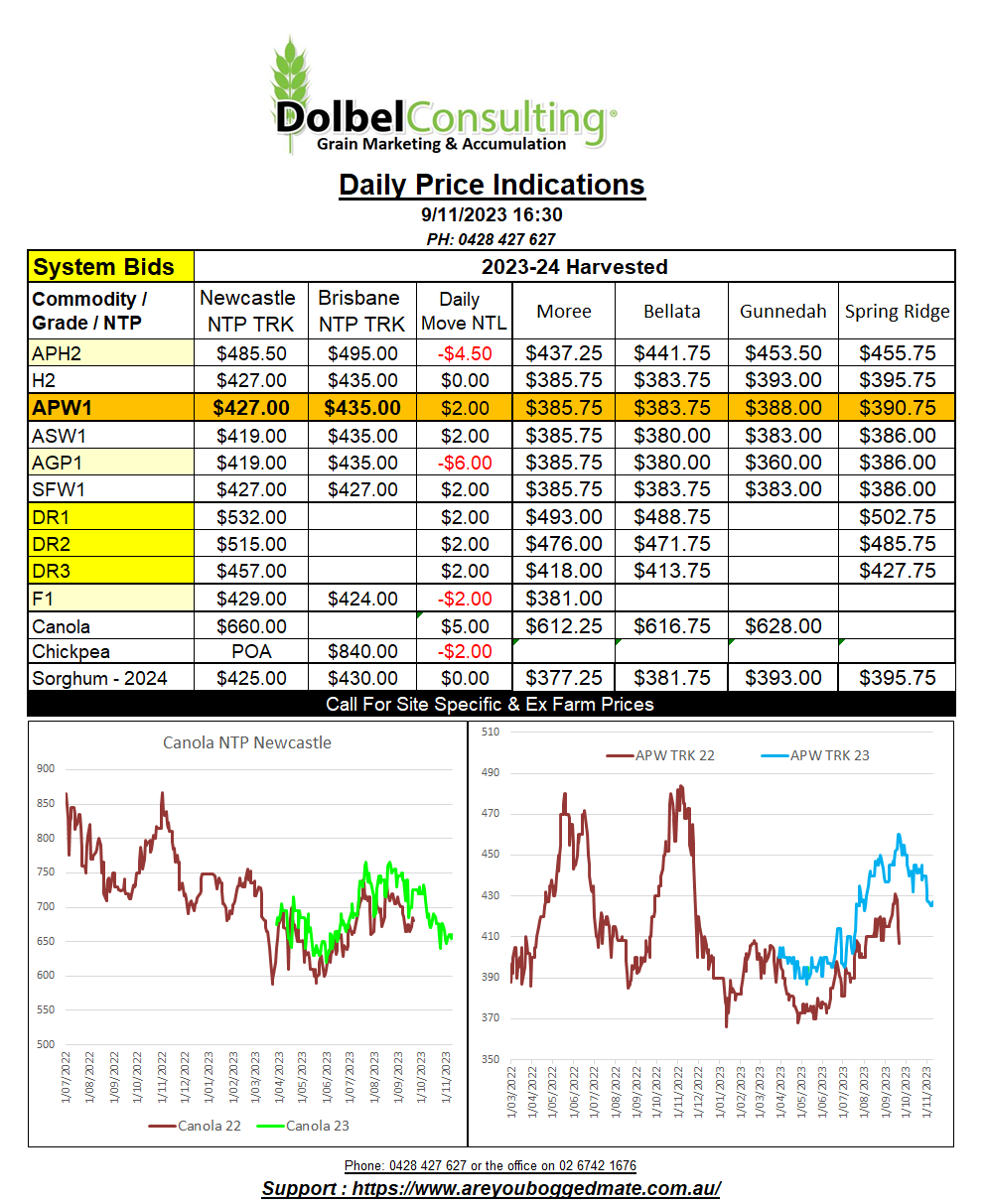

9/11/23 Prices

There’s a USDA WASDE report due out tonight. Futures trade in the states was mainly focused of technical trade and short covering, prior to the report. The punters continue to hold massive shorts in wheat and corn while also sustaining a long position in soybeans and soybean products.

The latest CFTC report, out on week old data, showed that Managed Money from the 31st of October had a net short in soft red wheat of 108,837 contracts, that’s roughly 14.8mt, another 4.5mt of HRWW and a massive 18.39mt of corn shorts.

At some stage these shorts will need to be rolled or covered. The raw numbers don’t really give a lot of useful data, like the months these positions are in and the rate of decline.

The stochastic chart for CME SRWW has shown a sharp decline from overbought to oversold over the last 8 sessions. Technically the wheat market at Chicago was due for the rally it had last night. If we can find some fundamental support from tonight’s USDA WASDE report we may well see more buying into the weekend. One would need to see some sustained upside to call this anything other than a dead cat bounce at this stage though. Possibly lower ending stocks and an uptick in US wheat exports would help.

Saudi Arabia picked up 710kt of wheat yesterday. The value ranged from a low of US$290.20 C&F to US$302.90 C&F. The greater number is roughly equivalent to about AUD$310 ex farm LPP. Well below current values bid locally and also below returns possible for Australian wheat into the Asian market. Local bids for H2 wheat for instance continue to make even NNSW wheat affordable to the Asian consumer. This may have an impact on the local S&D for wheat in N-NSW later in 2024, if exports are made from the Newcastle port zone. The Graincorp shipping stem shows no current export bookings for wheat out of Newcastle. The NAT stem report shows a wheat vessel with a dwt of 55kt heading to port to load next week.