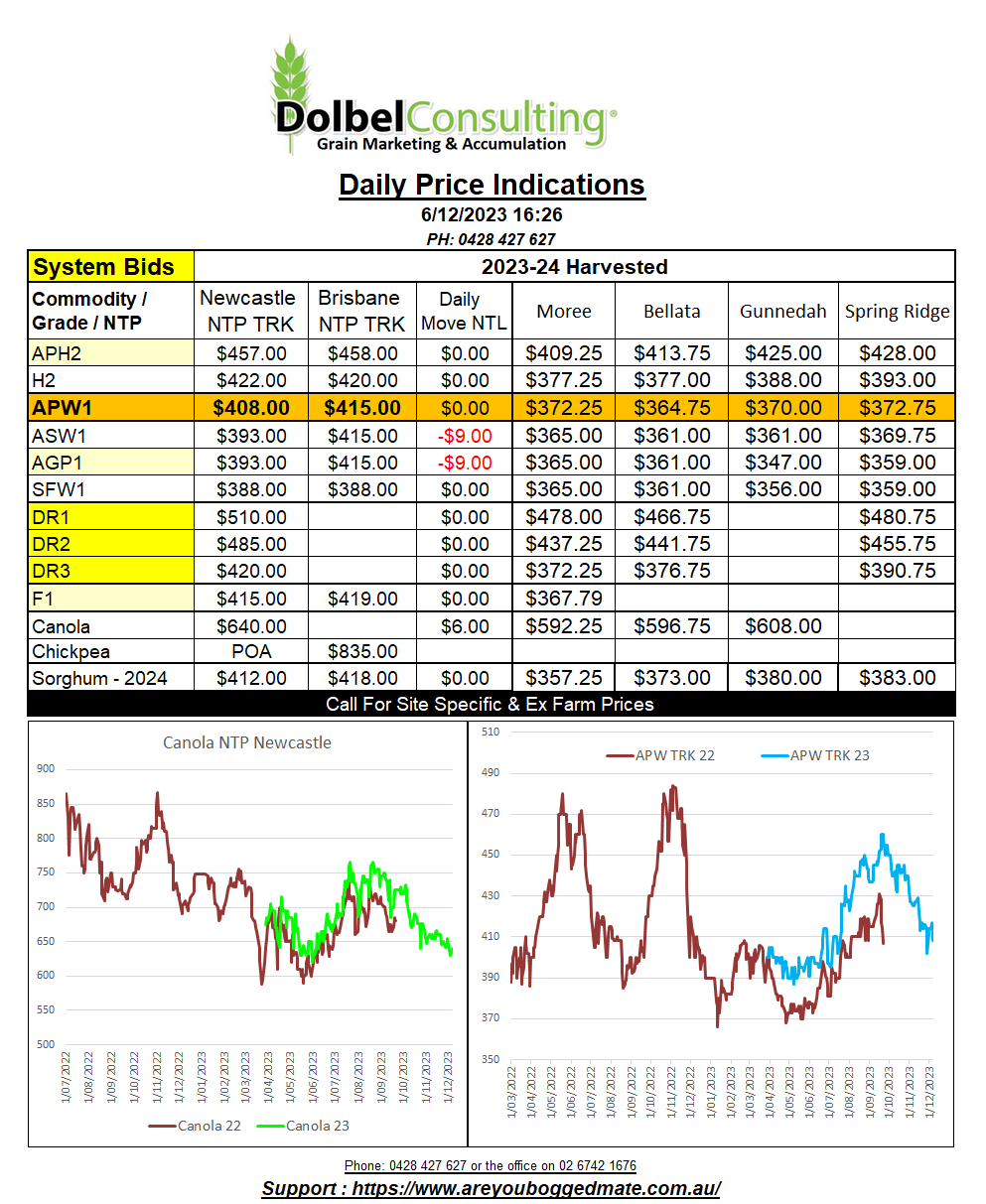

6/12/23 Prices

The Algerian tender for 50kt of durum was completed earlier this week. Algeria do not make public their tender results. The trade usually speculate on both value and actual tonnage booked over the following days once the tender closes. This tender is no different.

Initial reports had just 50kt being booked at values which one could consider a little cheap. Overnight more trade chatter has resulted in some more “details” coming to light. As speculative as they are the volume and values do appear more representative of the current durum market. The consensus now appears to be that there was about 500kt booked, 300kt of that being Canadian durum and the balance split between Mexico and Australia at values between US$435 and US$470 for a handimax.

The later value tends to ride well with local values, coming in about AUD$30 above current cash bids, that is usually about the margin we see here.

Still in the durum market, we now see Italian farmers getting local politicians on board to protest against cheap imports of Turkish, Russian and Black Sea durum wheat. There is even some talk of an anti-dumping case being commenced due to the difference in price between internal and external values in Turkey. I’m not across the laws surrounding EU imports / Turkish exports. Looks like horse is way over there and gate is…….well ……….. missing.

The combination of a weaker AUD, and higher US wheat futures and cash prices, should help export parity values for milling wheat today. The RBA kept local rates unchanged in their December meeting. Q3 GDP data is due out today and may have an influence on the AUD this afternoon. Local retail was back roughly 20% during Q3, I don’t know if that’s a national gauge or not but it was certainly ugly at a local level. The move in the AUD is worth just over AUD$3.00 for wheat. For canola it has turned a E0.50 decline in Paris futures into a plausible $3.13 improvement.