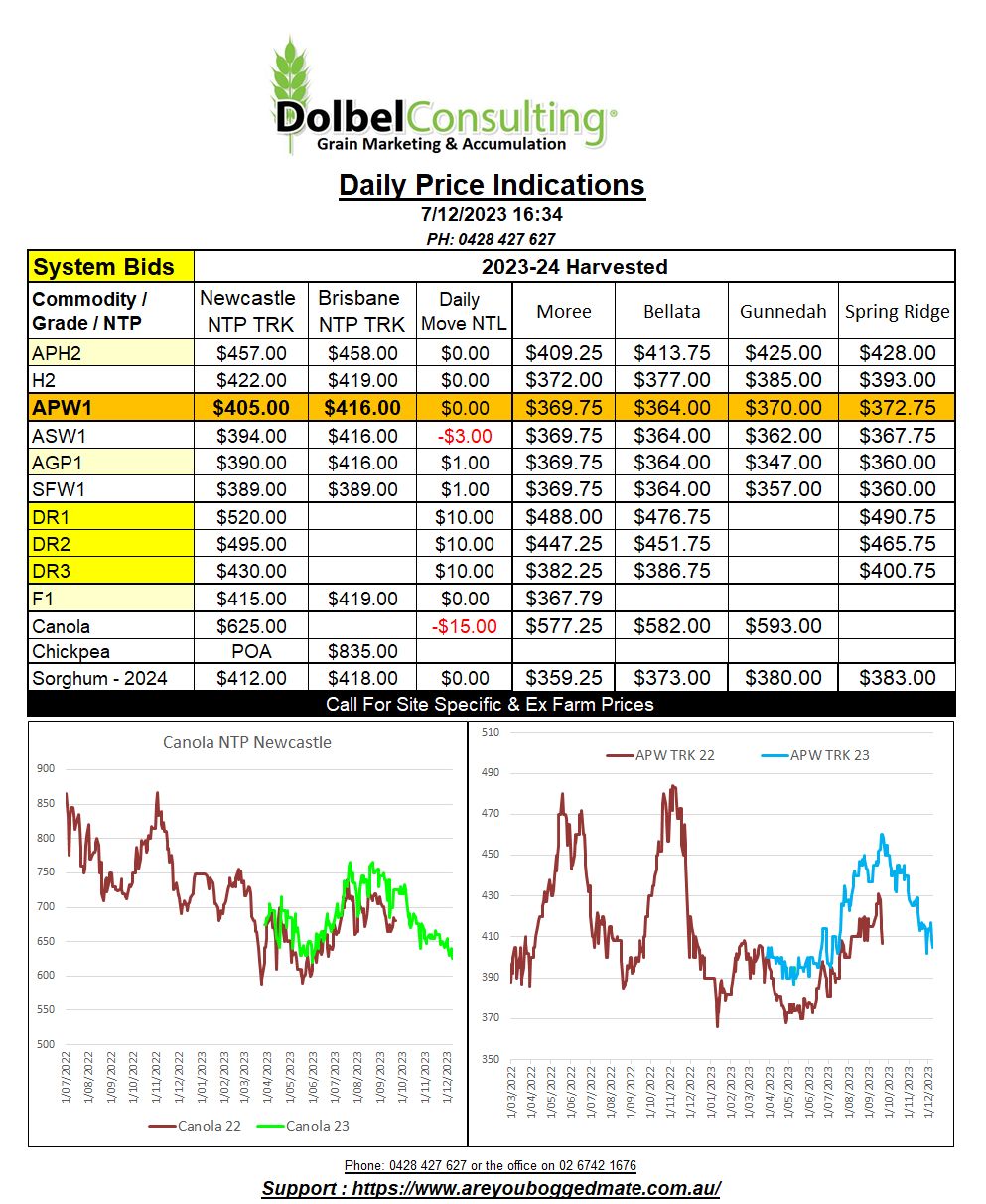

7/12/23 Prices

Paris and Winnipeg rapeseed / canola futures were hit pretty hard last night. The Paris contract, that the local markets here have generally been tracking a little more closely than the Canadian market, was back E8.75 on the nearby February contract. In day to day AUD terms this equates to roughly AUD$15.46 per tonne. With both Paris and Winnipeg lower, as well as Chicago soybeans, it’ll be hard to talk the local oilseed market higher today.

In spite of the rally in US wheat futures Paris milling wheat futures had been reluctant to follow the lead from Chicago. This changed last night with Paris milling wheat futures pushing E4.25 higher on the nearby December contract and E2.25 higher on the March contract. London feed wheat futures even managed to close a little higher across all months.

In the states Chicago, Kansas and Minneapolis wheat futures all took a breather, Chicago SRWW futures after 6 consecutive higher closes in a row.

The weakness in the global oil seeds market is coming from a lot of directions. The major force is probably improved weather in Brazil, this may at least stabilise the condition of their soybean crop short term. Production there is still estimated at a massive 150mt +/-. Another lower close in palm oil futures also weighed on the complex. Chicago beans, unable to fight off the weaker sentiment, also closed lower, back 11c/bu in the March contract.

A quick look around at global weather shows 10-25mm of rain across the Indian chickpea region. It’s actually a bit wetter than average there and this rain should help their crop significantly. During the week chickpea values at the Delhi market have slipped. The weaker AUD has countered this a little locally. The 14 day rainfall anomaly in Brazil, Mato Grosso, shows it’s still drier than average with about 40-60% of normal rain falling over the fortnight.