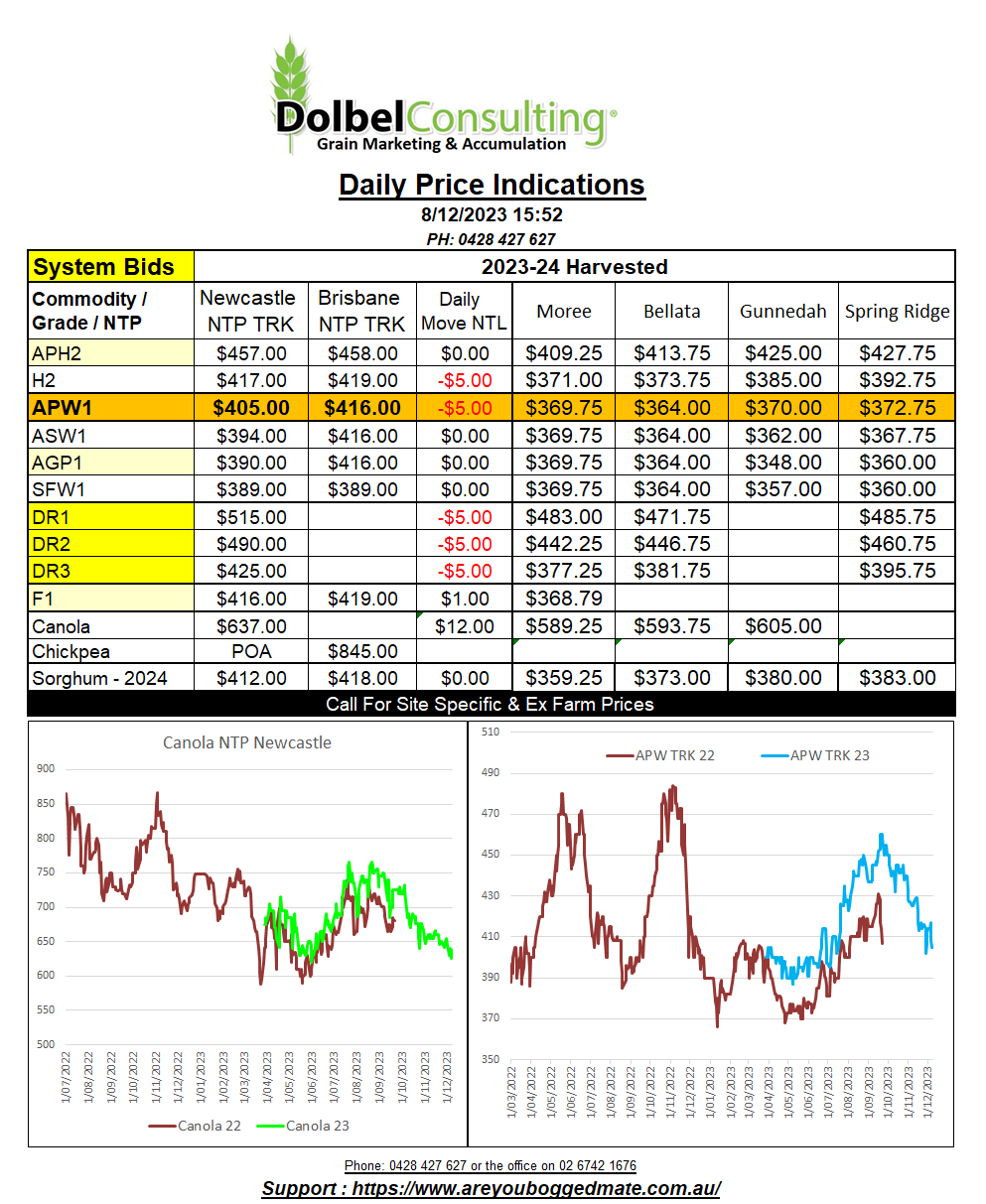

8/12/23 Prices

Am I watching the same trade “play book” being used in Argentina as I am here? Wheat values there have fallen since harvest started. Conditions there were poor for wheat production this year. Not a full drought crop, but not unlike the conditions experienced across NNSW and QLD. The trade seem to have placed sales while the prices were high, prior to harvest. Now grain is available prices have fallen. With some consumers removed from the equation as they are covered by the trade. Hand to mouth purchases from the trade and remaining consumers continue to see the softest seller set the price.

Argentine 12% protein wheat values have fallen roughly AUD$73, using spot currency, since the first of November. In NNSW we’ve also seen a weaker H2 market, during the same window shedding $10 ($29 since Oct 1st), so maybe we are a little lucky.

As for what the mid grade milling wheat is worth on the international market, using China as an end use point, we see that Argentine wheat is now at a C&F level China some US$20 under Australian values. Australian values compete well with most N.American grades, bar a direct comparison to HRWW, unless you start to take into account the different milling characteristics between H2 white wheat and hard red winter wheat.

The monthly World Ag Supply and Demand Estimates (WASDE) report is out tonight. With most of the N.Hemisphere wheat now in the silo and a good chunk of the Aussie and Argentine crop in the bin we should be getting a much clearer picture of the current world S&D and potential wheat carry over. The dark horse will be a possible increase to the Aussie crop, a possible increase in Russian ending stocks due to slightly slower exports and of course any possible increase in Chinese demand. The recent flash sales of wheat from the USA to China may not be factored into this WASDE as they are very recently reported. We may even see an increase in imports from India. The consensus is for lower wheat stocks, hence recent short covering.