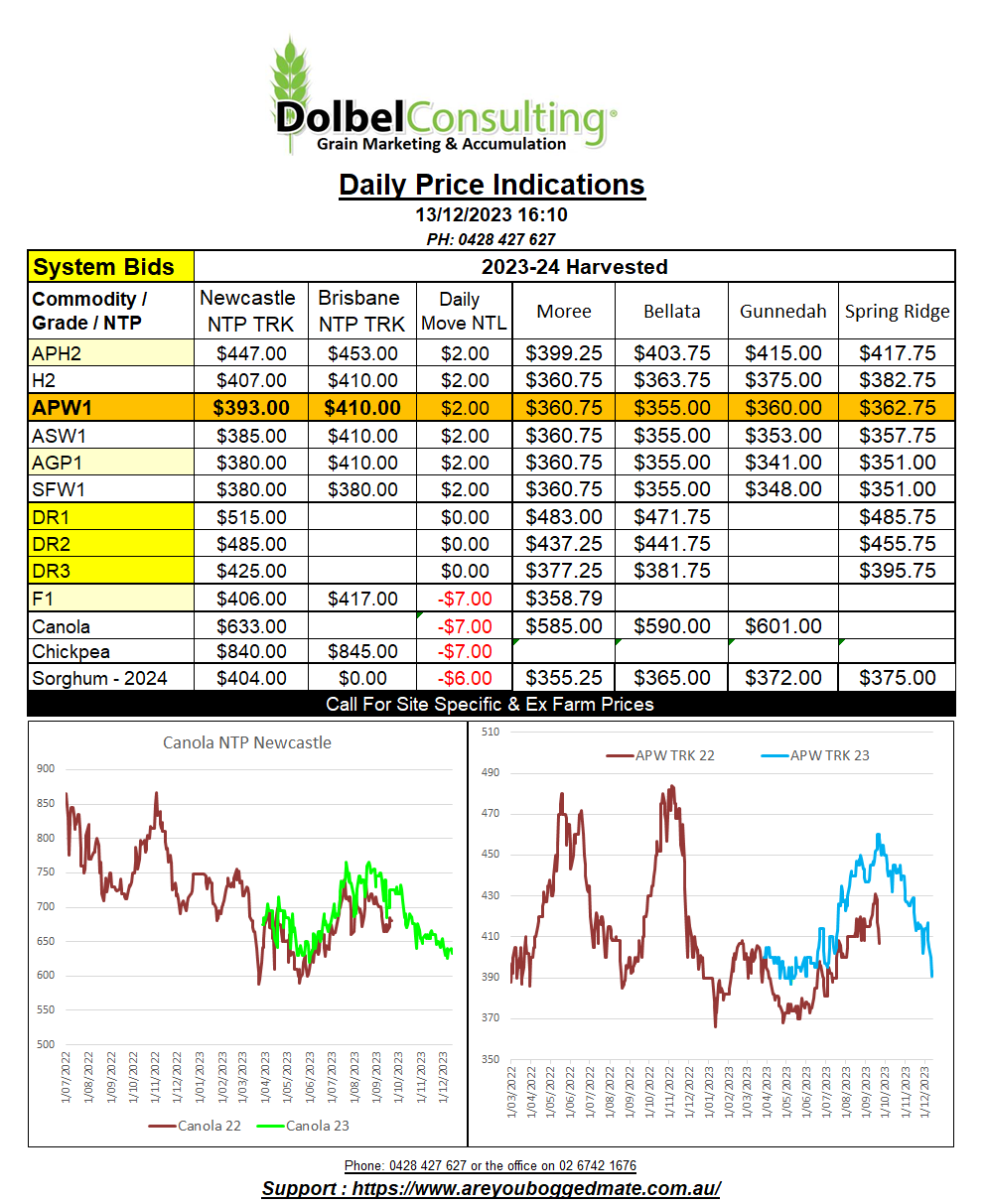

13/12/23 Prices

International markets were basically a reversal of the previous session. Wheat and corn finding support at Chicago, Minneapolis, London and Paris, while the oilseeds stumbled. Paris rapeseed Feb24 slipping E6.75 / tonne and Winnipeg canola falling C$9.80 on the nearby Jan24 slot. Chicago soybeans fell 12.25c/bu on the nearby.

There’s been some very good rain across most of the cropping districts of Argentina over the last week. Some parts of The Pampas seeing in excess of 70mm. Falls were also heavy across the NE of Argentina and through Paraguay and Uruguay. Rainfall across central Brazil remains patchy at best but there has been some good falls across parts of Mato Grosso. It’s not general rain but for those that got under a storm it should help.

Private analyst continue to remind the punters that even if Argentina and Brazil failed to meet current production estimates for soybeans by 10mt-15mt, it would still be a combined S.American record. The size of the S.American crop will weigh on oilseed values for some time.

The latest CFTC report outlining the position of certain participants in the US wheat futures market tells the story of last weeks rally nicely. Managed money, the funds, reversed around 4.09mt of short wheat. The latest report still shows the funds short around 9.12mt though. So expect them to sell any significant rally going forward. This may cap the impact of bullish news that would normally create a significant rally. Say, for instance a sale of 1mt of wheat possibly to China. One would usually consider that news a major market mover, possibly worth 50-100c/bu, but futures may only rally 20 – 40c/bu. This type of short covering may lead to a sideways market in the mid term, depending of the frequency of reporting of positive news. Delays in US sales announcements don’t help anyone, accept maybe those who manage to tied a call option to the market prior to making the announcement.