5/1/24 Prices

A softer close in Chicago soybean futures weighed on both the Winnipeg canola contract and Paris rapeseed futures. The weaker dollar helped, turning the Winnipeg move from a potential -AUD$11.62 to -AUD$8.52. At Paris the move equates to a day to day change of about -AUD$2.80 thanks to a weaker AUD/Euro conversion.

All grades of US wheat futures closed higher. SRWW futures, the highest volume contract, lead the way. HRWW and Spring Wheat futures were not as convincing in their close higher. It will be interesting to see the funds position on the latest CFTC report.

The move has neither a lot of technical or fundamental support behind it. International tender business was minimal, S.Korea in for 50kt of milling wheat from the US, Jordan booked 120kt of milling wheat @ US$276.75 with optional origin, probably from Russia. Egypt reckon they have sown 500,000 more acres of wheat than last year according to their Ag Minister, sounds like he may have an Indian speech writer on staff. Egypt continue to be the world largest or 2nd largest importer of wheat. Jordan is also expected to announce a second 120kt tender in the coming days.

China picked up 50kt of French wheat last week.

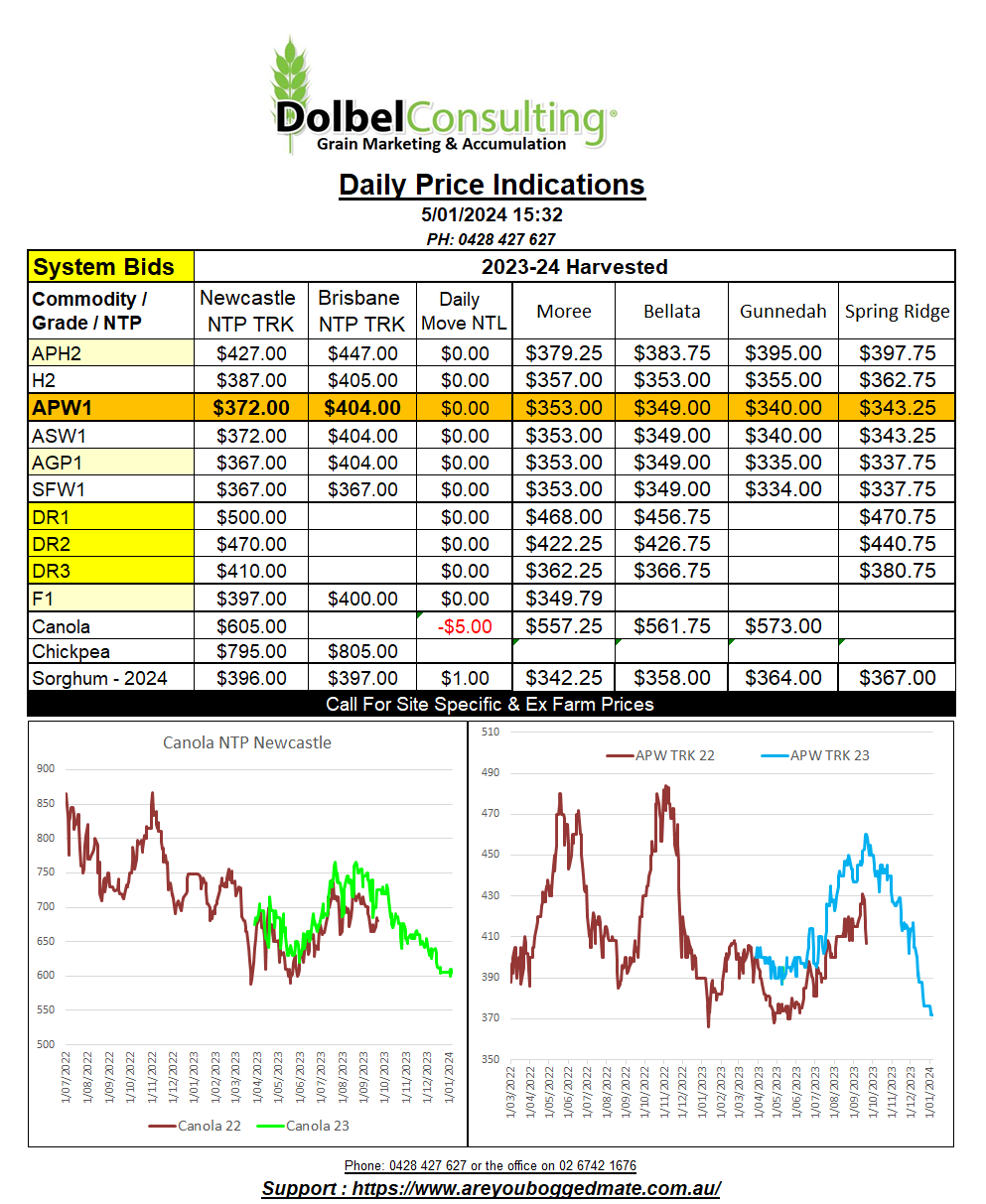

Milling wheat FOB Rouen is worth roughly US$236 today. On the back of an envelope, using China as an end user point, that would roughly convert to an ex farm LPP number of about AUD$360 – $380. One would hope that Aussie H2 wheat would also be able to attract a white wheat premium over European or US wheat of the same protein level. Currently we see H2 bid at $447 delivered Brisbane. That’s not much of premium to export parity.

The weather map continues to look very promising for Brazil and Argentina, both production areas likely to see 30-70mm over the next 7 days.