8/1/24 Prices

The biggest losers overnight were the oilseeds. Funds continue to clear a long position held in Chicago soybean futures as good rain falls, and is predicted to continue to fall, across much of the major production area’s for soybeans (and corn) in Brazil and Argentina.

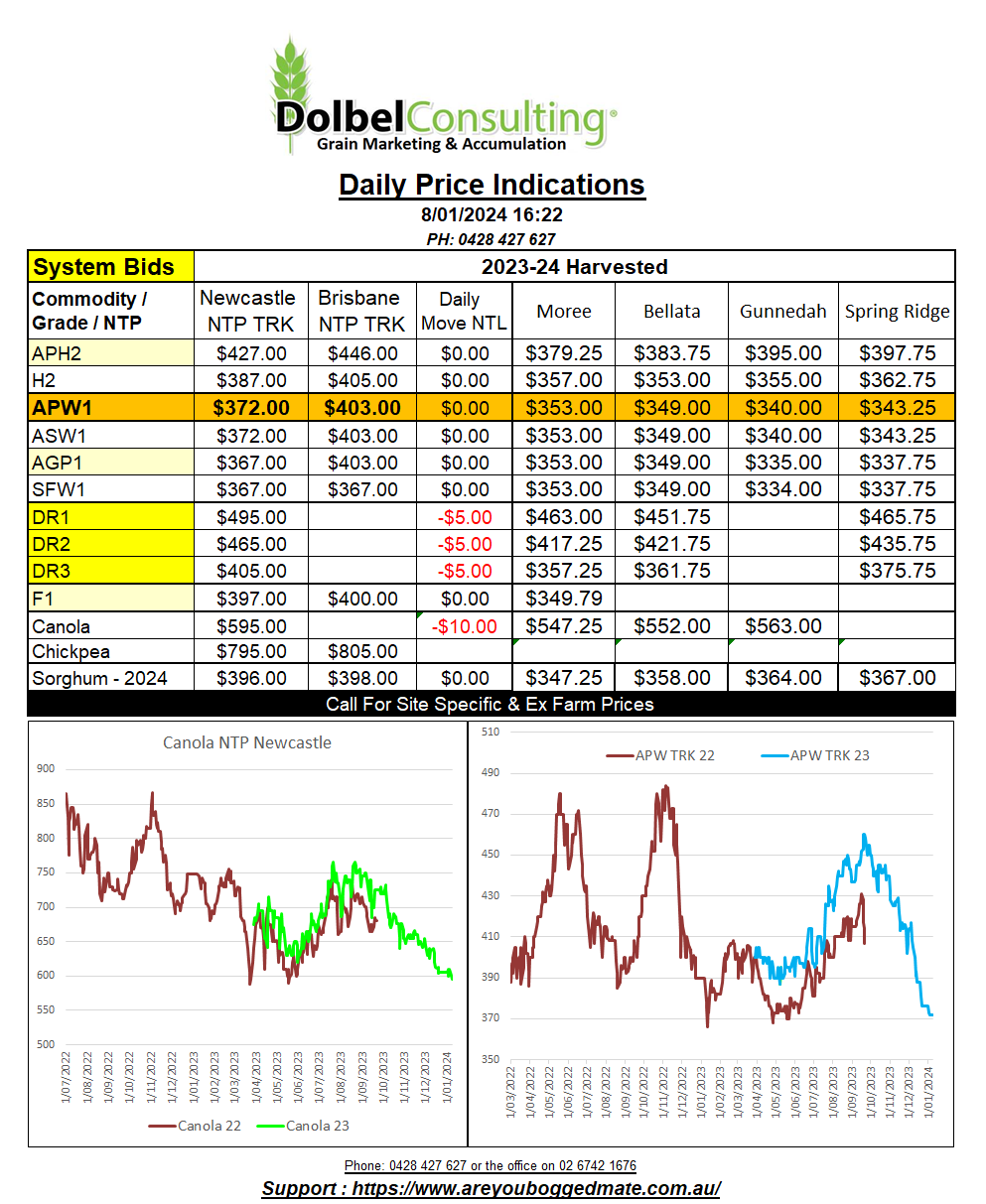

The pressure from this fundamental shift in S.American weather in conjunction with a fund position reversal has weighed on both Winnipeg canola futures and Paris rapeseed future. The later shedding E8.50 in the Feb 2024 slot by the close. This represents a fall of about AUD$15.69 when taking daily fluctuations in the AUD / Euro into account. The conversion of the move in Winnipeg canola futures is even worse. The day to day variation there is about AUD$17.17 lower. All these factors will likely continue to weigh on local bids for both old and new crop canola here short to mid term at least. CME crude oil futures were a little higher but still only 73.80.

S.Korea and Taiwan picked up US milling wheat overnight. Taiwan bought 83kt of milling wheat for Feb / March from CHS. The order was split between 23.5kt of DNS wheat 14.5% protein at US$331.06 FOB, or US$373.05 C&F. HRWW was also bought at US$285.86 FOB US and 4500t of soft wheat @ US$305.07 C&F. A second parcel of DNS was also booked from another trader at US$372.77 C&F. The later March portion also includes HRWW @ US$339.86 C&F and another 4.8kt of soft wheat @ US$293.63 C&F.

The HRWW value of US$285.86 FOB US roughly converts to a comparable price of AUD$415 port, that’s potentially possible off the east coast but unlikely. WA H2 wheat is bid at AUD$385 Kwinana to the grower, which comes out below the sale price, maybe too close to create significant trade margin but close enough to work. WA white wheat should at least pull a $25 premium to HRWW too, so probably close to the money.