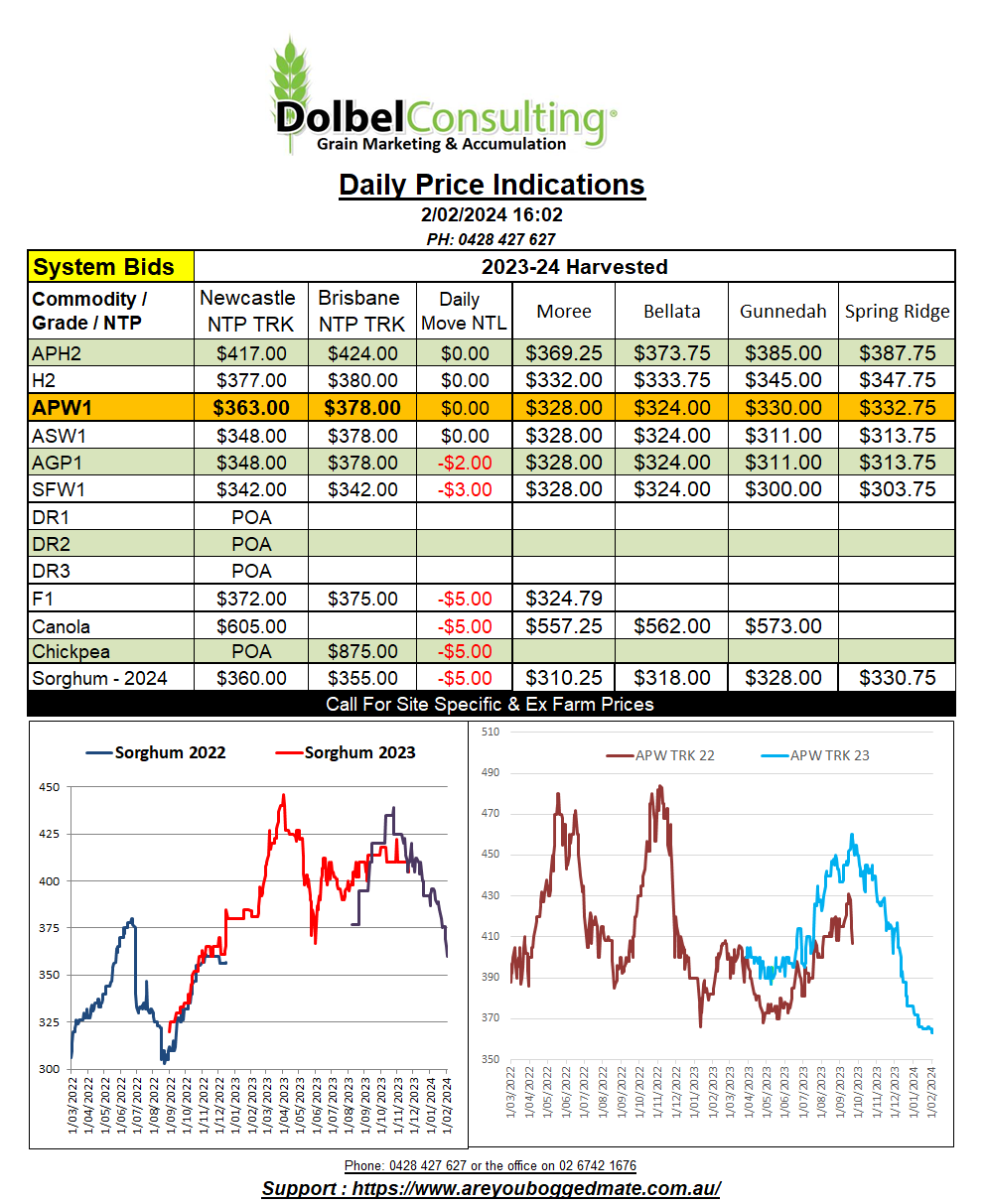

2/2/24 Prices

US weekly net wheat sales were reported by the USDA at 322.5kt, a little lower than both last week and the 4 week average. This didn’t help wheat futures in the US and won’t help us as much as the 0.63% reduction in the AUD against the greenback will. Asian markets remained the best buyer for US wheat. US wheat merchants using price to compete well Asia against a better quality Australian product.

Net US corn sales were good at 1.206mt, up 26% week on week and 58% better than the 4 week average. These numbers made little difference to the corn futures market at Chicago, which closed the session unchanged on the nearby. Cash values out of the Gulf were actually a smidge lower thanks to a higher USD.

Chicago soybeans were hit pretty hard, the losses there being reflected across both the Winnipeg and Paris oilseed market. Paris rapeseed futures slipped E5.75 on the nearby March contract. Winnipeg was back roughly equivalent to AUD$10.48. Cash values for Canadian farmers ex farm SE Saskatchewan were also lower. The average bid for XF SE Sask in March was C$569.19, back C$4.70 according to PDQ. Outer months were hit harder there, back C$9.45 for a April lift. New crop values across SE Sask were back C$12.20 for Sept, to C$570.79.

Durum values across SE Sask were C$2.97 lower for a March lift, yesterday averaging C$425.77 for 1CWAD13 (AUD$483.85). The talk of more Turkish durum tendering had been forcing international durum values lower over the last week. It’s not official but there are reliable trade sources stating that Turkey sold 150kt yesterday at better than expected values, between US$354.10 and US$404.80, depending on port. The values tend to indicate that premium grades are likely to return to the values prior to falling away late January, lower grades may struggle to regain recent losses.

Thailand picked up 120kt of feed wheat, 60kt @ US$262 C&F / 60kt @ US$259 C&F from ADM. Roughly equivalent to AUD$305 XF LPP.