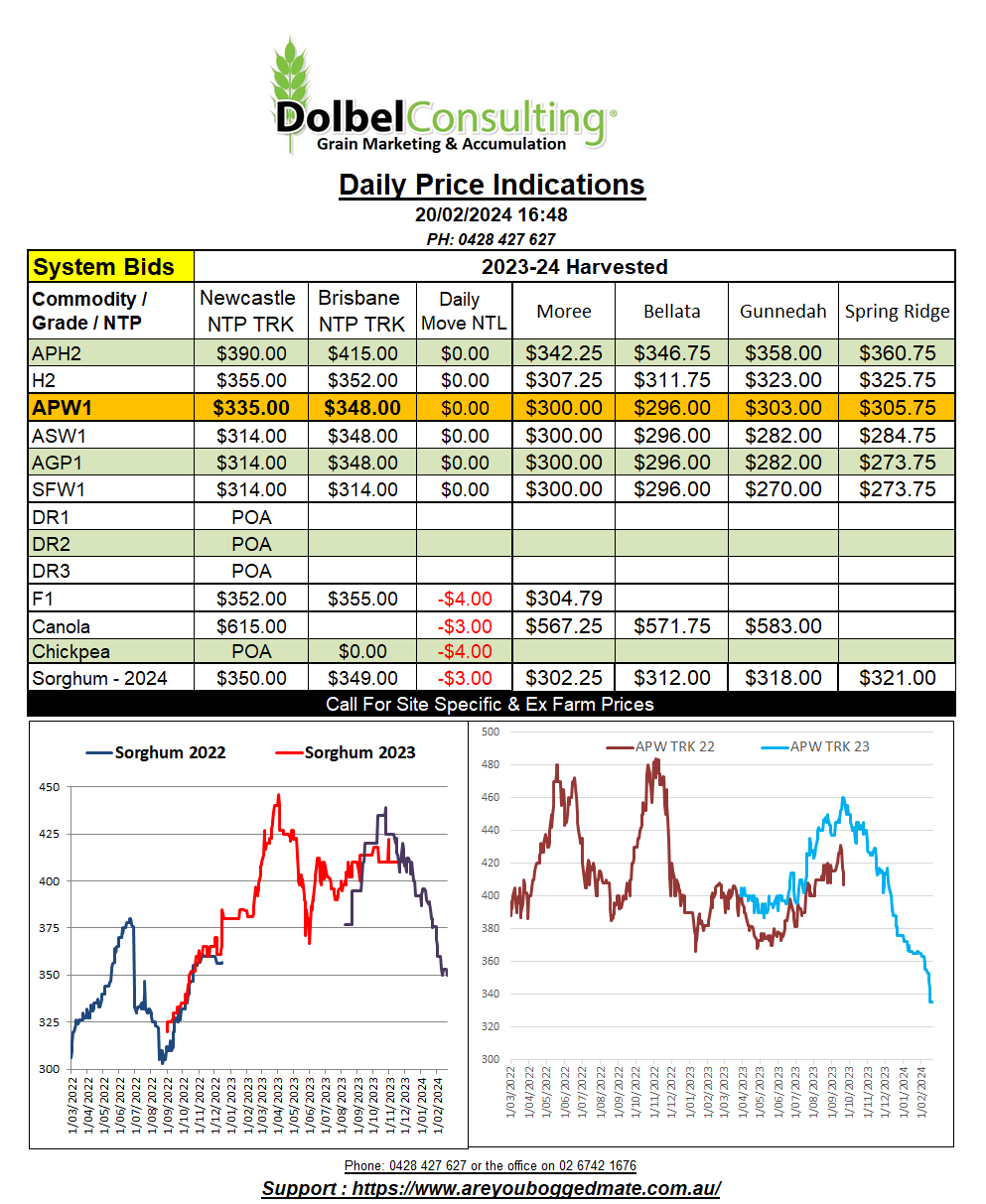

20/2/24 Prices

China is back, the US and Canada took a day off though so market data is a little thin on the ground this morning. Dalian corn futures were lower, the May24 slot shedding Y19, to close at Y2389, or US$331.87 or AUD$507.52 per tonne.

Paris milling wheat futures were back E3.00 on the nearby and E4.25 for the December 24 slot, not an ideal way to start the week. Paris rapeseed was also a little lower, shedding E0.75 on the nearby and E2.25/t for the Feb 25 slot. The spread between the nearby and Feb 25 Paris rapeseed is E5.25, that’s not a lot of carry for the new crop and will probably deter sowings in regions like Australia. Gross margins for new crops, winter crops, is a tight this year. It’s shaping up to be one of those years you might strive for yield over quality in Australia. With China back in the game for Aussie barley I wouldn’t be surprised if there’s a reduction in canola area and an increase in barley area.

Funds still hold a net short in Chicago soft red winter wheat of 57,880 contracts (7.87mt), long 79,676 contracts, short 137,556 contracts a short increase of 1,139 contracts week on week. Funds are also net short in hard red winter wheat and also spring wheat. Managed money is also very much short in corn and soybeans. This is a result of roughly 354 wheat traders.

The durum trade is keeping a close eye on rainfall across the N.African countries of Algeria, Tunisia and Morocco. Both Algeria and Morocco are seeing very dry conditions for the 2023-24 season. Although Tunisia is dry it is at least in better shape than it was this time last year. The same can not be said for Algeria and Morocco. Interesting to note that Italian sowing intentions for durum are also back around 10% on last year. Combine this with dry conditions across the major durum production regions of Italy and the persistent dry in Canada and durum may yet have some life in it for 2024, unless killed by head scab, crown rot…..or any of the other 100 things that mess durum up.