19/3/24 Prices

US wheat futures closed higher on the back of news that Russia had attacked grain infrastructure in Odessa and Mykolaiv ports. The lower volume in the days trade for nearby SRWW at Chicago was also seen as a factor to the increased volatility. Open interest remains exceptionally high.

After last weeks Chinese cancellations of French, Australian and US wheat it may take some good sales to see a rally sustained.

Algeria are in the hunt for some more durum. Most of the punters expect to see Canadian durum pick up the lions share of this tender but there’s also a good chance that Mexican and possibly Turkish durum may also feature. Volume is not expected to be huge, possibly 200kt, anything higher will have an impact on the market. Algeria do not make public their tender results but we should get a good feel for the details later in the week.

Algeria imported roughly 94.5kt of Canadian durum in January, Morocco 80.5kt and Italy 72.2kt. Canadian durum remains some of the best durum available in the world at present.

North Africa durum regions remains very dry, not ideal as the crop is now flowering or trying to fill grain. Harvest there is just 4-6 weeks away.

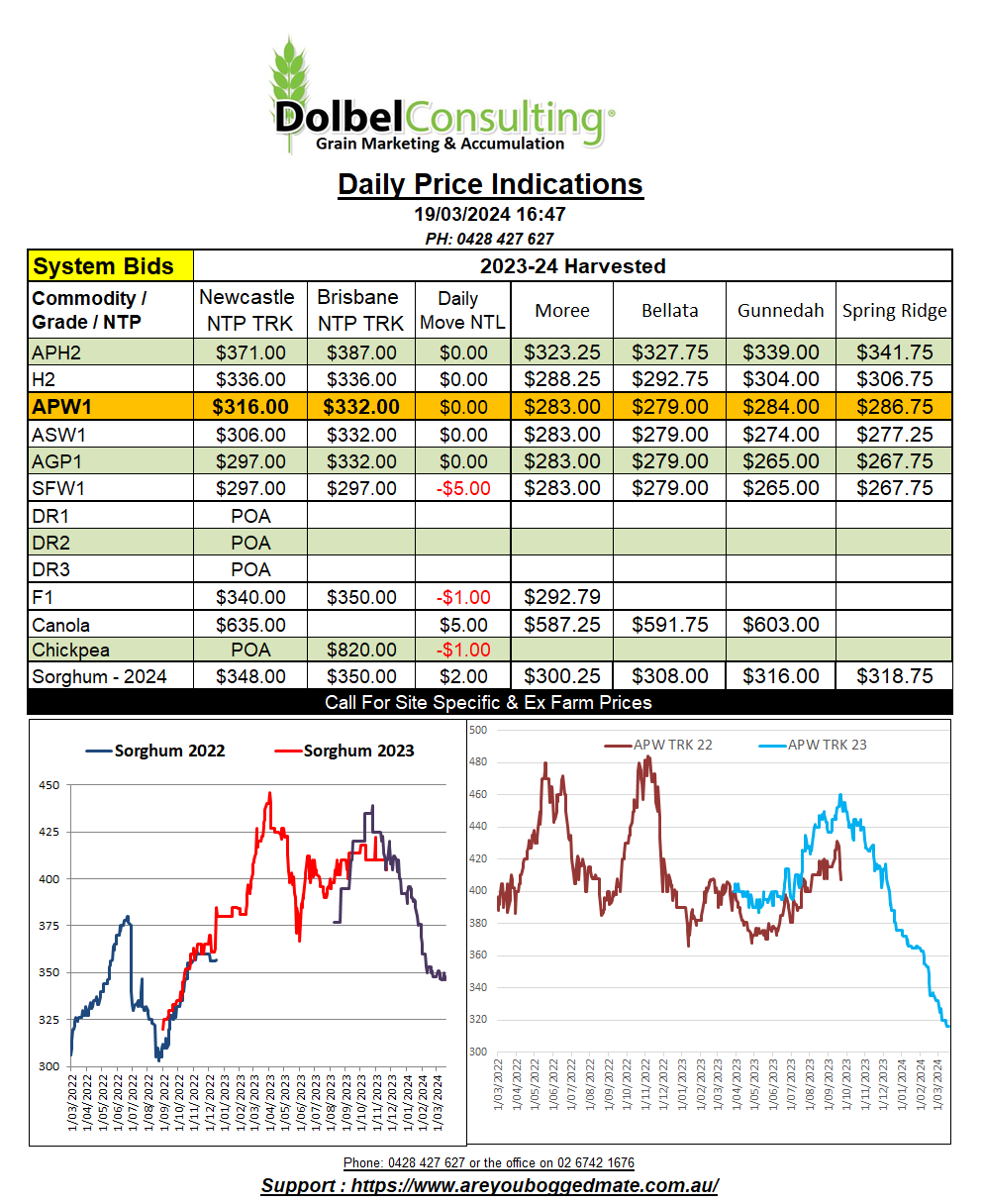

International sorghum values were, in AUD terms, flat. Values out of the US Gulf were mixed, some reports indicating a flat to slightly firmer market while other reports show a sharp jump in FOB Texas values. The Chinese Index was up smidge. World corn values into China were generally flat to slightly firmer. US sorghum export sales were low, down 93% week on week ending March 7th. China remains the key importer of US sorghum.

Australian sorghum sales also remain very lacklustre with no change of export sales volume reported week on week. Graincorp are yet to confirm a booking for sorghum on the Carrington stem for this season.