28/3/24

The slight rally in US wheat futures was not generally reflected across the Paris milling wheat contract. The move in US wheat wasn’t anything to write home about but the fact it broke away from pressure from a lower corn and bean market at Chicago can’t be viewed as bearish. Paris milling wheat was mixed, the Sept / Dec slots a smidge firmer while the nearby and outer months were lower.

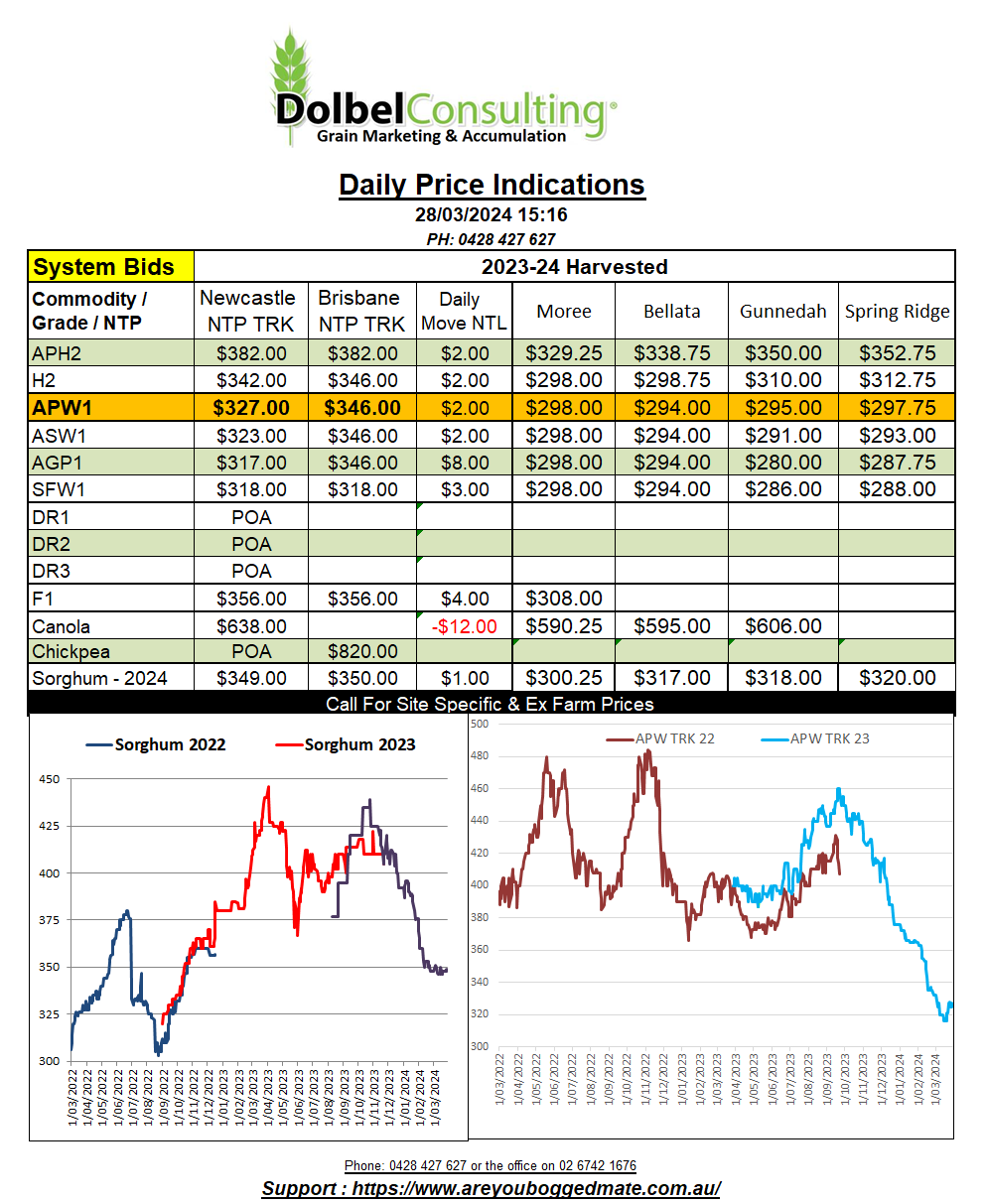

World cash values for wheat were mostly flat to firmer. It’s promising to see Russian values firmer, not matching the lower offers from Romania and Bulgaria in the last major tender.

Without a major production issue in the N.Hemisphere this spring it will be very hard to talk this market up. But at the same time we are also expecting to see world consumption out strip production again. This is starting to make a dint in world ending stocks, particularly for the stock level of the major exporters and world ending stocks excluding China. Global wheat stocks are still presently too high to create a major issue but the next 2 months is where the northern hemisphere crop is made.

Both Paris rapeseed futures and Winnipeg canola futures were lower again last night. Pressure came from large S.American soybean production, and no major concern for the N.Hemisphere oilseed market apart from some possible reduction in Indian rapeseed production.

In Aussie dollar terms the fall in Paris rapeseed futures was roughly equivalent to -AUD$17.65 and the fall in Winnipeg was closer to -AUD$12.10. This is likely to put pressure on local Newcastle port prices for both new and old crop today.

There are signs of visible sprouting in some sorghum fields across SE Queensland. Reports of shot and sprung sorghum around Brookstead. This may put pressure on supply in QLD for the export market, and SOR2 spreads, if these reports continue to grow in size.