21/8/25 Prices

Chicago corn futures basically ignored news of two flash sales during the day. Around 227kt of corn was booked, having little impact on futures values. The trade appeared happy to stand back and wait for the USDA weekly sales report data for last week, due out tomorrow.

Chicago SRWW futures bounced off recent lows, gaining 7c/bu (AUD$4.00/t) in the Dec slot. Both HRWW futures at Chicago and MGEX spring wheat futures both closed unconvincingly higher. Paris milling wheat saw small losses across all months, down half a euro. Paris rapeseed futures were mixed, lower nearby and up €0.25/t in the Feb slot. Chicago soybean futures crawled higher, up just 2c/bu in the Jan slot.

The weaker AUD helps convert most small gains in international wheat values to slight increases compared to yesterday’s conversions. US / Canadian wheat out of the Pacific Northwest and most EU and Black Sea wheat gained roughly AUD$1.00 to AUD$2.00 / tonne.

The US corn tour continues to produce yield estimates generally greater than last year. Soybeans are also being checked, with varying results, some sites better than last year some sites worse. Generally the trend in corn is confirming the bigger estimates the USDA have been promoting. The US are in the running to produce a record corn crop this year. More acres and bigger yields pushing estimates as high as 425mt. Possibly explaining some of the apprehension we are seeing here in the new crop sorghum bid.

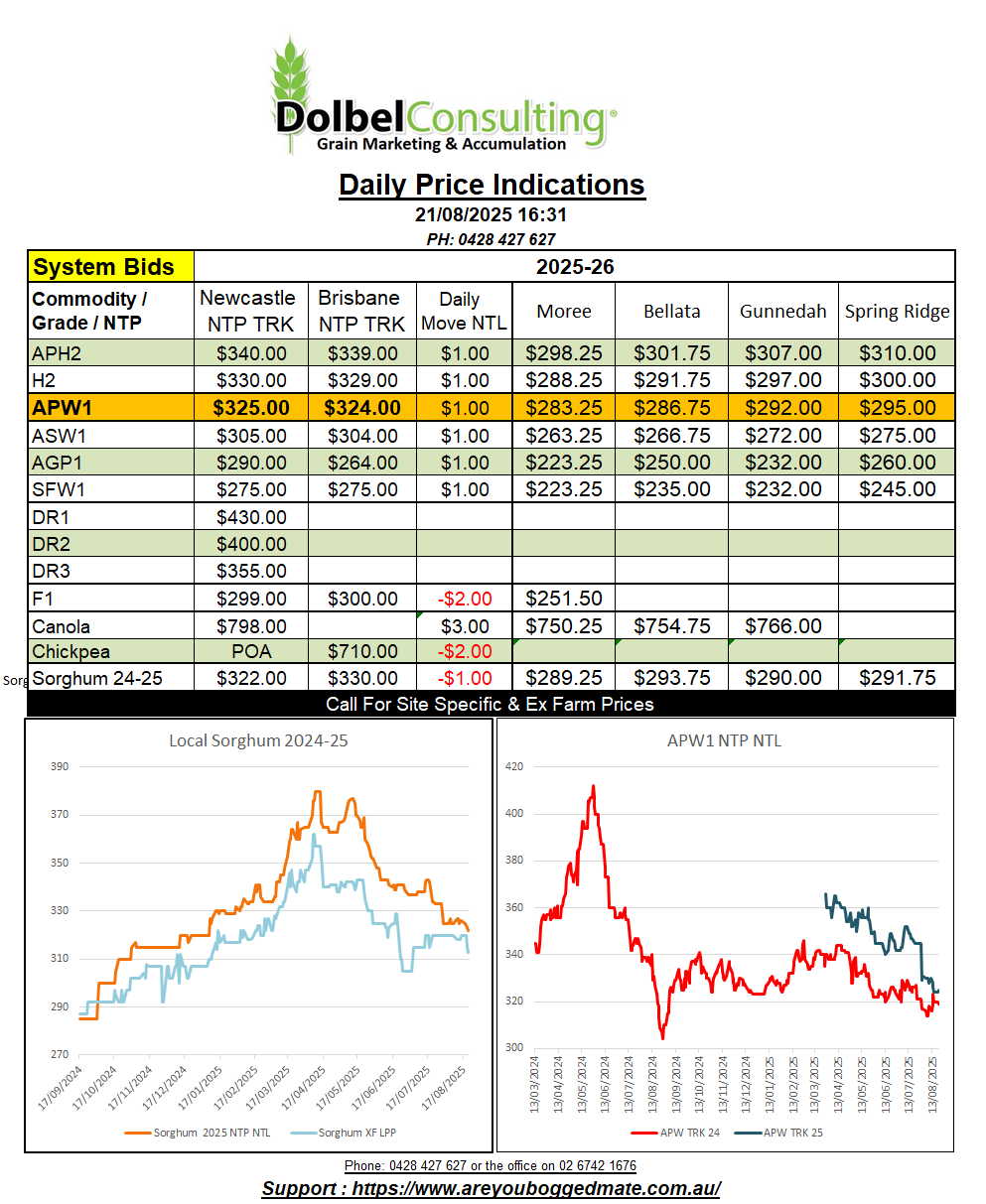

The US projected sorghum production is around 391 million bushels (10.641mt), with a carry in of 1.41mt, increasing year on year supply to 12.06mt. The US project an increase in domestic usage but expect exports to remain unchanged at 6.12mt, resulting in a nett increase in carry over and a reduction in the estimated farm gate price to US$3.70/bu (US$136/t), a 7.5% reduction in price over last season. Possibly optimistic given the tariff with China. If we deduct 7.5% off our seasonal high and low from the 2024-25 crop here, we come up with a price range of AUD$264 to AUD$352 NTP Newcastle.

Chickpeas took a hit yesterday. The number of major buyers participating in public bids did reduce yesterday, that may of had more to do with price adjustment than a general trend sharply lower.

We have seen local new crop chickpea values reduce this week in response to lower numbers at the Delhi market, but we’ve also seen the AUD decline against the Rupiah, almost by enough to counter the weaker Indian values. Overnight Delhi market values ranged from as low as 6069Rs/Q to 6381Rs/Q, a range of roughly AUD$66.00 / tonne. Last priced at 6225Rs/Q.

The closing value roughly converts back to a packer bid somewhere around AUD$770 / tonne without trade margin and some associated costs. Currently we are seeing Narrabri packer bid at roughly AUD$660.00. One would assume that this would allow a trader to still generate profit even if they were booked towards the lower end of the market variation seen last night.

Demand into both Bangladesh and Pakistan remains strong after poor production. Australian chickpeas will be needed to top up regional supplies.

Yellow peas from Canada and the Black Sea continue to offer a cheap alternative to chickpeas. Canadian yellow peas are offered at roughly US$350 – US$400 CnF sub continent, some US$50.00 higher than the Black Sea equivalent. The substitution of pulses where possible will be the cap in the market.

Further falls from the Downs to Dubbo continue to do more good than harm for sown crops. I’m not sure if the addition to potential yields will counter the reduction in area though. If you haven’t sent me you winter crop sowing data please do so as soon as possible.