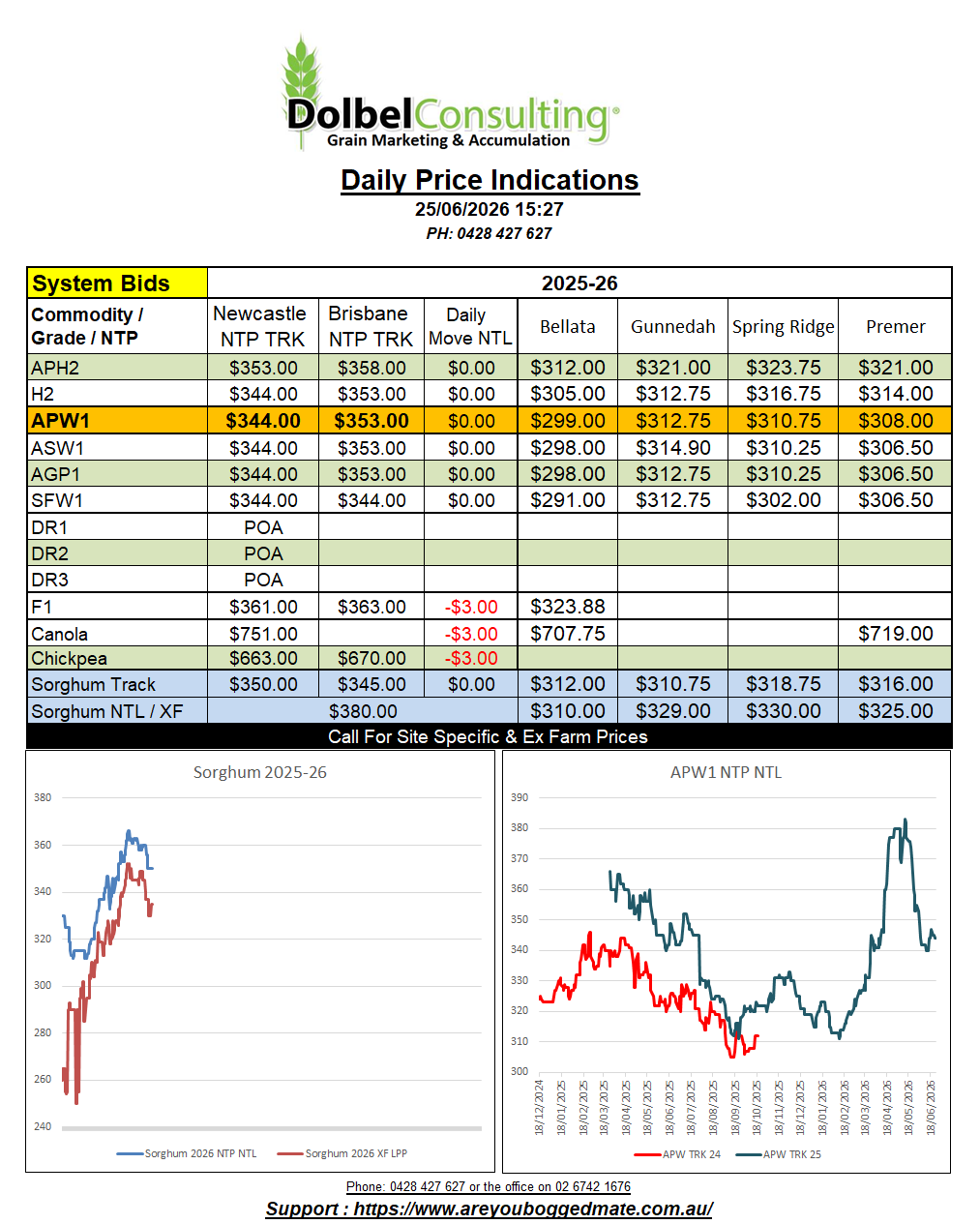

25/6/26 Prices

The 2.25% decline in the AUD against the Indian Rupee is probably not the biggest thing to happen in the grains industry overnight, but it’s a thing worth looking at. The Delhi mandi price was relatively stable overnight. The average price by the close was roughly 5949Rs/Q, up just 5Rs/Q, not much. The comparison between yesterdays conversion back to AUD/t and this mornings is stark though, the conversion increasing by AUD$21.33/t.

The reason for the decline maybe as simple as the fall in the value of the Rs is over. Recently the Indian Rupee had fallen sharply, changes to capital gains tax laws had seen a large out flow of funds from India. The Indian government had also wanted to see the Rs weaker to strengthen export competitiveness. One of these two reasons is worth looking at very closely.

Indian now finds itself (and it’s gold reserves) in good shape compared to some countries now talking interest rate rises. If the US / EU is to go through a devaluation process it may come out as a very healthy import destination for chickpeas in the future.

The AUD was mostly sideways against other major currencies, including the USD.

Very wet conditions in parts of the central US corn belt may see crop ratings for soybeans fall week on week on Tuesday. Currently the rain in the States has been mostly beneficial, but too much of a good thing is still too much. Meanwhile canola and rapeseed futures handed back some of the value gained in the last session. With lower crude oil and palm oil futures now becoming an anchor to further gains in canola, we may need to see a reduction in US soybean crop condition ratings to sustain current values.

US wheat, corn and soybeans futures were all slightly softer. EU futures for wheat and corn closed in the green, on the back of weather concerns, bar rapeseed at Paris which fell one Euro in the Feb 27 slot.