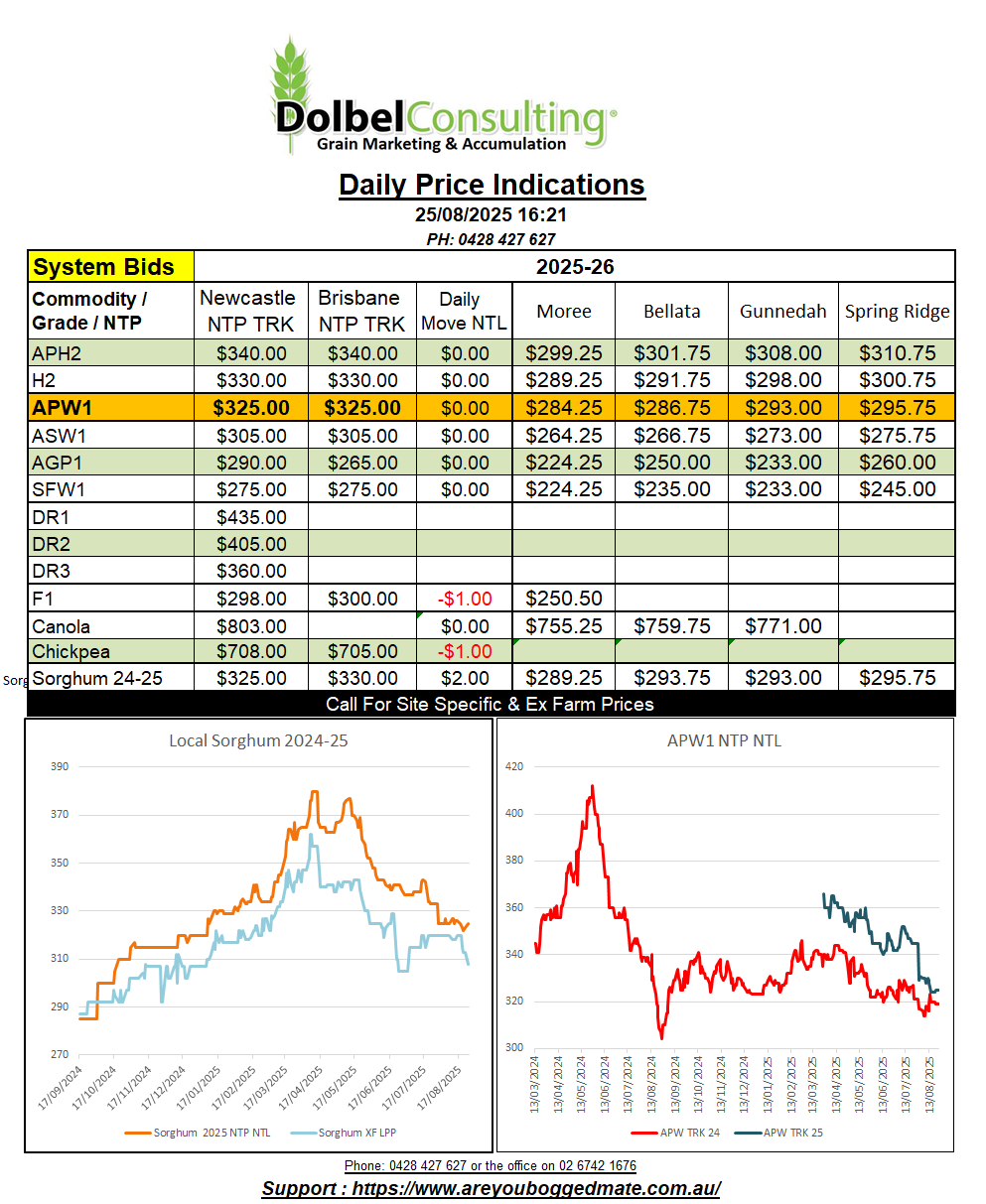

25/8/25 Prices

Chicago grain futures were mixed, soft red winter wheat was either side of unchanged, hard red winter wheat was lower and MGEX spring wheat followed the lead from SRWW, up 0.25c/bu nearby and unchanged in the Dec slot. The big news came from the currency market. The US FED indicating there is the chance of a drop in US rates in September. Wall St took that chance and ran with it. Not only do we have US wheat cheap but with a weaker USD we could see it cheaper again when compared to other exporters.

Values out of the EU pushed lower, Paris milling wheat futures back €2.00/t in the Dec slot. Cash wheat values FOB Black Sea were relatively unchanged. New crop wheat FOB Argentina was unchanged, still showing a premium to the old crop. There’s currently a US$45 spread in 12% wheat FOB up river Argentina between nearby and November. Given the season one might expect to see this eroded as harvest nears. Currently Argie wheat at the November value is that far above other major exporter values into most markets that is will need to shed some serious value in this delivery slot to make a sale. 14 day rainfall totals for much of the Argentine wheat belt have exceeded 30mm, with many of the eastern parts seeing 50-100mm.

Rainfall continues to be above average for both the Russian and Kazakhstan spring wheat region. What was shaping up to be a dream season for this part of the world may soon develop into a nightmare unless harvest conditions improve. Recent production estimates for Russia have increased by at least 2mt, much of that on the back of the potential of the spring wheat crop. If something like test weight is reduced we may start to see both production estimates, and demand, for Russian spring wheat reduced.

Rain is continuing to be a slight issue for some producers on the Canadian Prairies too. Over the last 14 days much of the country that had been dry during the growing season has seen 25-50mm of rain now the headers are out of the shed. Rainfall hasn’t been restricted to the southern wheat growing districts. Northern parts of the prairies across Alberta and Saskatchewan, prime canola country, have also seen rainfall, up to 80mm in parts of N.Central Sask.

The AUD will be a problem on Monday. The conversion of both international grain futures and cash values to Aussie dollars per tonne this morning is showing downside potential of $4.00 to $5.00. The move in the AUD responsible for roughly 72% of that downside. The AUD did soften for much of the week, but turned that around last night.

The AUD was sharply higher against the Indian rupiah, up 1.13%. Combine this move in the dollar with a 49Rs/Q move lower in cash values at the Delhi market for chickpeas, and we have a difference in the day to day conversion of the Delhi market price of roughly -AUD$21.02/t. This would make the week on week change in the value roughly AUD$22.37 lower than last Friday’s conversion.

As is so common with the currency market it is more about what is said than done. The US FED talked more about US unemployment than rising inflation. The market interpreted that as “we will probably cut US rates in September”. Powell stated that the data will determine any move, and that data is yet to be viewed. The punters were all over it and bet that rates would fall. Thus we have sudden strength in the AUD, unless we see lower rates here in the next month or US rates remain unchanged in Sept, the AUD will be a thorn in the side to exporters.

The move in the AUD countered the move in Canadian canola values. Winnipeg canola futures closed AUD$3.46/t higher, while the AUD had a negative impact on the conversion of AUD$3.47 / tonne. The move in the AUD also exacerbating the decline in US wheat futures, Paris rapeseed and a raft of cash values for wheat, barley, rapeseed, corn, and sorghum from around the world. In the case of barley there was actually a few FOB values that moved higher, but not by a value large enough to counter the move in the AUD.