31/10/25 Prices

Watching the US soybean futures market was interesting yesterday. Trump finally met with Xi and exclaimed the meeting was great, the best meeting ever, rating it a 12 out of 10. Soybean futures plummeted 24c/bu before eventually recovering late in the session and making modest gains. The trading range in January bean futures at Chicago was wide, the session high 1114.5c/bu and the low at 1070.5c/bu, 44c/bu (AUD$24.68/t). China has apparently agreed to buy 12mt of US soybeans and committed to a minimum of 25mt of US beans spread over the next 3 years. So basically on par, if not a little lower, than what they usually buy during the S.American off season.

One might think this is what had an impact on Canadian canola values overnight, it probably did a little, but more importantly was the news that Canada may be considering removing or reducing the tariff they put on Chinese electric vehicles. China placed a massive 75.8% import tax on Canadian canola in response to the EV tax. China has stated that they would remove the canola tax if Canada was to remove the EV tax.

The result was a jump in Winnipeg canola futures, not a huge jump, when taking the day to day change in the AUD/CAD into account, it is roughly equivalent to a change of +AUD$8.24/t to the Winnipeg closing price in February.

This probably isn’t the best news for Australian farmers and may result in a slightly weaker basis here for canola today. Paris futures were up €0.25/t in the Feb slot. Fundamentally the global S&D for canola might remain unchanged. We’ll just have to speculate on where Chinese demand will come from. If they put Canadian canola back on the menu then it actually means they have the ability to play off Aussie against Canadian, and potentially Black Sea canola going forward. It may become more about how much China buys, as opposed to who they buy from going forward. The EU may find themselves the ones coming out of this having to pay more. I have no empathy for the EU considering their ISCC scheme is often interpreted as nothing more than simple extortion.

Wheat values around the world were generally weaker, following the trend in other grains after a “buy the rumour, sell the fact” week.

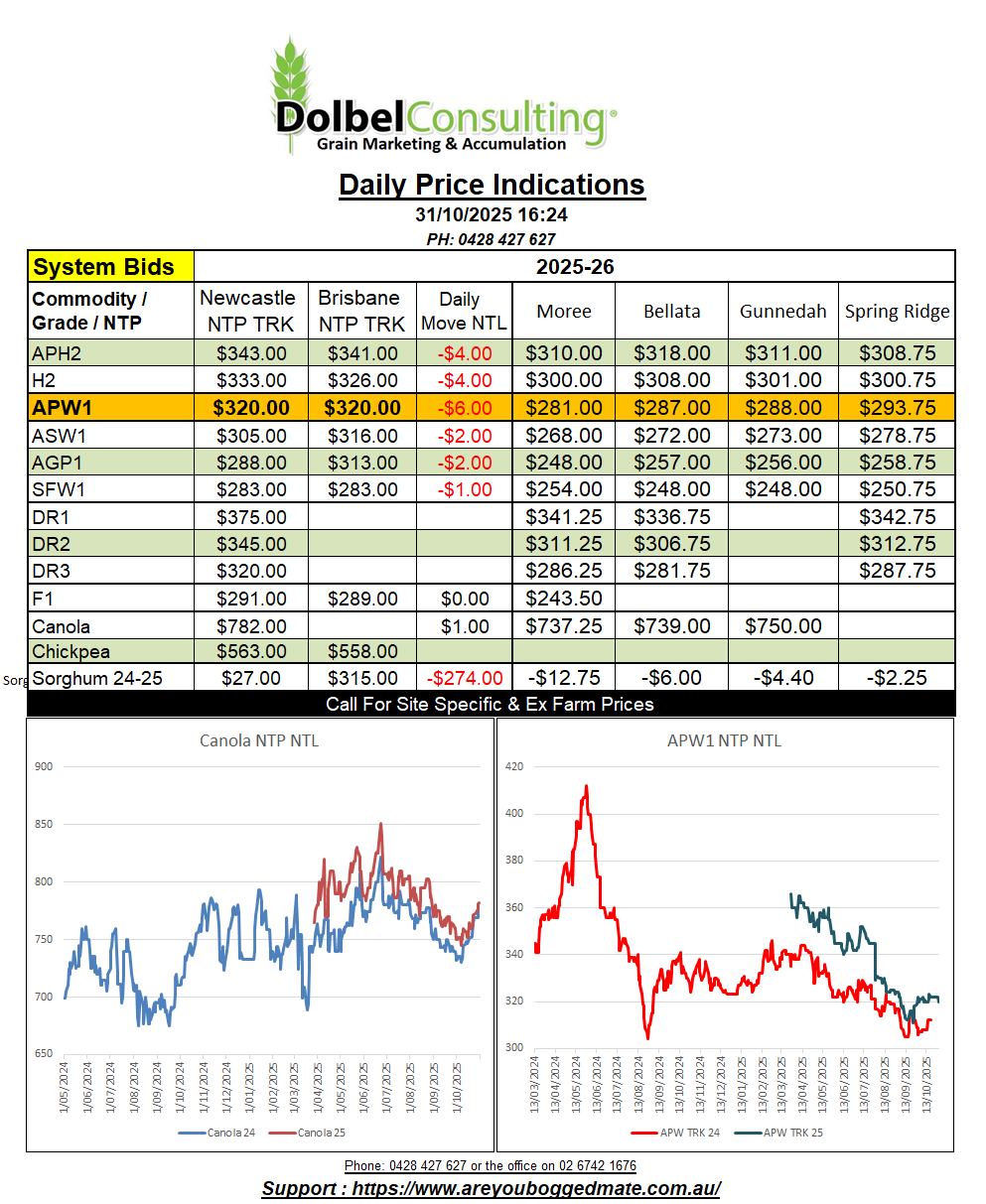

Local markets were sideways. There was further demand for ASW+ into the Tamworth feed market. Bids are firmer for the Q1 2026 period. At $320 delivered Tamworth end user it’s a mile better than the track. It’s been years since feed grains were better off on the track though so no surprise there.

Is $320 delivered a fair price. Let’s look at what it would cost the buyer to execute APW on the track at Spring Ridge and cart that by road to Tamworth. APW at Spring Ridge was bid at $293.75/t yesterday, that’d make it roughly $319.50 Free On Truck, plus freight to Tamworth, plus trade margin. Forgetting trade margin, the landed Tamworth price would be around $340 delivered. So $20.00 above the current delivered bid.

The big thing going forward will be quality, not only here but out west, and what that grain can move into Tamworth at. Yesterday saw APW at Coonamble bid at $285.25 / tonne, roughly $311 FOT, or $343 delivered Tamworth, FOT track Walgett into Tamworth would work out around $346 delivered. So there’s not a lot of opportunity on the track to buy lower, unless grades slip below APW1.

The spread on the track between APW and ASW is -$15.00, so the trade / consumer, would be sweating on some ASW coming in both here and further north.

New crop sorghum values were back a little at the public level by road into Newcastle March / April 2026 yesterday, but Brisbane and Downs bids for the same delivery period were generally unchanged. The weather in China that is hurting a lot of the summer grown crops across the North China Plain may, in time, pull sorghum values higher. With damaged corn the local producer may well find it better to feed sorghum, maybe. This will depend on the price of imported corn versus what the Baijiu market can pay. US corn / sorghum is pretty much the same price C&F China and still attracts a Chinese import tax.