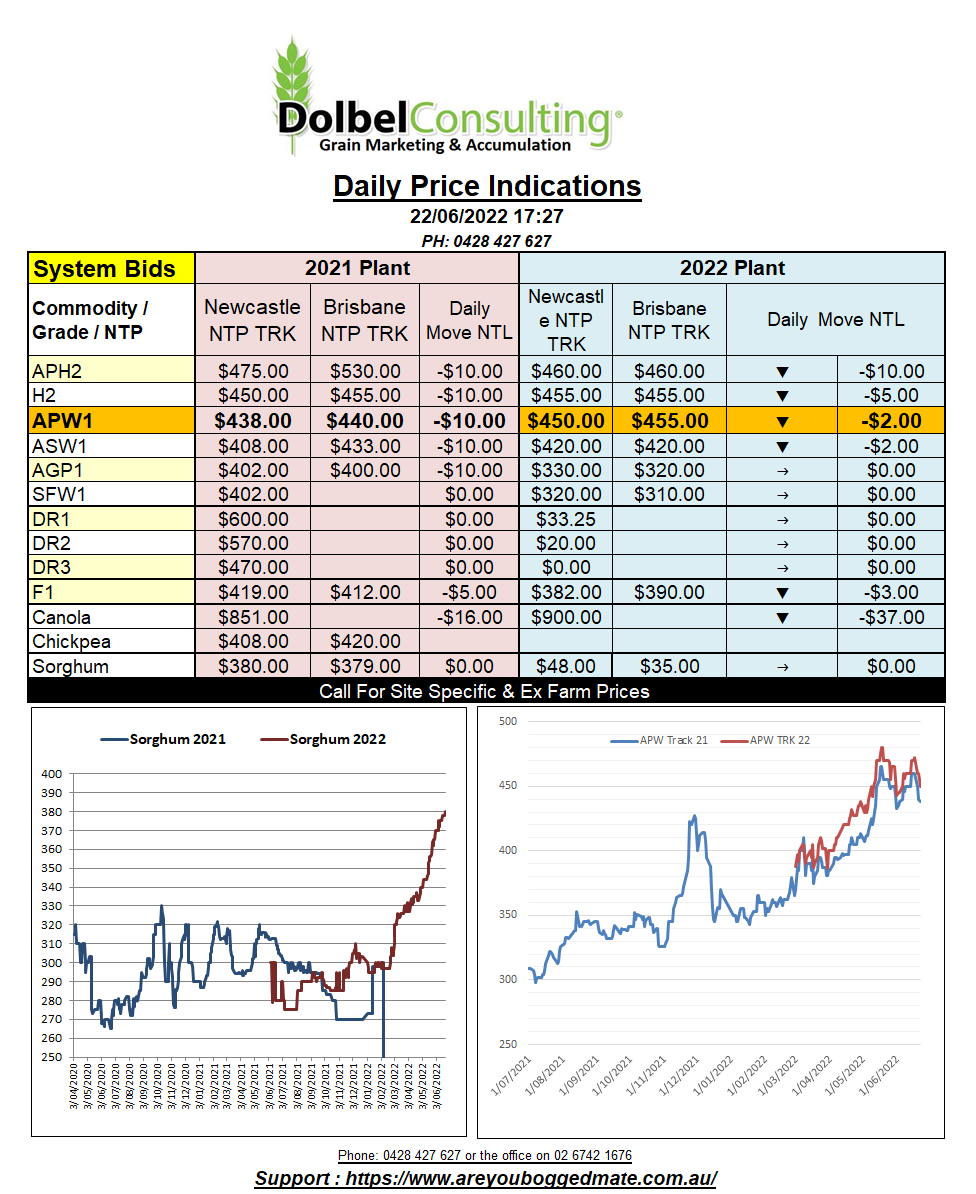

22/6/22 Prices

US wheat futures were crushed in overnight trade. Talk of a Ukraine / Russia deal to allow grain exports from Black Sea ports is apparently gaining momentum, if not in the real world, it is over a cup of coffee at the morning meeting of the fund managers who are long wheat futures. This has the nearby Chicago soft red winter wheat contract back 103c/bu (AUD$54.29/t) in the last two sessions. The December contract has fallen over 250c/bu, about AUD$132/t, since the 16th of May.

It does tend to raise the question “what is wheat really worth ?”. Local new crop APW1 did not follow the US contracts up, basis imploded. Hopefully we will not reflect the correction lower. Since the 16th of May local APW had fallen AUD$15. So we now have Dec wheat at Chicago priced roughly the same as what it was around the 4th of April. At that time local APW new crop was priced at AUD$405 @ 75c currency, the currency fall since then is worth about AUD$35. So if we are to believe local values are closer to reality than the US futures market than today we could see something closer to $440 – $450 Newcastle track for new crop, a plausible fall of AUD$20. A bid around this value would still represent some pretty crappy basis though.

Technically CME Dec wheat is close to neutral, does this signal a reprieve in selling tonight, potentially, but there are no rules for this kind of volatility.

Algeria was said to have bought 660kt of wheat at US$445 CFR. This price would equate to roughly US$387 NOLA, that’s about 10.53/bu, that’s still below where the US FOB price for HRWW was on Friday, even if you deduct the 105c drop since then. Would the US be competitive into Algeria normally, well no it’s unlikely, so it’s probably not a fair comparison.

US corn crop rating declined 2% to 70% G/E, 95% sown. Kansas wheat harvest 27% complete, hot weather assisting. US winter wheat crop condition declined 1% to 30% G/E. Spring wheat 98% sown, condition improved to 59% G/E, + 5%.