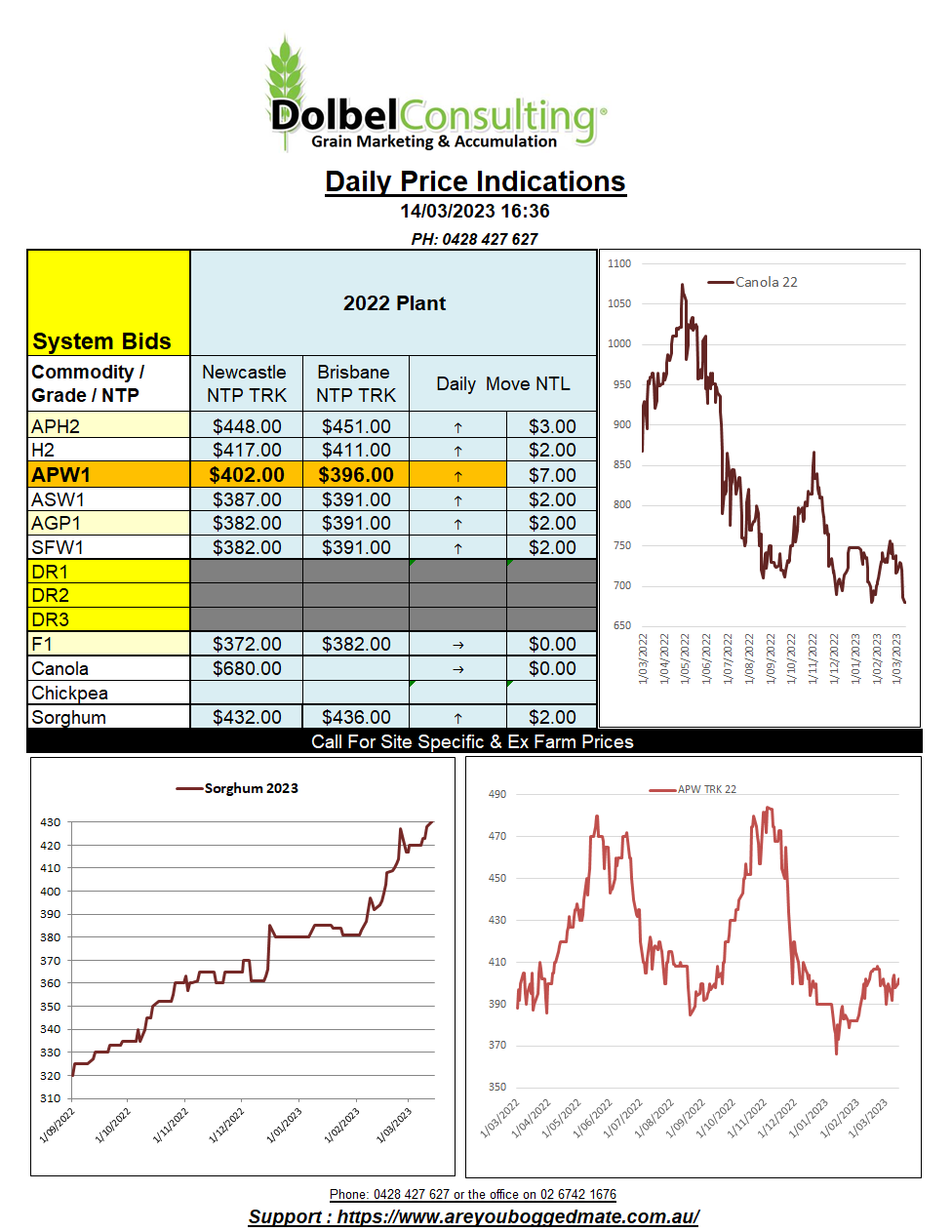

14/3/23 Prices

Black Sea grain corridor deal looks more certain, today…… I mean really has it ever looked uncertain over the last couple of weeks. The Russians have objected to a few things but really, does it make any difference to the Russians, no, no it doesn’t their grain export pace has been strong, the weather having more of an impact on their export volume than any sanctions have.

Overnight Russia has suggested a shorter extension time frame for the new deal. 60 days versus the previous 120 days. According to Russian minister Vershinin “Our further stance will be determined upon tangible progress on normalization of our agricultural exports, not in words, but in deeds,” What does this actually mean ? Sanctions have not been aimed at agricultural exports, but sanctions have been targeted at payments systems, logistic restraints, and increased costs such as insurance have created a barrier. This is what Russia is trying to dismantle.

As expected, Ukraine do not agree to anything less than the 120 days extension terms. The possible impasse between the two resulted in some volatility in wheat futures, more so in Europe than in the USA. Paris milling wheat futures pushed E5.25 higher on the nearby contract and E4.00 in the Dec 23 slot. London feed wheat and Paris corn also found support.

Paris rapeseed futures were not invited to that party. Instead, Paris rapeseed found spill over pressure from a lower Chicago soybean pit and a sharply lower ICE canola contract at Winnipeg. Both markets are being largely influenced by the size of the currently being harvested Brazilian soybean crop. Dry weather in Argentina continues to be overlooked, Brazilian production is expected to counter serious losses to the Argentine corn and bean crop.

Chicago wheat futures found a little support from Black Sea Corridor negotiation developments but was countered greatly by the poor weekly US export inspection results, which fell well below trade expectation