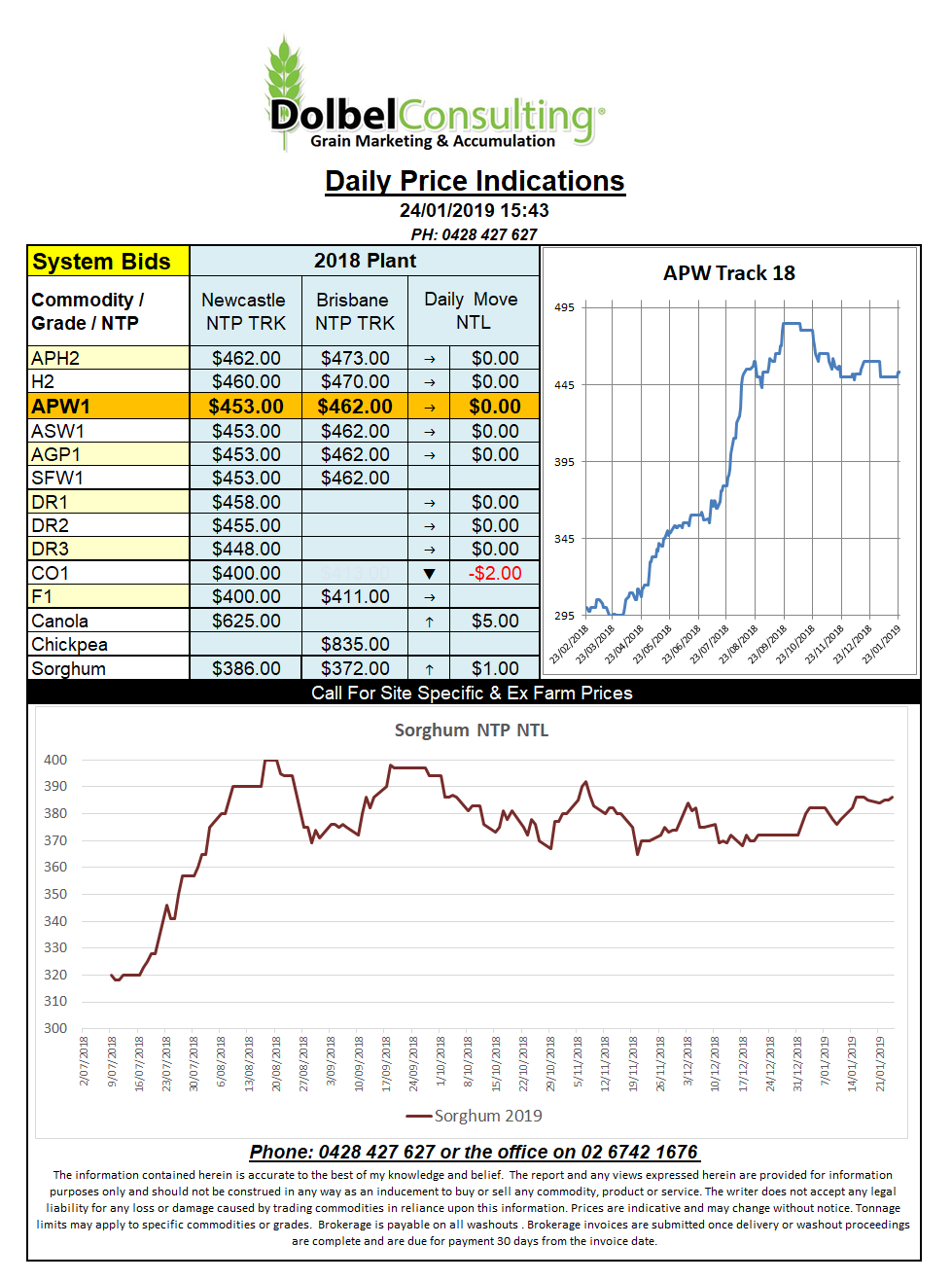

Prices 24/1/19

In the US corn futures were flat while soybeans and wheat moved higher.

Soybeans found strength in the poor weather being experienced in Brazil and to some extent Argentina (wet). Dry weather is expected to persist for another week or two across Mato Grosso which generally produces around a third of the countries soybeans. To the SE of Mato Grosso is also dry. Combined these states to the SE make up close to another 30% of production.

Current production estimates are still around 118mt, only slightly lower than last year’s record but in the last few days there has been a few private predictions closer to 110mt. A far cry from the 130mt some punters where backing at planting time.

On the international market we continue to see milling wheat values creeping higher. Russian offers out of the Black Sea are there at roughly US$243 per tonne for good quality milling wheat. Wheat out of the US Pacific North West is firmer by a couple of dollars. The PNW continues to lead the way in US exports as Asian markets turn to the US as prices are generally lower than Australian values but quality is also a little lower.

Tunisia paid a little more than last month for 100kt of milling wheat. Priced at US$259.70 CFR for Feb it’s basically a dollar higher. It was an optional origin tender but at these values can almost work from Europe or the Black Sea but I’d be putting money on the Black Sea. Looking at European milling wheat futures their wheat maybe around US$10 above the mark.