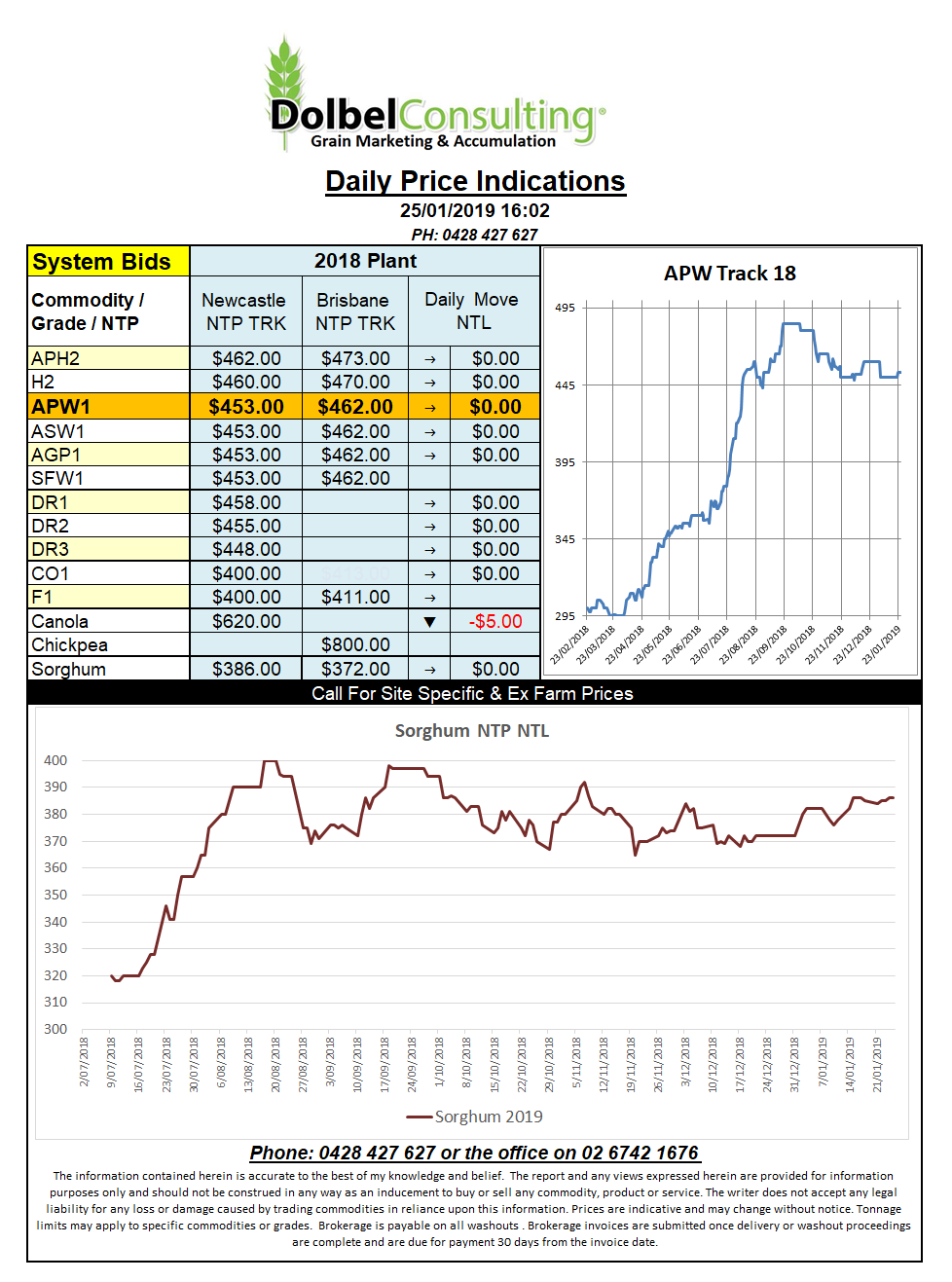

Prices 25/1/19

Oh my god, market data, it’s only the International Grains Council monthly S&D report but well, it might just be the substitute the world was looking for now the USDA has been put to sleep.

So a quick look at a yawn worthy report tells me that 2018-19 world wheat production is pegged at 737mt, year on year that is quite a change, 30mt down but it is much higher than their previous stab in December which is a little bearish. Ending stocks are the key, at 263mt that’s a year on year decrease of 7mt. The stocks to use ratio is still pretty fat though at over 35%, we really need to see this down into the 20’s to create serious volatility.

It was more of the same in the US futures markets, it’s been a case of take a few give a few for a while now. The direction for the month at least is higher though with the nearby soft wheat contract at Chicago putting on about AUD$10 for the month. Much of that move was done in the first 9 days though so the last couple of weeks has been very tiring.

The same market drivers are in place, China / US trade negotiations crawl along at a political pace not a futures pace. Those poor caffeinated punters must be going crazy. Weather in S.America is also a major driver for the oilseed market. It’s still pretty dry in Mato Grosso, Brazil. Most of the rain has been to the north and SE of the driest regions. Further south in Argentina the seven day totals are still impressive with around 150mm falling across the far NE of the soybean belt. The major bean area seeing a nice 50mm.