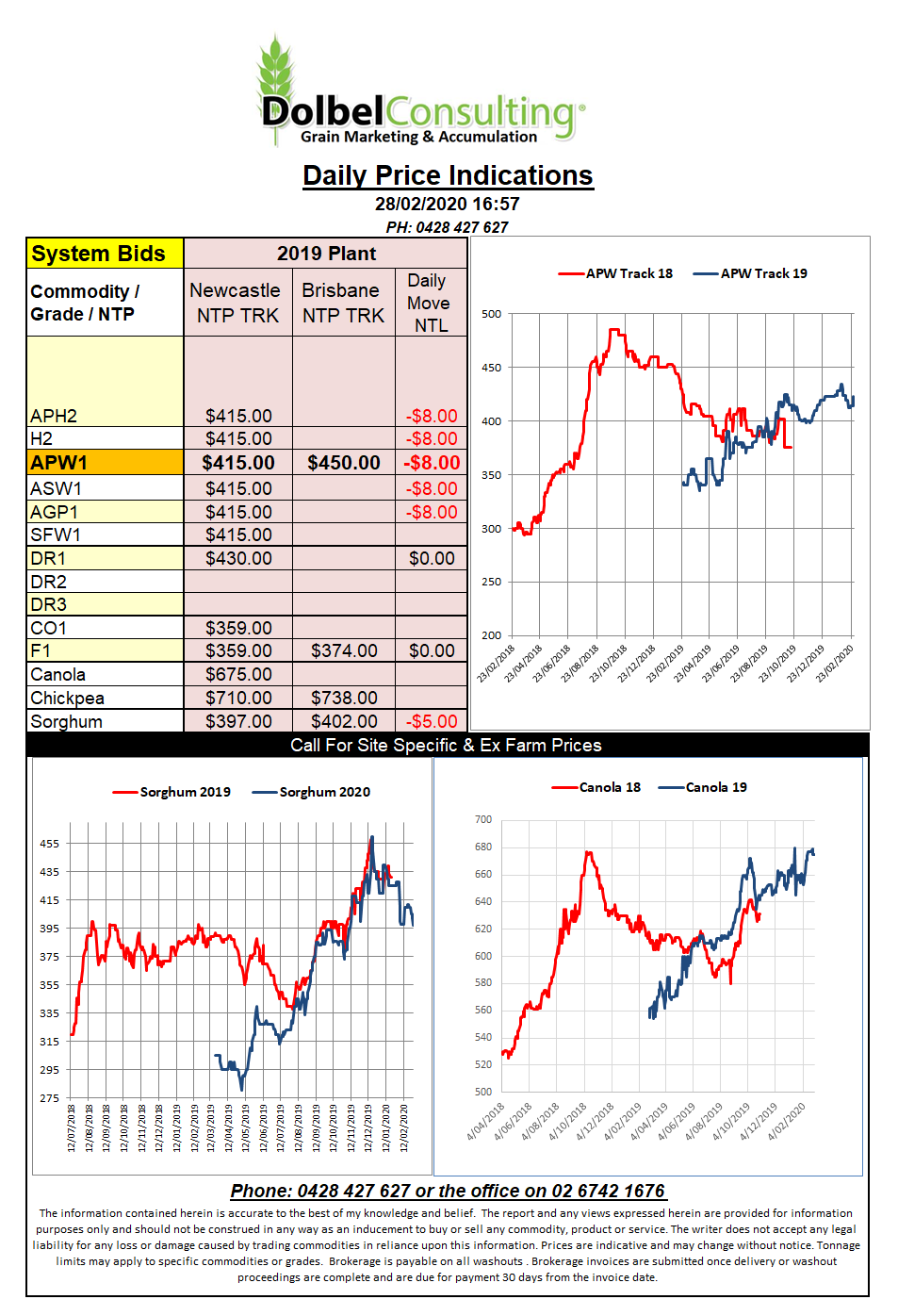

28/2/20 Prices

Weekly US wheat sales were less than inspiring and the market reacted accordingly. At 382kt of old crop wheat sales it was lower than trade estimates prior to the release of the report. Even combined with new crop sales of 68kt the final figure still came in below expectations. The market didn’t need much to continue down the path of least resistance.

The International Grains Council (IGC) had their monthly stab at the grains market last night. New crop wheat, 20/21, production was increased to 769mt, that’s a record. Old crop was also increased 2mt over last month’s estimate, now 763mt. Increases are mainly attributed to better crops in India 103.6mt vs 102.2mt. Black Sea production was left unchanged while Australian production was reduced from 15.9mt to 15.2mt. The IGC still expect to see Australia with ending wheat stocks of 4mt, dreamin.

Wheat may have some issues in regards to building stocks as we move into the northern hemisphere harvest. Argentina has grown a good crop this year, around 19.5mt, but exports continue to be slow due to a big reduction in grower selling. Producers there continue to protest the implementation of higher export taxes by simply not selling their wheat. This in turn may well see higher stocks in Argentina in the mid-term and may also put pressure on prices as they “catch up” and sell prior to planting. The IGC did increase Argentine ending stocks for wheat from 1.5mt to 1.7mt but keep an eye on this number going forward.