1/12/20 Prices

Cash bids for US grains out of the Pacific North West were flat to lower. White wheat held onto values while both DNS wheat and HRW slipped a few cents per bushel. Club white wheat with 10.5% protein was bid at US$248 FOB PNW, which on the back of an envelope equates to a number of about AUD$322 Newcastle port, or AUD$290 ex farm LPP for Jan / Feb slot.

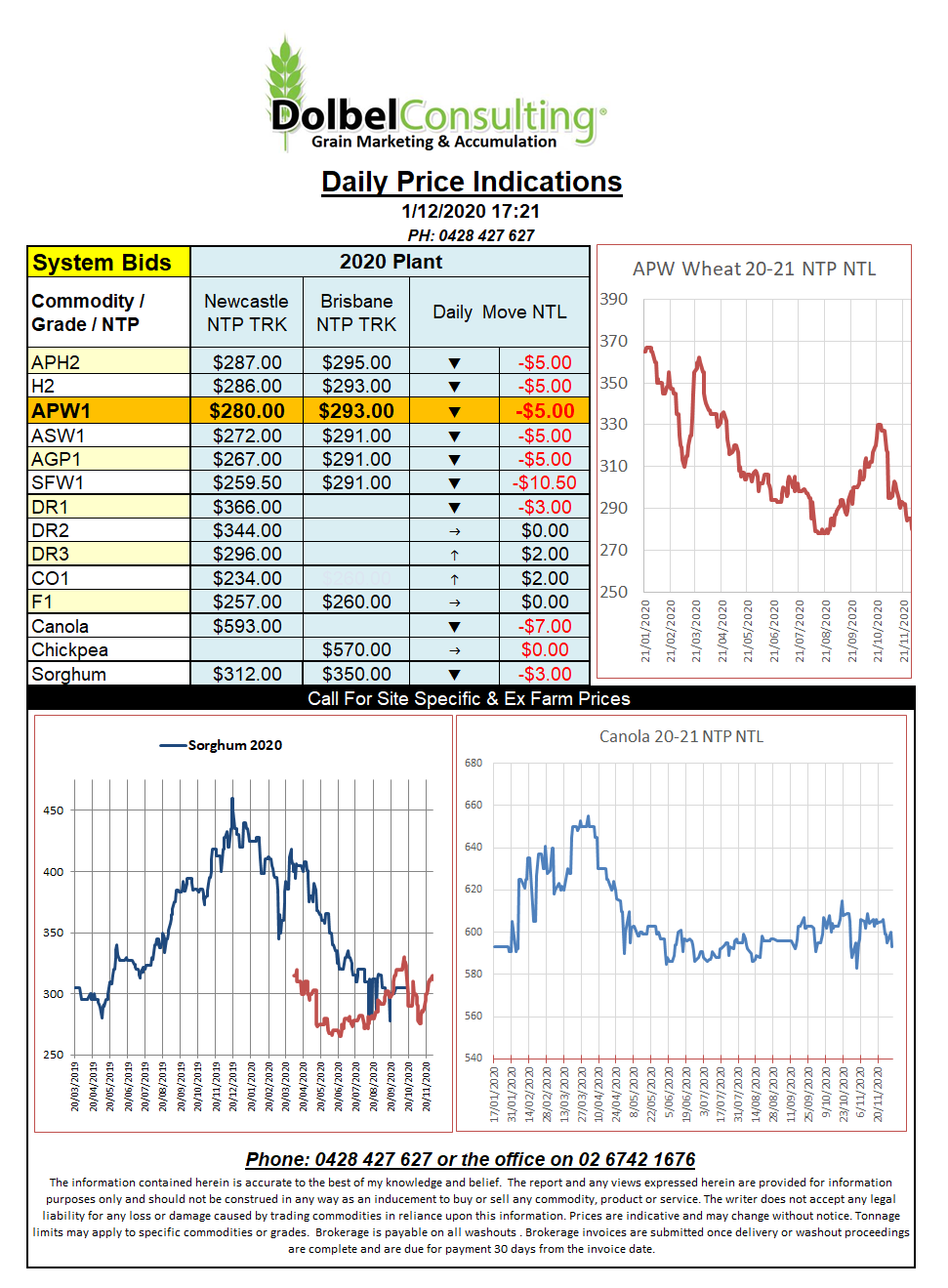

Looking at the Aussie APW1 FOB Platts futures contract at Chicago, we see it is still untraded, but closing at US$263.50 FOB for a Feb slot. This converts to about an AUD$284.55 ex farm LPP number.

Chicago wheat futures were sharply lower on the back of ……….. really good US weekly export sales numbers. Yeah sometimes futures markets don’t make a lot of sense. The pressure appears to be coming from both soybean and corn futures which when looking at the stochastic chart are both well over bought and due for a correction. The wheat stochastic not so much, the March SRW chart at Chicago would actually help you argue the case of stronger futures but the spill over pressure from the row crops is a major influence.

The latest ABARES report didn’t help much. There were some big increases in Australian wheat production. NSW production went from 10.26mt in Sept to 12.24mt in the last report. WA was the only state seeing a slight reduction. The increases take the national projection to 31.165mt. A slight increase over last year’s 15.16mt. The barley number still amazes me, now pegged at 11.96mt. Canola also higher at 3.7mt, this estimate goes some way to explaining the terrible basis being shown to the Aussie market at present.