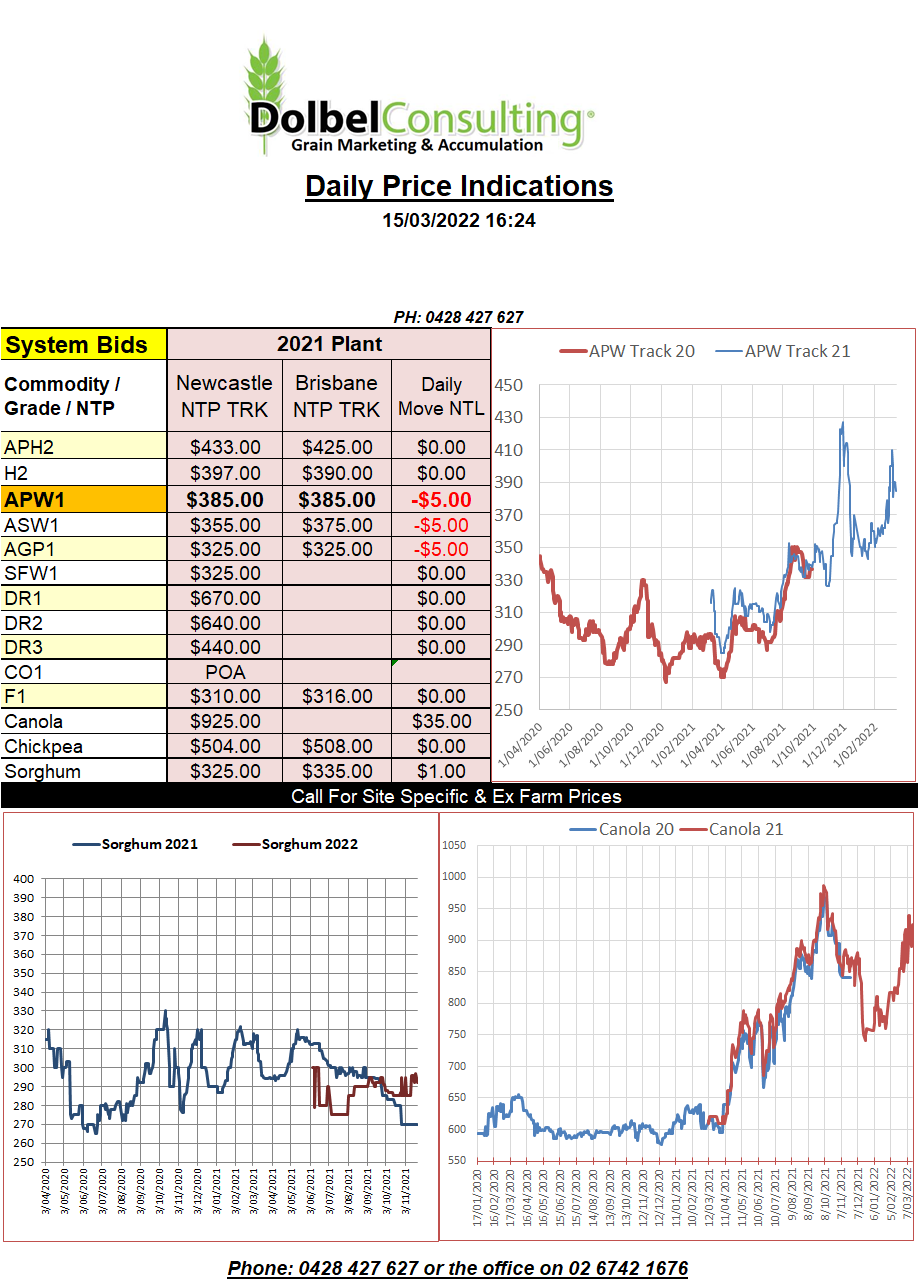

15/3/22 Prices

The Aussie dollar is sharply lower this morning, back 1.32%.

Talk of higher interest rates in the USA, the current inflation rate and low employment rate all key reasons to why they feel the need to grind the economy back into the dirt. When you do nothing but print money to fix a problem the side-affects eventually fester though, inflation is one such side-affect. I’m not sold lifting interest rates will fix this lack of supply driven inflation though, nor will shrinkflation. Usually more supply would fix a supply driven issues but instead they, the US Fed, will go about crushing demand instead through potentially collapsing buying ability. Seems counter-productive to me, why not stimulate supply production, time will tell. The bigger question is where do all those freshly printed notes end up?

I’ll stick to grain markets, the smoke and mirrors are slightly clearer and less distorted, sometimes.

Nearby corn futures at Chicago are back a little, soybeans are too. Chicago hard red wheat is mixed, old crop firmer, new crop softer. One could easily create a counter argument to that move given the dry weather in the US and the lack of exportable stocks from the PNW into Asia.

We see wheat values out of the Pacific North West of the US firmer across the board, Canadian old crop offers sharply so. 1CWRS13.5 bids ex farm SE Saskatchewan were up sharply, driven by higher FOB values.

Talk of Russia blockading Black Sea wheat exports through to the new crop have a few punters wondering about new crop carry in, two edged sword.

In the oilseed market we see nearby soybeans, canola and rapeseed taking a breather, back a few dollars across all three exchanges. The new crop values for both Paris rapeseed and Winnipeg canola closed higher though. Ukrainian Black Sea rapeseed exports remain suspended.