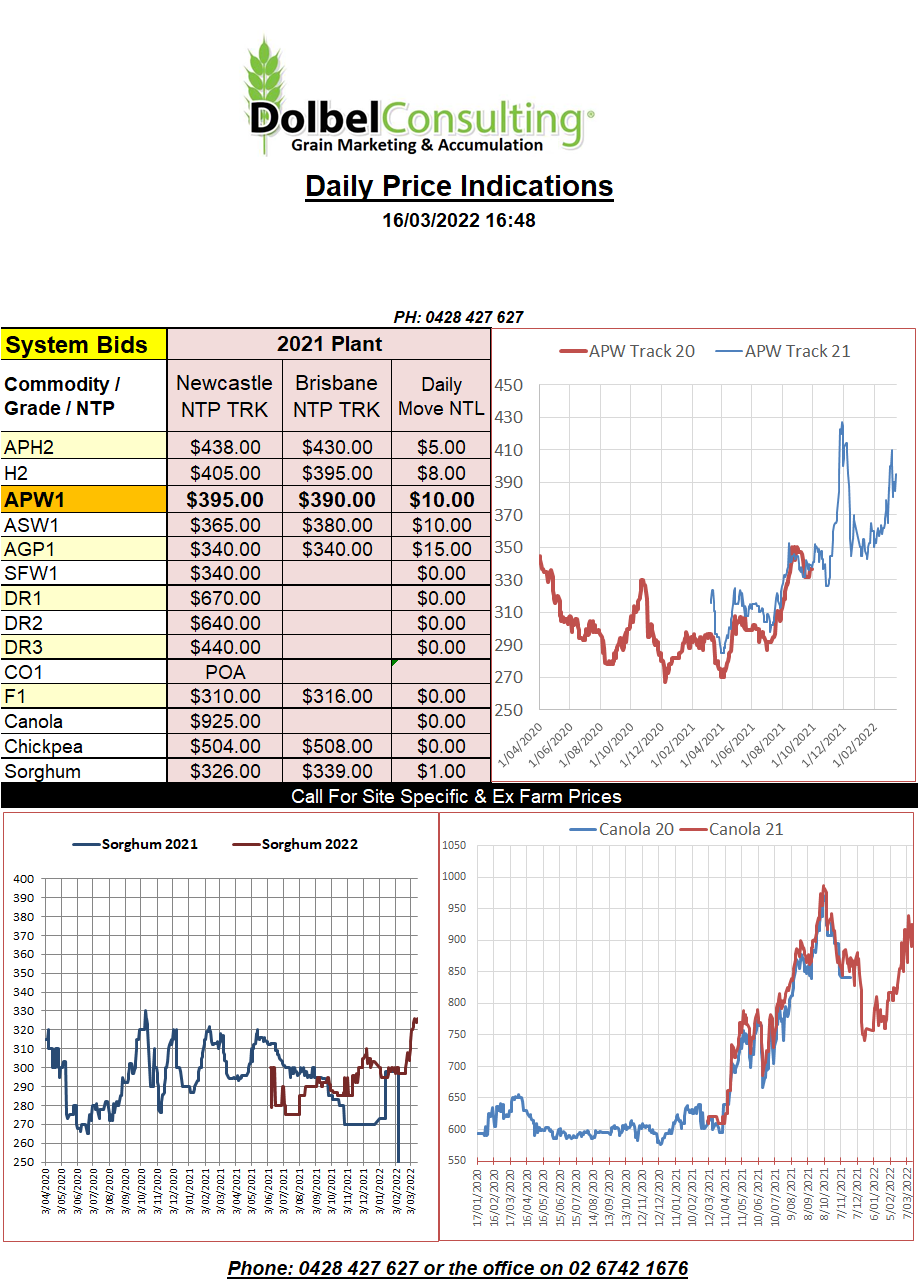

16/3/22 Prices

Covid is back in the Chinese equation again, it appears to be having more of an impact on their exports at present but was used as the catalyst for the sell-off in Chicago soybeans overnight. Not a massive fall lower compared to more recent market moves but with beans slipping away AUD$5.60 / tonne it wasn’t surprising to see nearby canola at Winnipeg slip a few dollars. Paris rapeseed was firmer on the nearby but fell away in all the outer months.

Wheat futures stole the show again, soft red winter wheat at Chicago putting on 58c/bu (AUD$29.60) in the May22 slot and 29.5c (AUD$15.05) in the Dec 22 slot. Hard red wheat futures at Chicago were also firmer, as was the spring wheat market at Minneapolis.

There are so many things feeding the wheat market at present it’s getting hard to keep track of. One commentary stated yesterday we are but one event away from a catastrophic issue in wheat supply. Nothing like a little dramatization to talk the book up is there. Regardless, any way you look at it the statement isn’t too far from the truth. Russia / Ukraine suspending sales. China confirming things are not as rosy as once believed and lining up for another covid fix. Dry weather persisting in the US HRW and spring wheat belt, where there’s not 8′ of snow. The realisation of a smaller S.American corn crop to add to feed demand and low opening stocks for many of the world’s major wheat importers. Lower production in N.Africa.

There you go, a paragraph like that should just about ensure a limit down move tonight.

The main driver for wheat was the Russian export ban announcement. The ban was followed by an official statement telling everyone to relax and not head down to the shops to horde food. These kind of statements are usually followed by people heading down to the shops to horde food.

Ukraine wheat area is expected to be back 39%, a combination of high abandonment, unsown area and loss of region.