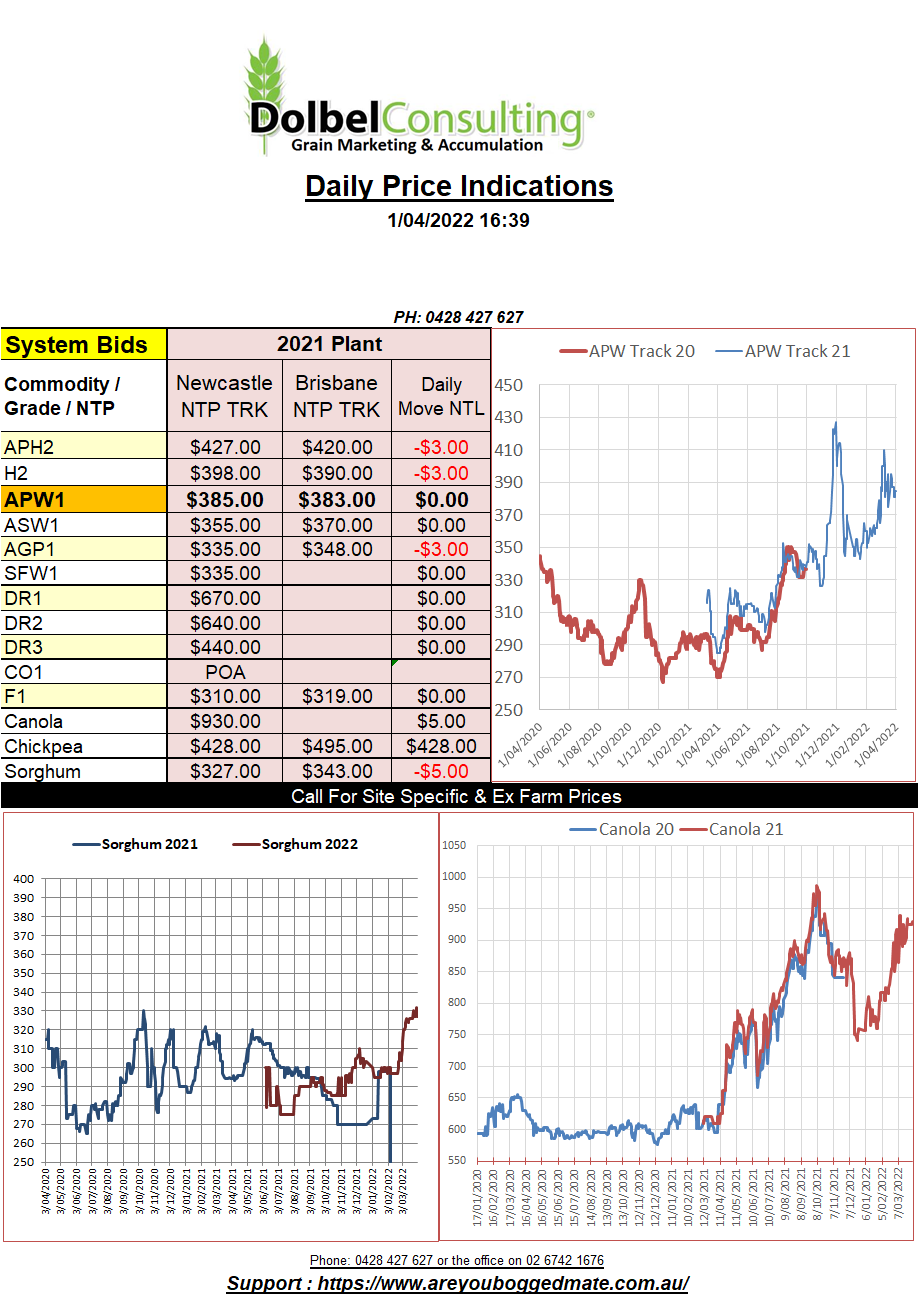

1/4/22 Prices

The USDA prospective plantings report, although a little predictable, did have an impact on US futures overnight. As expected by many the high cost of inputs for corn will result in some acreage swapping to soybeans, a crop that is a little cheaper to grow than corn and is currently seeing some good value. The reduction in corn area and the increase in soybean area saw futures for corn at Chicago climb higher while soybean futures there shed 45c/bu (AUD$22) on the Sept22 contract.

The move in Chicago soybeans futures didn’t have the impact one may have expected to see on the new crop canola market. Nearby futures for Paris rapeseed and Winnipeg canola were lower but outer month, for the new crop, were actually a little higher at both exchanges.

Wheat found support for US spring wheat futures as the USDA predicted lower than expected area to be sown to spring wheat. A bit of surprise given current values. The area under all winter wheat was confirmed to be a little higher though, triggering selling in both soft and hard red winter wheat futures at Chicago. The net all wheat acres for the US indicates an increase of 1% to 47.4 million acres. In saying this, it would represent the 5th lowest wheat acres since record keeping commenced in 1919. Although there is expected to be a reduction in total spring wheat area the USDA are predicting an increase of 17% in US durum acres, to 1.92 million acres. White wheat area is pegged at 3.62 million acres, this is a slight increase in white wheat acres from the 2021 prospective plantings report which pegged the area for white wheat in March 21 at 3.48 million acres.

Algeria picked up 570kt of wheat overnight. Traders guess values to be around US$37 less than their last purchase and valued at roughly US$448 C&F.