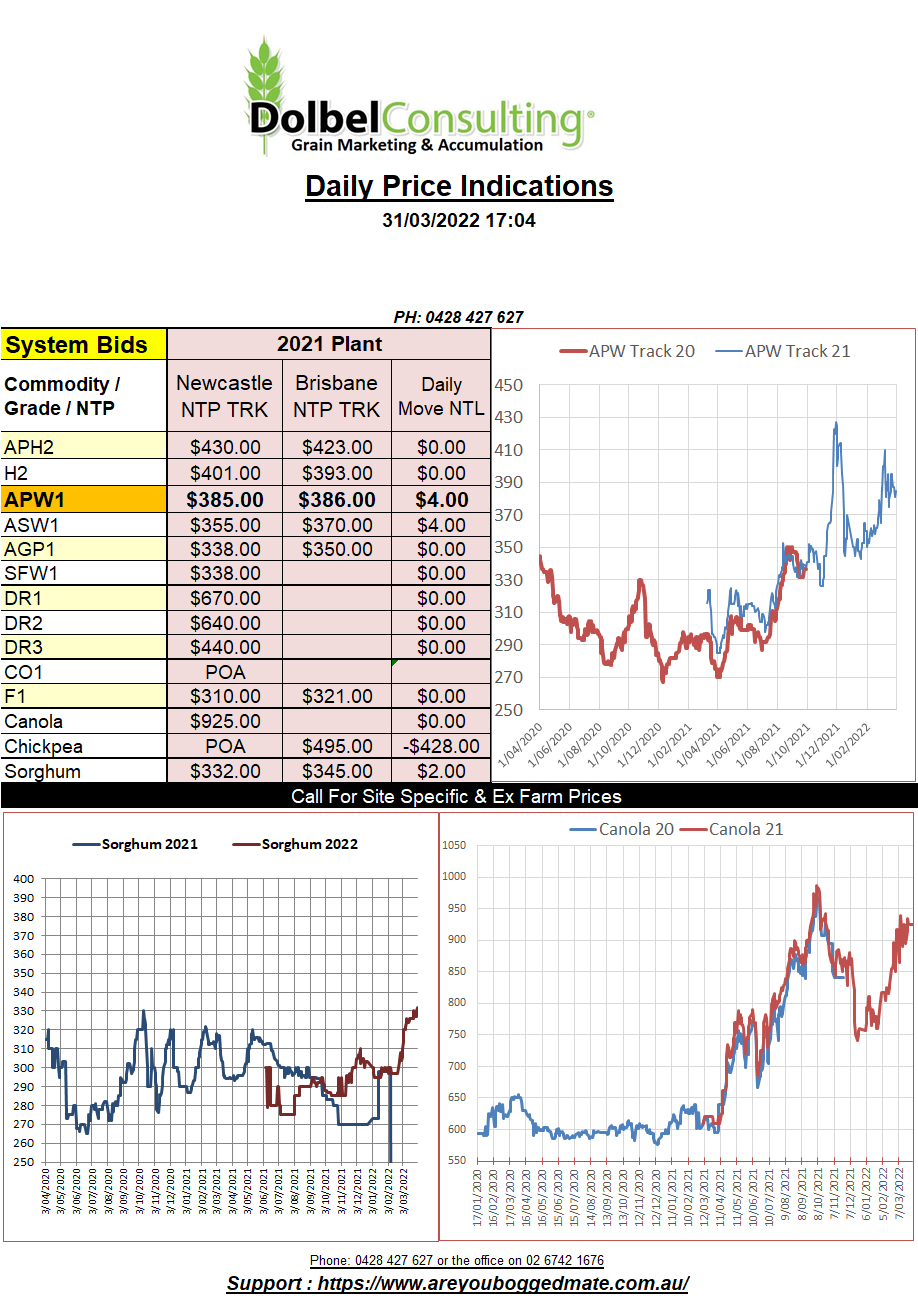

31/3/22 Prices

There is so much information coming from so many different directions at present it is very hard to glue it all together to determine a plausible outcome relating to grain production, consumption and ultimately price direction.

Demand destruction due to price increases, area adjustments due to drought, flood, and war. Shipping delays due to covid, war and vessel access due to the current “go slow” policies being practiced by some shipping companies to keep rates high. It’s the most complicated I’ve ever seen it, the ability to plot a clear path through the information and disinformation is truly time consuming.

The complex nature of today’s market is resulting in significant market swings. Overnight we saw US grain futures change direction again, pushing higher across the board. Corn, wheat, and soybeans at Chicago all closing in the green. Some reports claim that after the recent decline bargain hunters entered the market last night. Others claim that the move higher was simply positioning prior to the USDA Prospective Planting report due out tonight. It is indeed the “silly season” in the grain markets, with an extra dose of madness.

Fertilizer prices are the big talking point in the US (everywhere). The impact fertilizer prices will have on corn acres has been a big talking point of late. Some online surveys indicate that area will not be swayed by the price of inputs. The current value of corn still makes it more viable than some alternatives. Maybe the swing will come in more marginal areas, like the Canadian spring wheat belt or the borderline soybean regions in the USA.

Tunisia picked up feed barley at US$442.68 C&F. On the back of an envelope this would equate to an ex-farm Liverpool Plains price closer to AUD$400 than AUD$300. The global feed market remains well supported and Australian feed grains remain the cheapest on offer into many locations.