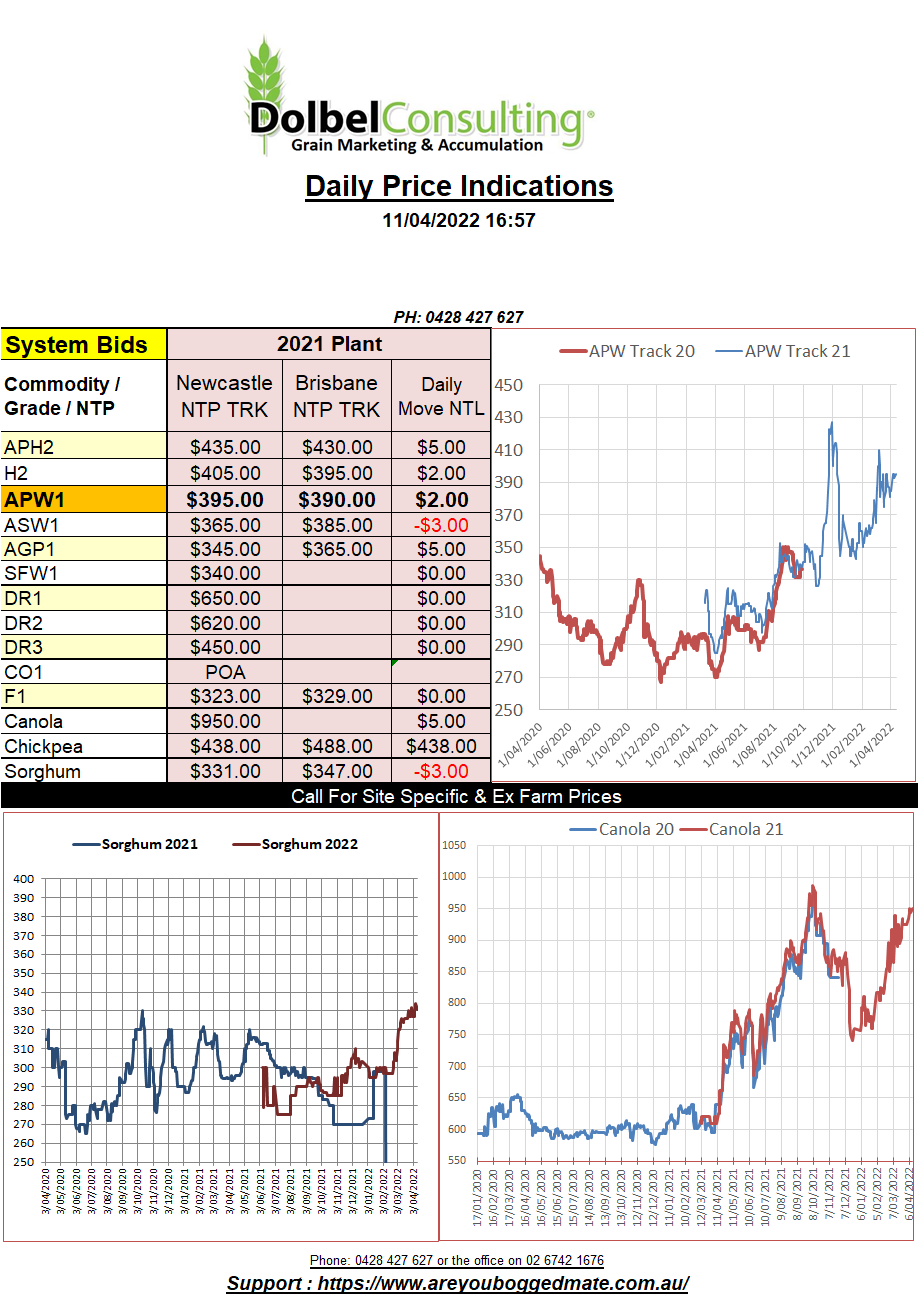

11/4/22 Prices

The USDA WASDE report for April was out overnight, almost sneaking under the radar with everything else going on at present. The report was generally bullish, pouring a little petrol on an already smouldering market. The USDA confirmed their thoughts that world corn stocks will climb a little this year as exports are reduced. Ukraine exports of corn were pegged at 27.5mt in last month’s report, this month they have been reduced to just 23mt.

World corn production was estimated at 1210.45mt, just under 4mt higher than last month and basically rolling straight through to a similar increase in ending stocks.

Sharply higher closes for both wheat and soybean futures at Chicago were initially fuelled by the same fundamentals that we’ve seen push these markets around for a few weeks now and then later in the session by the WASDE report. Canola and rapeseed futures did close higher but failed to follow the soybean markets higher dollar for dollar. It was interesting to see soybean production reduced in Brazil by 2mt to 125mt while also reducing exports, the nett result an increase in carry out. Interesting to see Chinese imports were also reduced from 94mt to 91mt, while US exports were increased by 680kt.

Wheat futures at Chicago, Minneapolis and Paris all closed higher. The weaker AUD isn’t going to hurt the conversion any on Monday either. The USDA report reduced world carry out by 3.09mt to 278.42mt or excluding China -3.1mt to 136.25mt. Australian numbers were left unchanged, Argie was up 500kt in production to 21mt, not a bad effort considering their season. Interesting to see Ukraine exports only reduced by 1mt to 19mt and Russian exports actually increased by 1mt to 33mt. Chinese imports were left unchanged at 9.5mt. I thought this may have been as high as 12mt by now. Indian exports were also left unchanged at 8.5mt, some were punting that number to increase a little as it replaced Black Sea wheat into some locations.