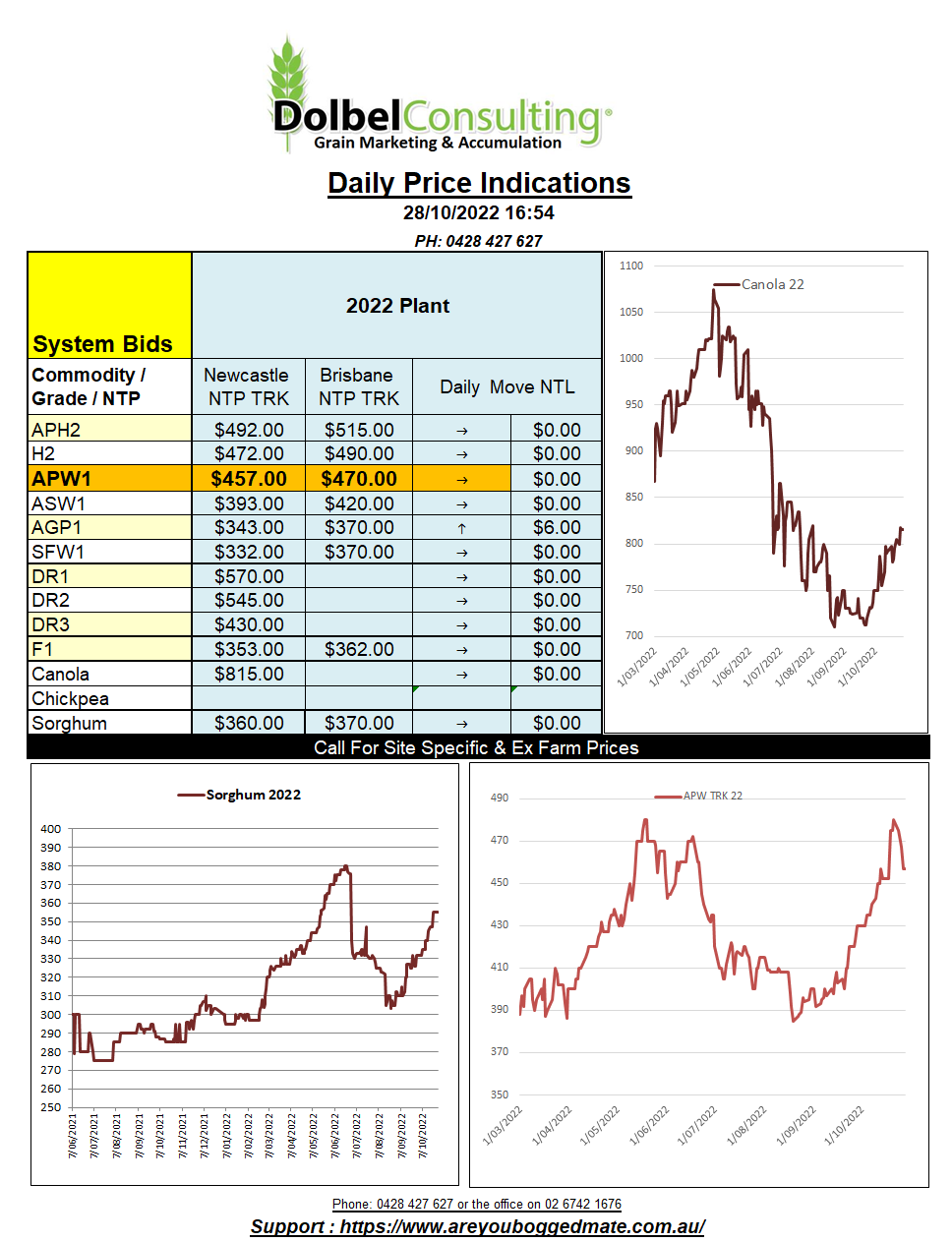

28/10/22 Prices

Interesting to see Canadian 1CWRS13.5 milling wheat and US white wheat values higher out of the PNW. If I was an Asian buyer of white wheat, particularly Prime Hard white wheat, I’d be trying to cover my long-term supply needs ASAP. With reports of low protein and low falling numbers coming out of SE QLD, and severe flooding across N-NSW, supply of higher-grade white wheat will become very tight.

Quantifying losses from recent heavy rain and flooding in Australia remains difficult. The most advanced crops were north and west of Narrabri where the worst flooding has occurred. Before the flooding wheat production estimates out of NNSW were roughly 3.95mt. Some private estimates have losses at 30%, so potentially 1.2mt. There is also grade and test weight to be taken into account for the balance of the crop north of Narrabri. This could leave potential crop losses closer to 2mt for wheat just in NNSW. This doesn’t consider crop losses in other catchments which have also seen a very wet spring and lots of flooding.

Wheat production estimates for Argentina continue to fall. The latest projection from the Rosario Exchange is 1.3mt lower than their previous estimate in September. At 13.7mt, we should start to see Argentina begin to reduce export projections. Domestic consumption is about 7mt.

Algeria picked up 80kt of milling wheat in their latest tender, the price was said to be around US$381 C&F. The Algerian business roughly converts to an ex-farm LPP price of something close to AUD$400.

US wheat futures continue to drift lower as export volume remains poor.

Pakistan remains in negotiation with the lowest offers from their recent wheat tender. With world production estimates generally slipping lower this is probably not the best strategy I’ve seen in recent weeks.