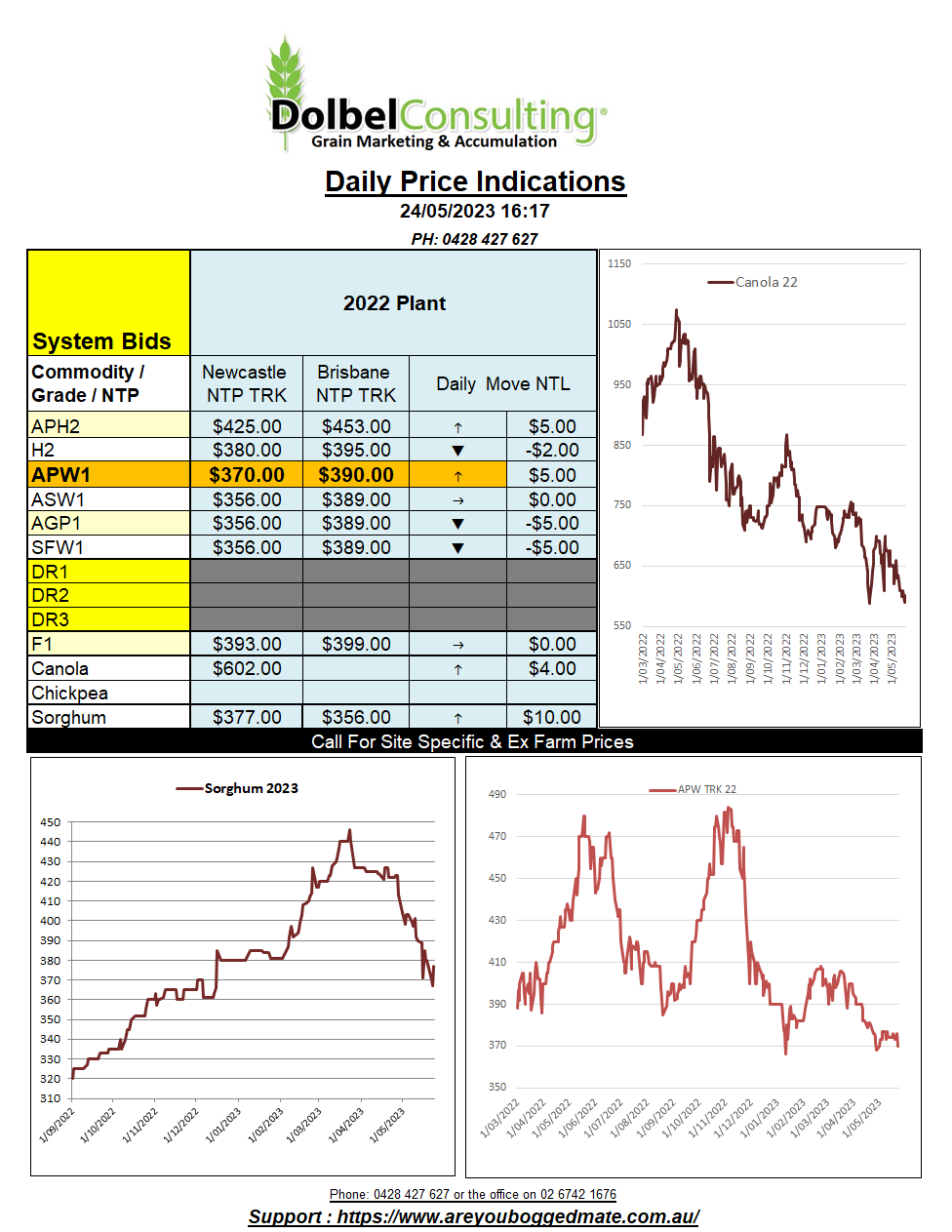

24/5/23 Prices

It’s hard to talk the wheat market up at present, this time last year we had the Russian invasion of Ukraine blocking Ukraine exports out of the Black Sea and the “world was going to starve”, India was going to save the day, that went pear shaped. Then the world was saved when the Black Sea grain corridor deal was struck, just after the major punters got short wheat, and that’s pretty much been the trend for a while now. Truth be told the world was never going to starve, world wheat stocks were healthy, regardless of what was coming out of Ukraine.

This leaves us trying to find some light at the end of this tunnel the market is trying to force us down. World stocks are projected lower even with average crops predicted in Argentina and Canada this year. Currently world stocks are estimated to close at 264.30mt in 2024, back 1.9mt. China still “own” 139.7mt of that estimate.

If you take Chinese stocks out of the market, their stocks will never be sold anywhere other than China, and China has been a net importer, even as their production grows at the ever constant rate. Once you take Chinese stocks out, you come up with 124.7mt. That’s actually the lowest ending stocks number for the world less China since 2008-09. Less than half of that is held by the big five exporters. The major exporters are pegged at just 55.7mt, that’s a fall of 7.6mt year on year, that’s a lot.

With southern hemisphere wheat and northern hemisphere spring wheat far from being a stable known, there is still plenty that could move this market. The continued dry weather across N.Africa, serious drought in Spain, wet weather in Italy. Lingering dry spots in Cordoba, Argentina and the HRW crop final production number in the USA, just to name a few. Throw into the mix the high level of uncertainty we are seeing in political arenas around the world and the drama facing the currency markets and there’s potentially a light out there in the distance for those with a wheat crop in 2023-24.