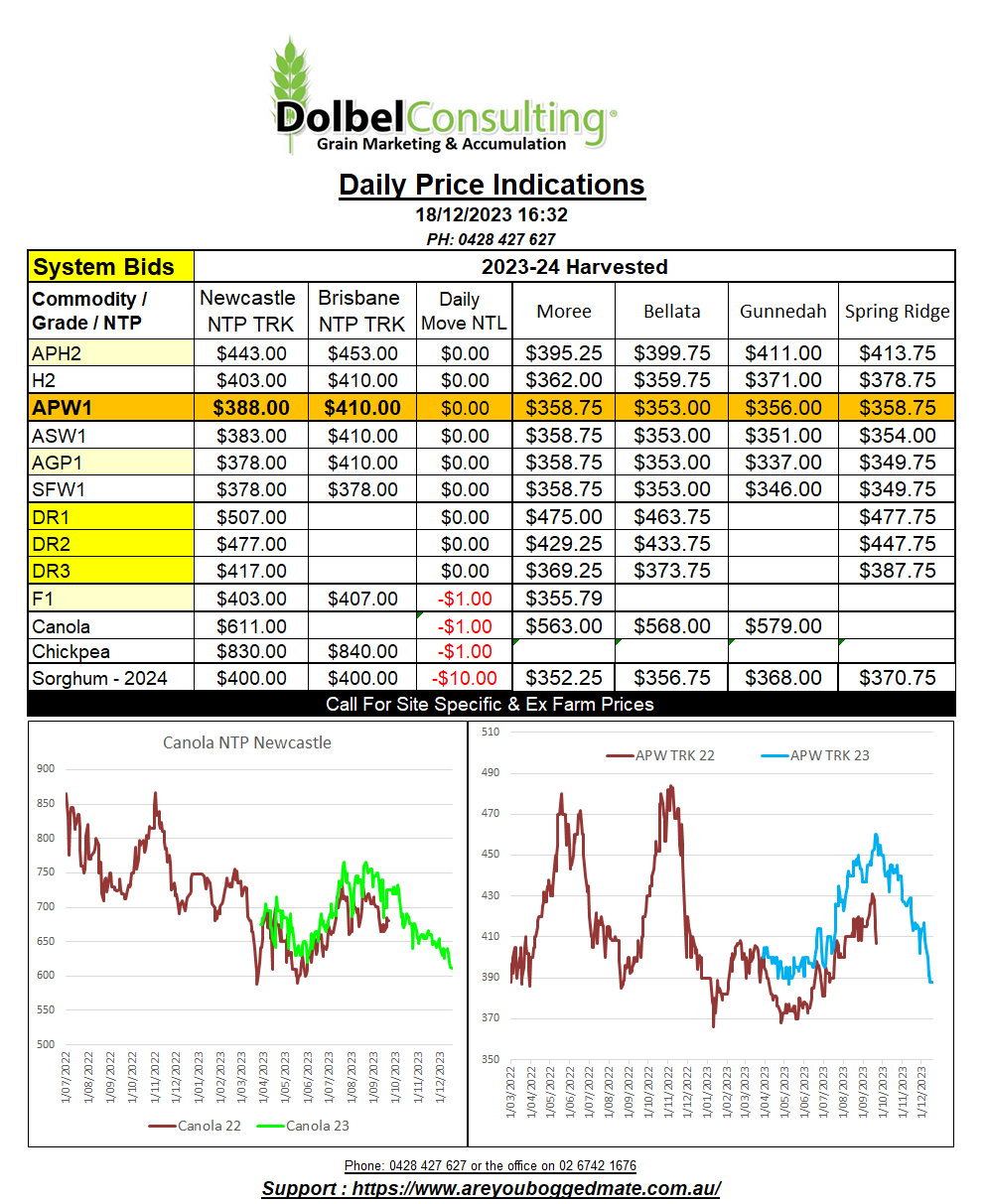

18/12/23 Prices

All the headlines for the local economy read like something from a Stephen King novel this morning. Do we sit back and wait for Michele Bullock to chop the bedroom door in with an axe, peering through, screaming “I’m back” while slashing interest rates…….. I sure do hope so…. I mean, we’ve all seen pictures of her, so this is entirely a metaphor.

The crux of it is, every economic headline I’m reading is talking about the “failing housing market”, the “immigration nightmare”, “households to batten down the hatches in readiness for a recession”. I mean, what kind of a rock have these ……. people been living under.

Now armed with all the fear of the media, do we forecast an AUD of 60c in the new year or 50c. Do we watch as global rates fall in unison, countering the impact of the first to fall, who knows. 2024 may yet be the year of the economist, more than the year of the grains analyst, but I’ll continue to punt.

The December contracts rolled off the board at Chicago. March SRWW futures there found some support, outer months a little more support. There was spillover support for both Kansas wheat and Minneapolis wheat, the later less so. White wheat values out of the US PNW were flat again overnight. The WW market hasn’t changed much at the FOB level out of the US into Asia much this week.

It’s been a big week in the international grain game. Confirmation of big wheat purchases from China, Algeria, Egypt and Saudi Arabia over the last fortnight has shown the wheat market that the price is right for the consumer. There’s been some speculation that French winter wheat production will be lower as the last of the crop will not be sown thanks to wet weather. It’s been abnormally wet in Ukraine. India has seen some unusual winter rain, not great news for chickpea sellers here. Chickpea values at the Delhi market have trended lower since late November, the AUD assisting the fall this week.