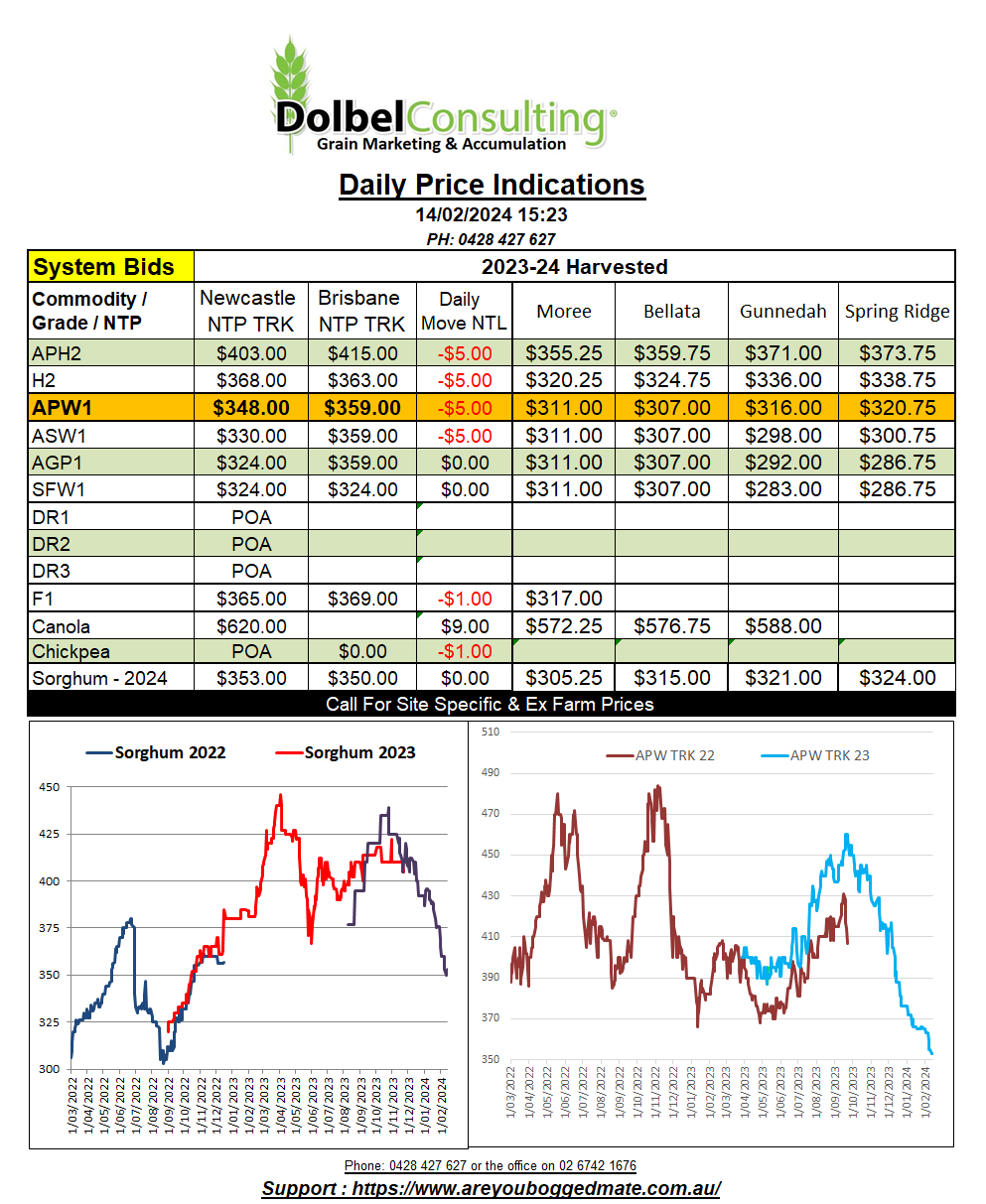

14/2/24 Prices

| International futures markets were quiet overnight. The main mover was the oilseeds market, both canola and rapeseed futures closing higher, helped along by talk of poorer yields in S.American soybeans and lower palm oil production in Asia. The move went against the flow in Chicago soybean, probably feeling the weight of the stronger US dollar and slow export pace of US product. Spring wheat futures, and cash values for US spring wheat out of the US Pacific Northwest were a little lower, the premium grade shedding the most of the main three wheat grades in the states. There wasn’t a lot of international news that was there to help values last night. Reports from the Ukraine ag ministry suggesting a 9% year on year reduction in corn area was probably a little bullish. The smaller than expected palm oil production out of Asia was good for oilseeds. Some lower production estimates for Brazilian soybeans were also on the wires. Some punters now calling production there sub 150mt, still huge, but not as huge. Russian wheat exports for January were slow and February exports are expected to come in between 2.8mt – 3.2mt, which is pretty much bang on the 3mt exported in February last year. Russian exports have been a little slower than the trade had hoped to see for a few months now. This will simply roll across to a higher opening stocks number for the new crop S&D, and will continue to weigh on world wheat prices moving through the second half of 2024, unless we see some production issues during the N.Hemisphere spring. |

||||||||||||||