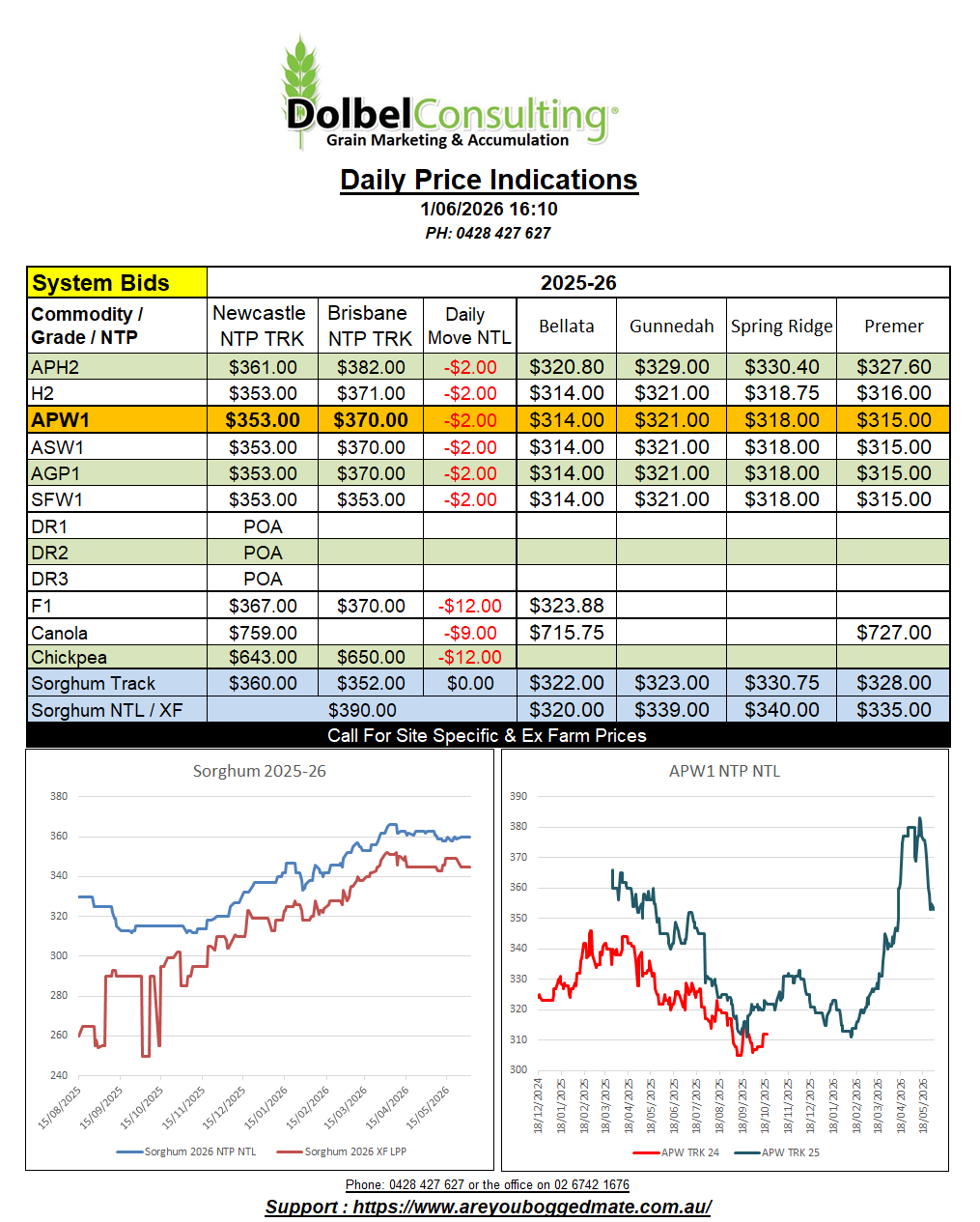

01/06/26 Prices

The market wires are telling us that the pressure on grains is coming from lower crude oil futures this morning. Talks between Iran and the USA will be crucial in determining the future direction of crude oil, but at the moment the punters can see an end to war and the return to free flowing oil out of the Straight of Hormuz.

Trump will likely stand back and congratulate himself for ending the war he started. What ever your view is on Trump, one can only determine if the war had more to do with oil than it did in stopping the mass murder of Iranian citizens wanting to be free from religious rule, as time goes on. I think we all know the answer to that, but lets hope for a less brutal future for all Iranians.

Unsurprisingly the French government reduced the Good / Excellent rating for the soft wheat crop, down 3pts to 78% G/E.

US wheat export sales saw roll over into the new crop marketing year, old crop a negative, new crop quiet high, the net result an unimpressive 250kt of sales. Corn net sales were OK, soybeans, not so much. Net sorghum sales were 66kt, 3kt of that was confirmed to be China, the balance was unknown, so probably China. C&F China values for sorghum were generally a little lower once converted to AUD/t, a combination of softer US FOB prices and the stronger AUD.

Reuters reported that Brazilian wheat imports are expected to rise in 2026-27 as their sown area recedes. The report suggests that a lower quality Argentine crop may see Brazil look towards the US for better quality milling wheat. Possibly acquiring up to 1mt-1.5mt from non S.American suppliers. Brazil sow their wheat crop in April / May / June, harvesting in Oct / Nov / Dec. This may be optimistic thinking for US suppliers. Although Argentina had a lower quality crop, they also had a record crop, allowing exporters to not only sell lower grade wheat into Asia, but also potentially supplying Brazil with the milling wheat they need.