1/12/23 Prices

Taiwan picked up 109kt of US milling wheat by tender yesterday. Grades were mixed, 34.2kt of dark northern spring wheat traded at US$336.57 FOB US, roughly comparable to US$374.51 C&F. The trade also had 14.8kt of HRWW, 12.5% protein at US$327.67 C&F and 5.7kt of soft white wheat at US$306.64 C&F change hands. This consignment of the tender, the first, is due for arrival 2nd half of January 2024.

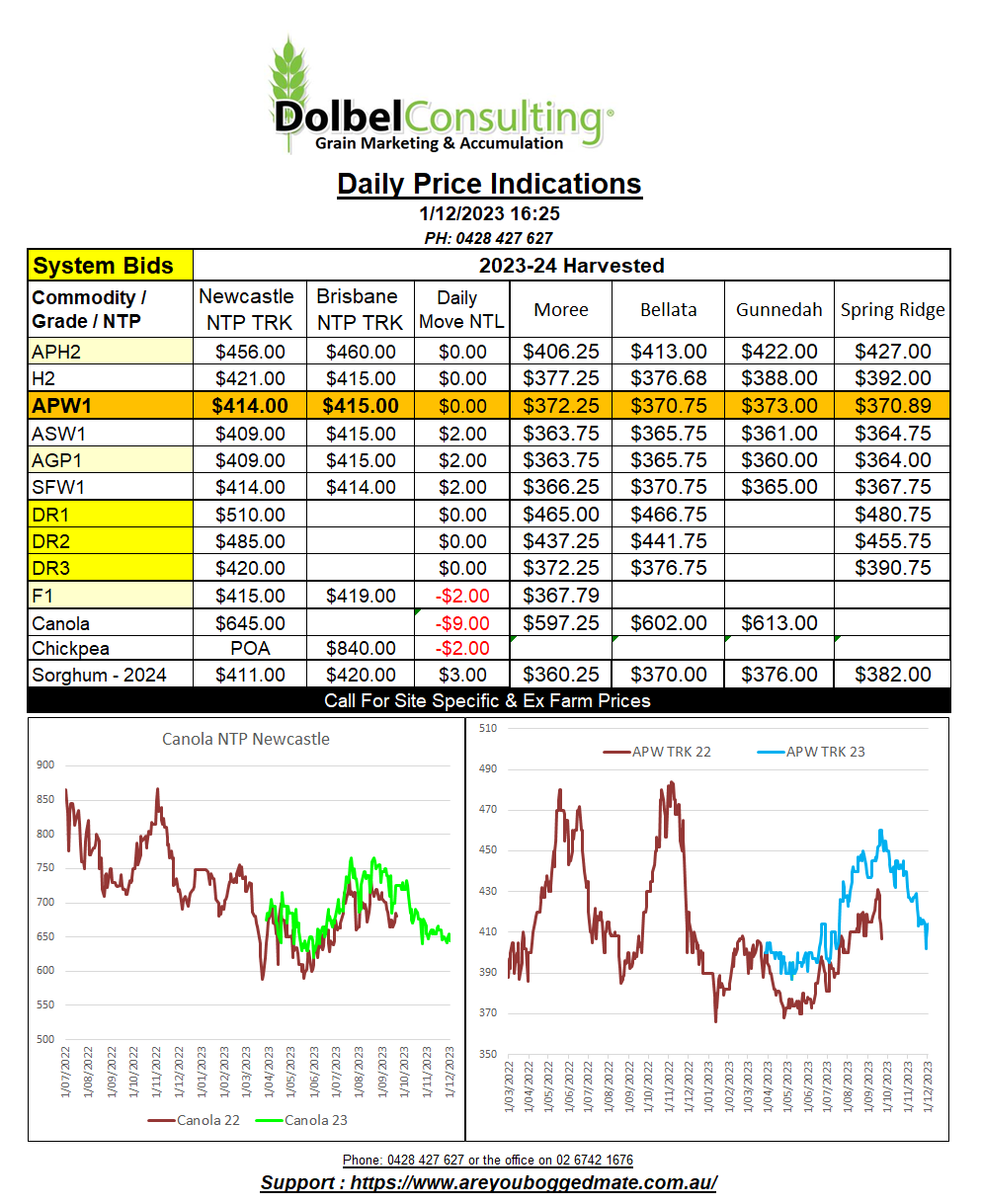

Comparing the value of the HRWW to local H2 prices here we see that the US wheat converts back to a number close to AUD$402 ex farm C-LPP, potentially confirming that the recent decline in local values simply put NNSW wheat back on the export plate, prior to the slight move higher in local bids late this week.

Reading of a few private punters lining up for a sell Chicago soybeans / buy Chicago soft red winter wheat trade. I’m no punter but soybeans have looked over priced for a while, and wheat is oversold, if not cheap. It’ll be interesting to see if they make any money in the mid term. Wheat futures at Chicago are massively oversold by the funds. At some stage one would assume this will need to be cleared. Will it be in an orderly fashion, potentially during the roll in Jan / Feb, or will it be in a panic on the back of a northern hemisphere scare during the spring thaw. They call it punting for a reason.

US weekly wheat sales came in better than expected and well above previous weekly sales. The data helped the Chicago market higher but the bigger picture still indicates that the US need to see a few more big weeks, like last week, to catch up to the current USDA projections.

Both Paris rapeseed futures and Winnipeg canola closed lower. The move may be slightly buffered by the weaker AUD but Paris will be hard to ignore.