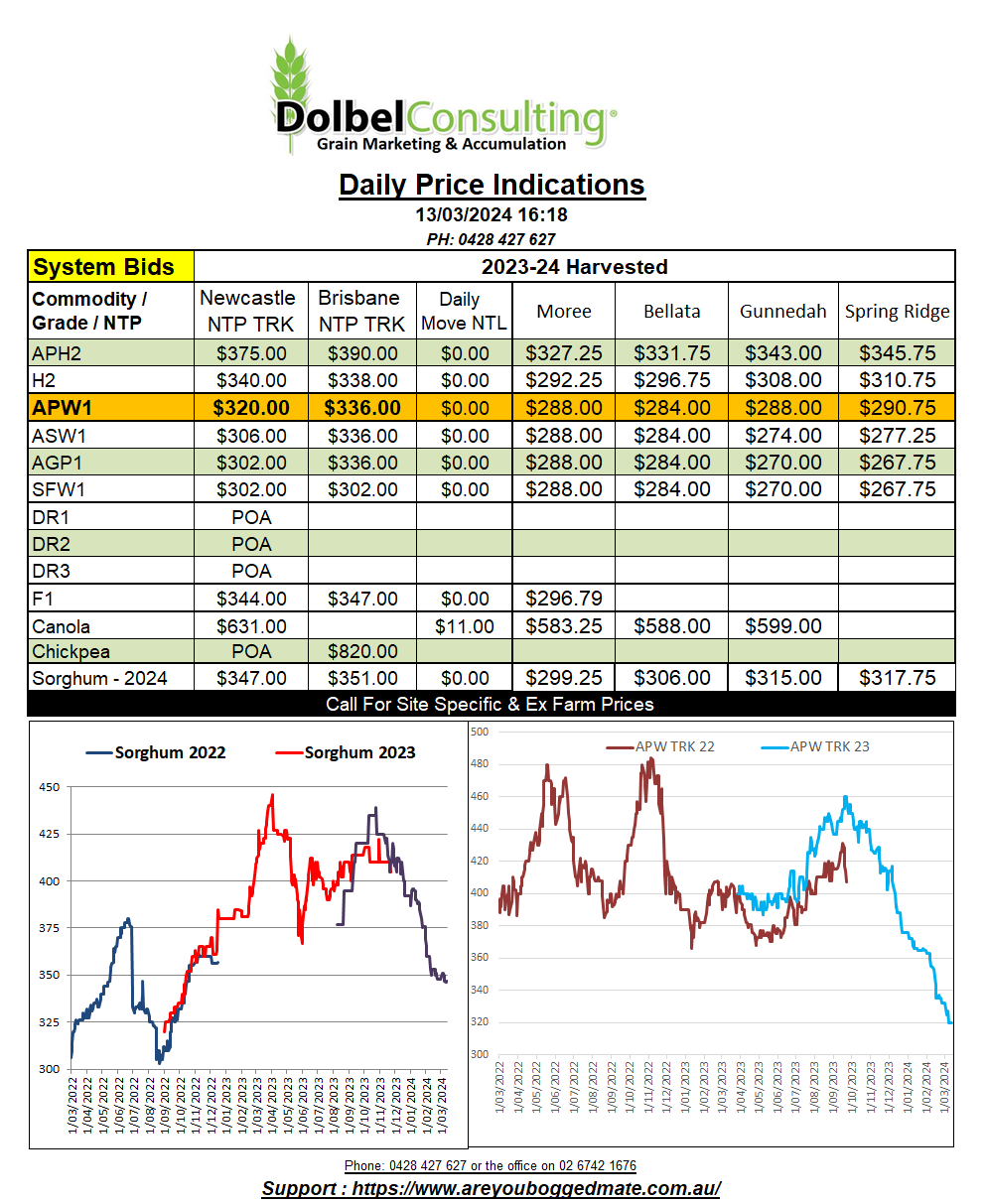

13/3/24 Prices

I don’t think I’ve ever seen the 5 nearby corn contracts at Chicago all close unchanged before. It’s not like there was a lack of volume in the May contract either. Approximately 121,994 contracts changed hands, that’s 15.24mt, in a range of just 7c/bu. Some reports assume that without the spillover strength from the soybean pit than corn futures may well have closed lower. Fundamental support may have come from a slightly smaller second plant estimate from Brazil.

Chicago soybeans closed higher. Production issues for canola in Europe and India and lower acreage projections for the spring sowing of canola in Canada all offered fundamental support for canola. Paris rapeseed futures closed higher, up E13.25 on the nearby and E11.75 per tonne in the Feb25 slot, there’s just E5.75 carry between the Feb25 contract and the nearby contract at Paris. So if you think you can make money from current values use that number in your budgeting.

Winnipeg canola futures were also higher, rallying C$12.00 nearby and C$13.00 in the Jan25 slot. Cash bids ex farm SE Sask didn’t reflect the futures market dollar for dollar but did close higher across the board for both old and new crop. Durum values ex farm SE Sask were unchanged.

US wheat futures were generally a touch lower, also showing minimal volatility. Values FOB Black Sea are mixed, Ukraine a little lower and Russian values appear to be a little higher. News that China has cancelled a bunch of US wheat orders and rumours that there are more cancellations to come appeared to be overlooked at the futures market and for cash values out of the PNW. China will likely take hedge profit on these cancellations and may re-enter the physical market again to pickup more wheat to help cover the poor quality of the 2023 crop there. Keep an eye on Indian quality reports over the next 60 days.

Hard red wheat and spring wheat values out of the PNW were flat to firmer but white wheat values were a tad lower in USD.