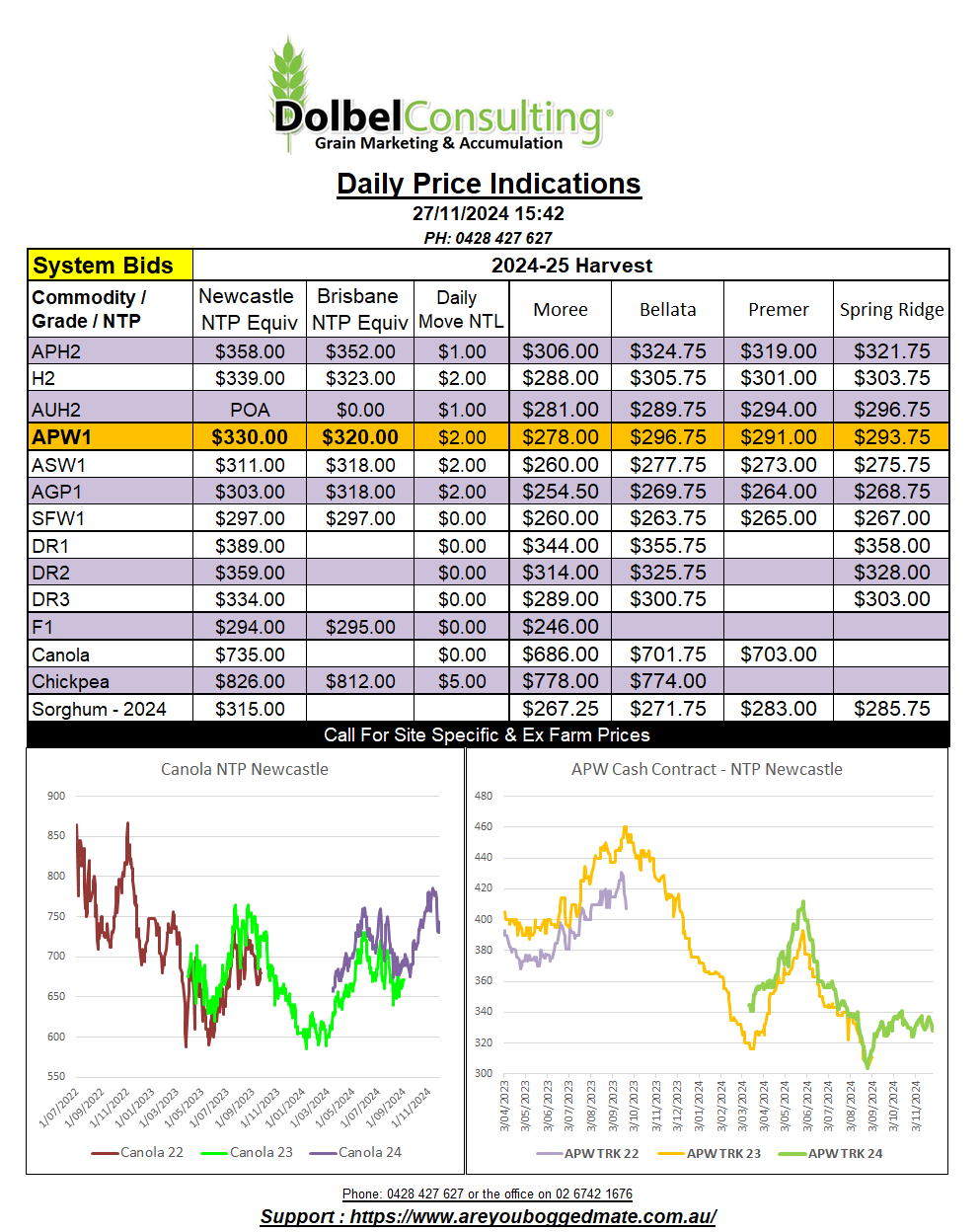

27/11/24 Prices

International Commentary

US wheat futures made some progress higher last night after falling for three of the last four sessions. Paris milling wheat futures also closed in the green, up €2.00 in the December contract and €0.50 in the March slot. Cash wheat values out of the US Pacific Northwest moved higher by AUD$2.00 to AUD$5.00 compared to yesterdays conversion. Canadian spring wheat futures followed US values higher.

Tunisia are in for 100kt of durum, the tender will closes tonight so we should have some numbers tomorrow. Maybe they are getting in while prices are low. The last Algerian tender did surprise a few sellers, cheaper than expected. Looking at current durum values in both France and Canada and converting those values to an Italian C&F price and then converting those values back to a delivered Newcastle port estimate. We tend to confirm that after the sharp losses here over the last week current local bids are midway between both French and Canadian values. This should place Aussie durum in the mix for any business into that part of the world.

Canola and rapeseed futures continued to trend lower after a nice reprieve yesterday. The saying penthouse to outhouse comes to mind. Both rapeseed and canola appear to break away from the influence of soybeans and palm oil last night. Nearby soybeans at Chicago were lower by 2.25c/bu, outer month firmer, but palm oil was up 29 nearby (AUD$10.06/t).

Jordan picked up 60kt of wheat from Cargill at US$268.90 C&F. Tender values ranged from as low as the Cargill offer to US$285.

The AUD is back under 65 US cents this morning. The punters appear to be factoring in more upside in the USD while their also appears to be a growing consensus that the RBA will drop rates here in Australia in December. I’m not 100% sold that they will do this, if they do, we could see a very low AUD by Jan.

Domestic Commentary

A sharp increase in local feed type wheat (ASW / SFW1) offers yesterday saw local bids tested but managing to hold on compared to the track milling wheat market which actually slipped $2.00 to $4.00 on the day, the lower grades holding on better.

ASW wheat changed hands for Jan / Feb pickup, at $305 XF SE LPP, destined for the Newcastle consumer market at $340 delivered.

ASW1 into the Tamworth consumer market saw buying interest from the trade for Nov / Dec at $310, or $320 for a Feb / March slot. The slots into both Tamworth for ASW and SFW1 for the Liverpool Plains feed lot markets are starting to fill up. Many buyers now only bidding for Jan / Feb / March, buyers call, we all know that means Feb / March.

AUH2 moved into the Newcastle export market at $348 delivered prompt. This market has been very mixed over the last few weeks and the level of bid greatly depends on the protein. Most exporters looking for some higher protein, 14% to 16%, to blend will lower protein APH2 or H1 type wheat for export. The spread for prompt H2 into the port and the lower grade AUH2 was $10 by the close of business, +$20 from AUH2 to APH2.

Canola clawed back $14.00 on the track, reflecting the entire move in Paris rapeseed futures, this was not expected. With the market trending lower I was of the view that some basis may have been eroded. With a lower close at Paris last night, the day to day conversion comparison is back AUD$7.74 / tonne. There may be a few traders that had of wished they built in a little basis buffer.