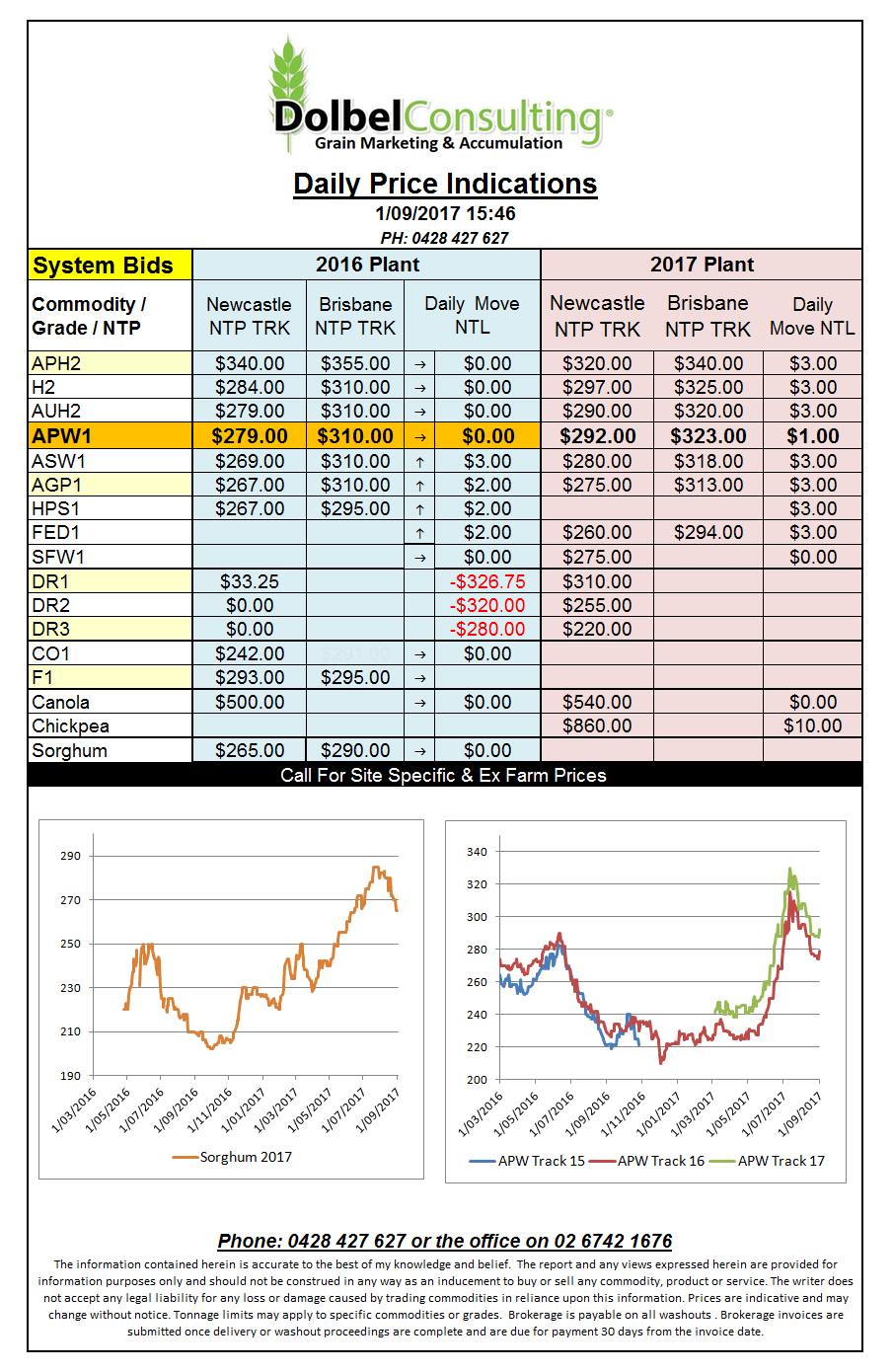

Prices 1/9/17

US futures closed August on a weekly high but August as a whole was a shocker. Nearby futures for SRW slipped 51c/bu for the month of August, almost AUD$24 / tonne.

Last night saw US soft wheat and hard wheat futures close higher on the back of a rally in corn futures. The combination of a weaker US dollar and good weekly export sales by the US saw corn futures improve by 12.75c/bu, a little over AUD$6.00 / tonne by the close. The AUD gained against all the majors and will probably counter a large slice of any potential move higher today.

The elephant in the room was spring wheat futures which closed over 14c/bu lower (AUD$6.50). The StatsCanada report came out with a Canadian spring wheat estimate of 18.89mt, a little higher than the trade was expecting. Although down 7.7% year on year with average yields falling 20% – 30% in major areas, the trade was expecting worse from the drought stricken S.Saskatchewan region.

The report did have a few positives though, especially for durum growers. With a production estimate of only 3.98mt it is half of last year’s production and around 1mt lower than the average trade estimate.

This decline in Canadian durum production backs up IGC data which recently reduced world production by 3mt to 36.9mt and suggested a significant tightening from the supply side. The IGC did peg Canadian production at 4.5mt in that report.