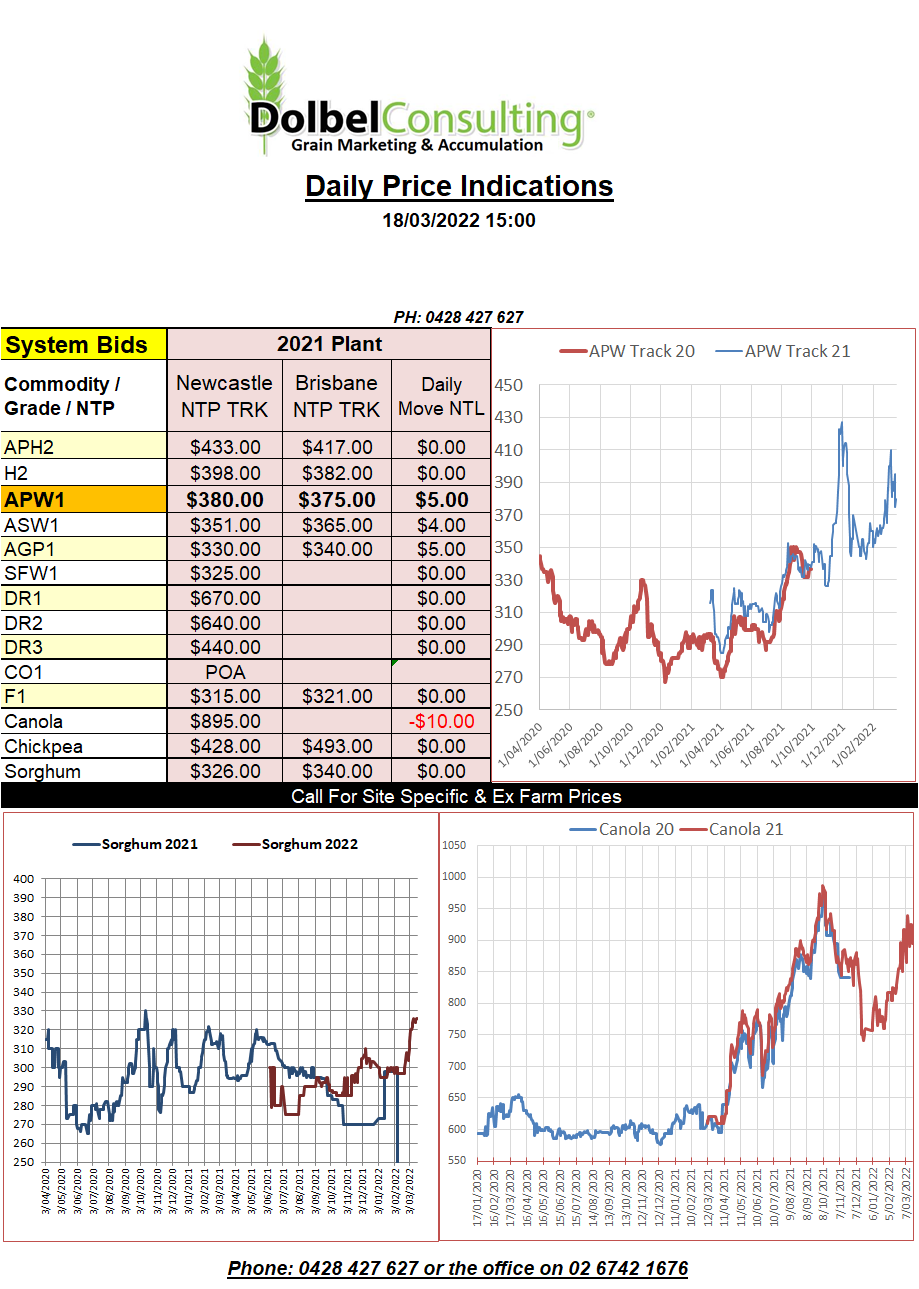

18/3/22 Prices

The punters are backing the RBA will follow US interest rates higher. Will this cool inflation or will it simply hammer a few more nails into already struggling businesses. With unemployment rates in Australia at a 13 year low in February, the punters may not be far off mark but from a retail perspective I can confirm that March has not shown anywhere near the level of confidence February held.

A jump to soon is going to hurt Australians and with an election just around the corner one might assume there will be some pressure for rates to remain unchanged for a month or two yet.

The downside to all this is the jump in the Aussie dollar, climbing from 0.7179 at the beginning of the month to close at 0.738 this morning.

The jump in the value of the AUD against the USD will counter last night’s rally in US wheat futures by about $6.00 and almost $7.50 for canola.

Turkey picked up 270kt of milling wheat overnight, offers were said to have been around US$445 – US$450, with business being done averaging around the US$445 mark C&F. The price reflects pretty much the values that Turkey walked away from in their last tender.

There was also talk of India selling 210kt of feed wheat into the Asian market. With internal values in India kept high by their minimum support price program wheat there rarely makes it to export. This has lead market analyst to assume values would have to be in the vicinity of US$345 FOB to make this happen. If this is the case we would see Indian wheat moving into Asia at something like US$370 – US$380 C&F. A price roughly comparable to over AUD$400 ex farm LPP. Confirming Australian SFW1 wheat at current values is still the cheapest wheat Asia can buy.

Export volumes of wheat out of both the US and the EU over the last fortnight have not been great, high prices killing demand quickly.