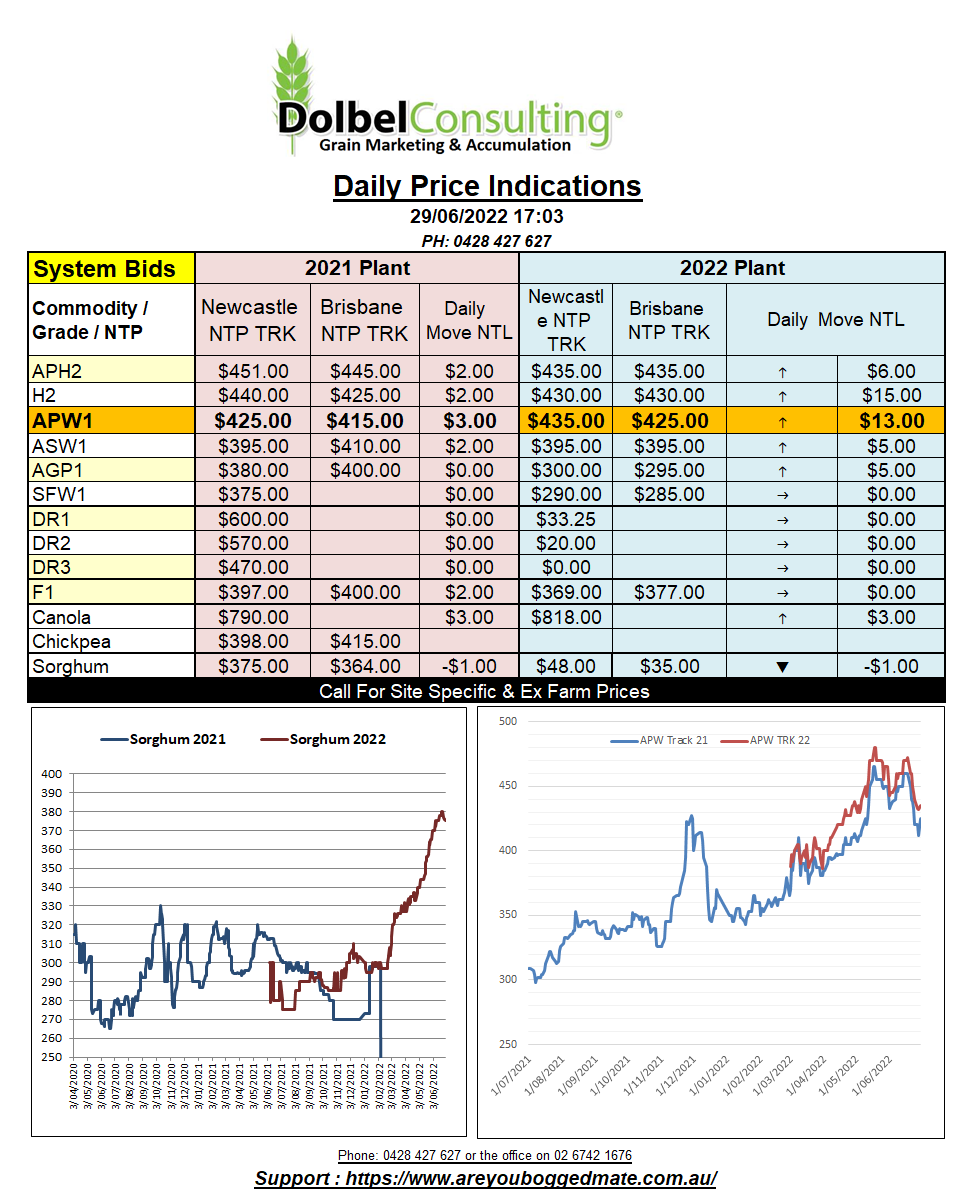

29/6/22 Prices

There was a bit of a bounce in US corn, soybeans and winter wheat futures at Chicago last night. The push higher in soybeans appeared to help the new crop canola contract at Winnipeg gain some ground as well. Paris rapeseed wasn’t left out of the equation, new crop gaining five euros by the close.

The financial markets are all talking about the Russian bond payment default. The “claytons” default, you know, the default you have when you’re not having a default. I guess it’s a bit hard to pay your bond holders when sanctions stop you from paying your bond holders. It’s not like they are broke. At the end of the day the sanctions have prevented a lot of imports while they have still been exporting, a lot of money in and not a lot of money out. Thus the rouble has actually improved against the US dollar.

In order to officially default 25% of the bond holders need to claim they have defaulted. If 50% of the bond holders don’t agree with this and decide to just wait it out the default in void. Well that’s how I read it anyway. So who losses in this instance, the fund managers or governments with Russian bonds, I doubt it, probably more likely larger businesses that had invested in Russian bonds, time will tell.

Bargain hunters were in the wheat pit, the recent falls finally tempting the punters back into the futures market at Chicago. MGEX, lacking the liquidity of Chicago failed to gain the attention of the punter and, as MGEX often does, tracked a more fundamental path, the path of least resistance at present, lower. With 8% of the spring wheat crop now in head, versus the 34% 5yr avg, one might consider spring wheat a better fundamental buy than winter wheat. Yields in winter wheat continue to be mixed in the US but there are many reports now of “better than expected” yields.