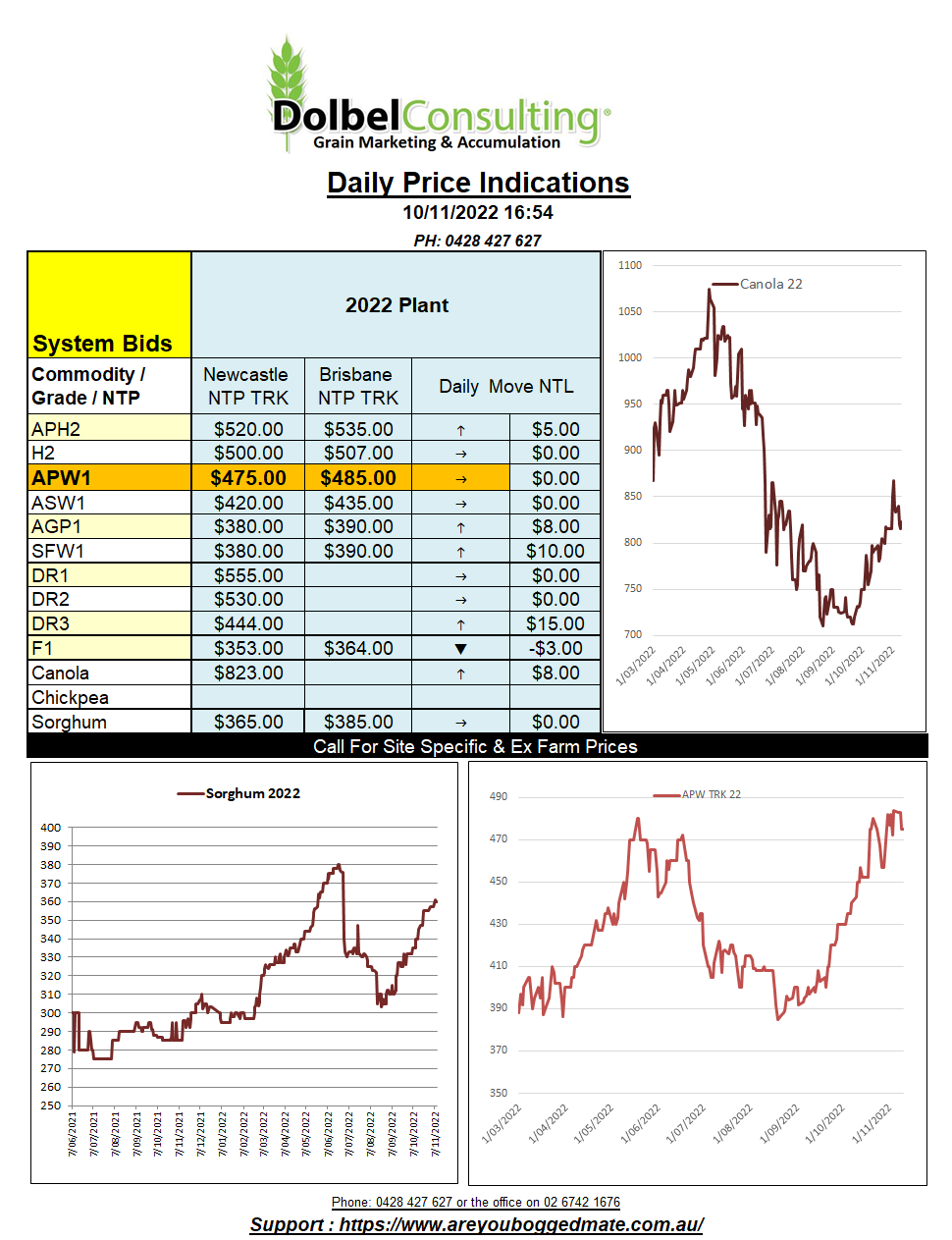

10/11/22 Prices

The USDA WASDE report for November lived up to expectations for wheat, not much to it really. Both carry in and production was increased, imports were reduced, and domestic consumption was increased resulting in a slight increase in carry out of 280kt, to 267.82mt, still to higher for current values.

Looking through the WASDE regional projections we find a few less than believable numbers.

Aussie wheat production stands out. The USDA increased national production by 1.5mt to 34.5mt. Their rock obviously not as mossy as the rocks across eastern Australia. Aussie carry in was left unchanged, and exports were increased by 1mt to 26mt resulting in an increase of 500kt of carry out, now pegged at 3.65mt (probably all feed wheat).

The number is still lower than some private estimates from the trade. Riverina Aust for example currently peg the Aussie crop at 35.29mt. Maybe they can host the USDA staff on a small plane flight from Goondiwindi to Forbes. Local head & grain counts are not as impressive as one would have expected given the season and that’s for the country that hasn’t been flooded. I can’t see east coast data as high as some. I would love to be proved wrong though.

Production estimates for the US, Canada, Russia, Ukraine, China, and India were all unchanged. Argentina was reduced to be more in line with current trade estimates from that region, back 2mt month on month to 15.5mt. The EU saw a reduction too, back 450kt to 134.3mt. Brazil wheat production was increased 200kt to 9.4mt, 300kt was peeled off their import requirements, their carry out was unchanged.

Corn, world ending stock projections were decreased to 300.76mt, Chinese stocks slipping just 100kt. Soybean ending stocks were increased 1.65mt. Interesting to see hardly any variation in world import requirements for soybeans.

Algeria bought 480kt of milling wheat and Philippines are back in tendering for some more feed wheat.