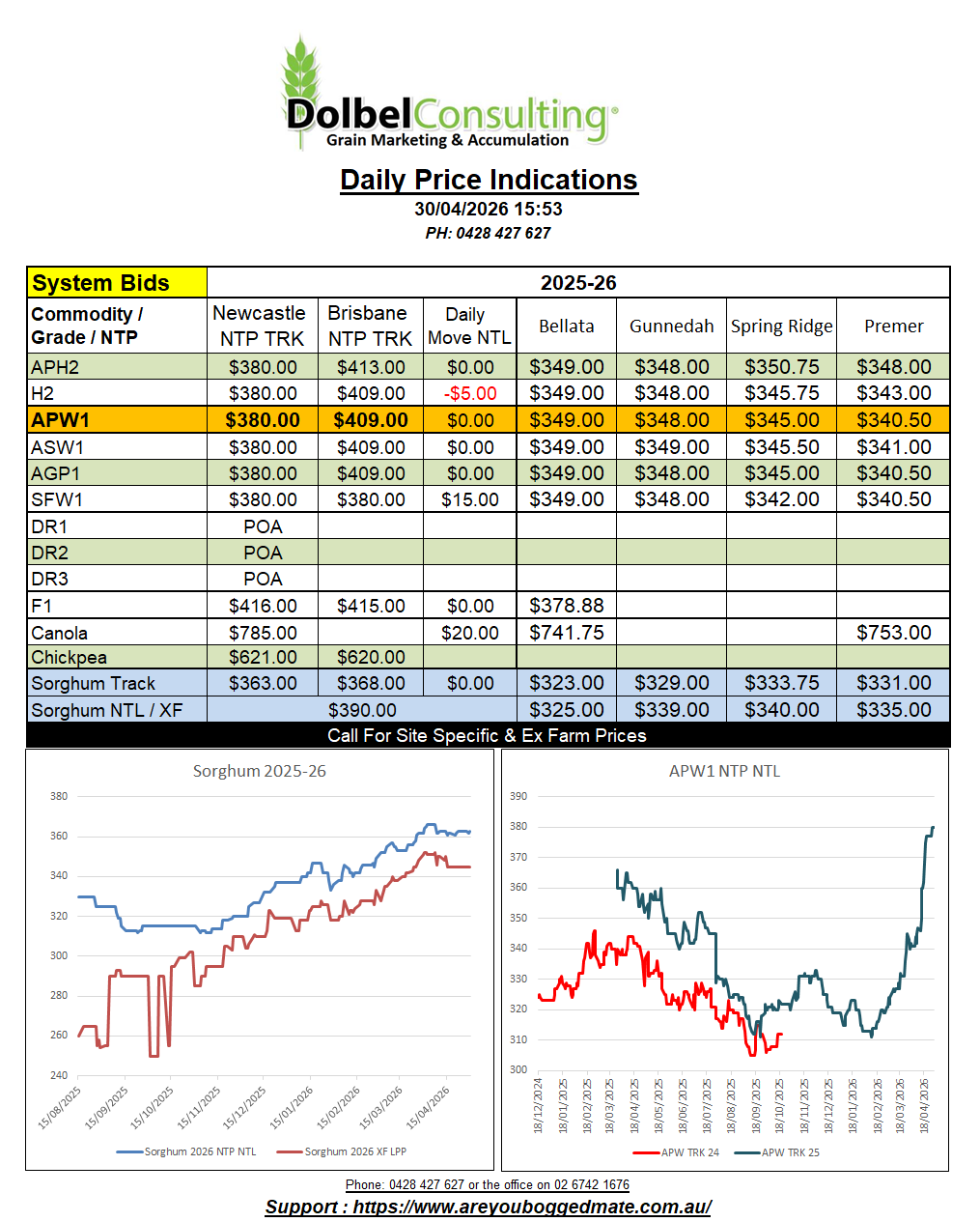

30/4/26 Prices

US hard red winter wheat futures have settled above 700cbu from the July slot through to the May 2028 contract now. Dec26 closed at 736.75c/bu. The last time we saw the nearby close at the Dec level for HRWW was back in late September 2023.

Values had pushed above 700c/bu about 2 years earlier, again due to production fears in the US but mostly due to the Russian / Ukraine war as we moved through early 2022. The rally following the invasion pushing US futures sharply higher in April / May of 2022 when Ukraine suspended wheat exports. Something they were not expected to do, and didn’t do in the 2014 skirmish. It took a while for world wheat prices, and US futures, to stabilise after that, trading at 800 – 900c/bu for much of 2022 and early 2023. Eventually stabilising around 600 to 700c/bu range late 2023 until recently.

HRWW wheat futures tested the downside in mid 2025, falling into the low 500c/bu range as the US harvest began in 2025 and the tariff war picked up. The average nearby futures value for HRWW over the last 5 years is actually about 709c/bu.

Now we have some mid term perspective we can see just how low the base was that we are coming off.

The world has a bunch of wheat according to the USDA, but with yields declining, or likely to decline in India, Europe, USA and Australia, the question is will the two major producers having a good run pick up the difference. I think the answer is mostly yes. Argentina had a huge crop last year, the odds of doing that 2 years in row isn’t huge, but their season is so far very good moisture wise, maybe too good in places. Say Argentine production slips 15% year on year that’s a reduction in production of 4mt+/-. Russian winter wheat is in good shape and spring wheat should also be fine once sown. Lets call Russian production flat. Lets call Canadian production back 10%, there are sowing delays and input cost adjustments to be made. We’ll call US HRWW and spring wheat back 1.86mt, but in all honesty it will probably be more without rain on the HRWW area soon. Australia is likely to be the hardest hit, the year on year production decline could be as much as 9mt or more. Take these adjustment from the majors into account and we see world production at about 820mt.