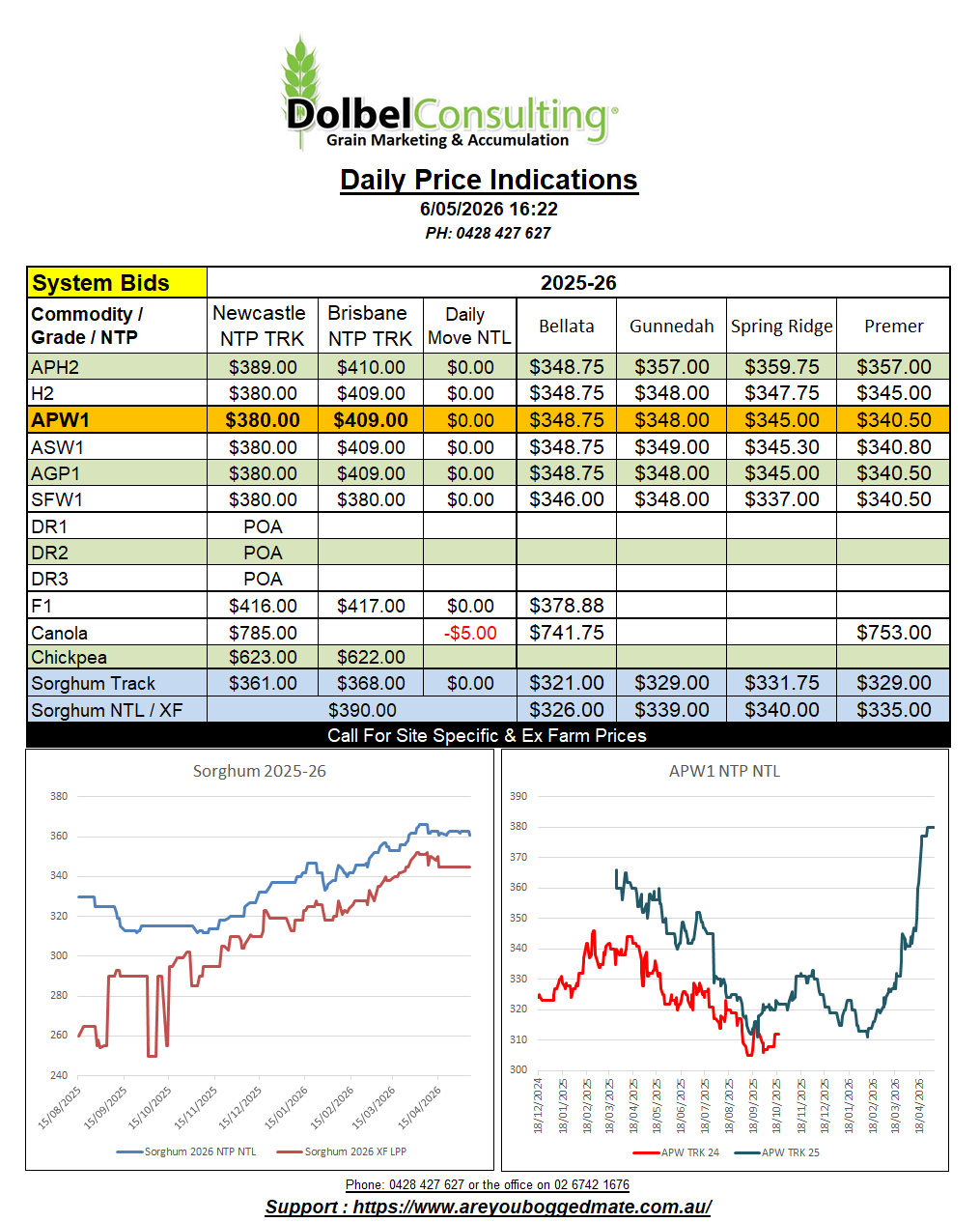

6/5/26 Prices

US and Canadian cash wheat values out of the Pacific Northwest were lower overnight when compared to the previous days conversions to AUD / tonne equivalent. Down roughly AUD$2.00 to AUD$4.00 per tonne, the US product lead global wheat value lower, French, Russian and Argentine values all slipped lower when compared to yesterdays conversions, but none more so than US wheat.

Comparing US, Canadian, Aussie and Argie wheat into the Asian market shows that the US product is still the cheapest milling wheat of that bunch, closely followed by Canadian and then Argentine milling wheat. Aussie wheat is the most expensive, as it has been for some time now, or at least since dry weather has devastated new crop prospects and pasture across much of the east Australian wheat belt in 2025-26.

Conditions are starting to dry out a little across Argentina. The Pampas remains wet, but central and northern Cordoba, and Santa Fe to the east, are drying down a little now after a very wet start to autumn. The 7 day forecast for Argentina is showing a continuation of this, drier to the west and wetter to the east across the Pampas region of BA. Values for both milling wheat and sorghum out of Argentina have moved higher over the last week or two, milling wheat there up roughly AUD$40.00 since late March.

US grain futures have been linked to crude oil by a proxy connection to biofuel through corn and soybean, and by the influence oil has had on general market sentiment. I read a great comment this morning stating that the US is 9 weeks into a 4 week war that they won 8 weeks ago. Does that mean that the last 8 weeks has simply been an exercise in market manipulation and option trading…… Don’t get me started, my tin foil hat has gotten that heavy since 2020 I’m flat out lifting it to put in on these days. Crude oil was higher yesterday, only to shed much of that gain overnight. Palm oil, rapeseed, canola and soybeans are all being caught up in this spillover, this cross over contamination currently muddying the fundamentals for global oilseeds and grains. The bigger picture, at least fundamentally, is still focused on productions issues in the US HRWW belt, dry weather in France (good rain predicted there this week) and eastern Australia.