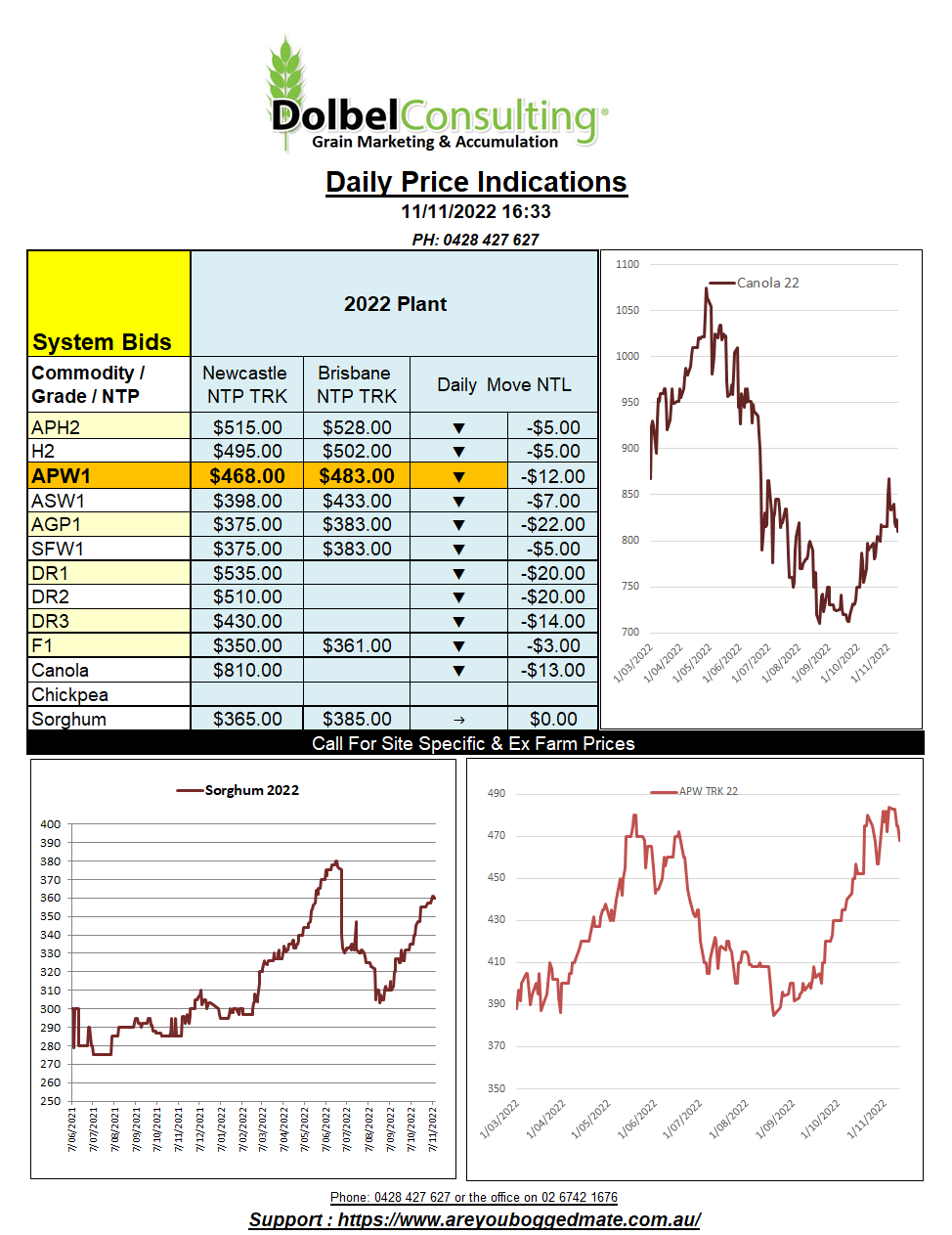

11/11/22 Prices

Officials from Russia, Turkey, Ukraine, and the UN are set to meet at Geneva on Friday to discuss the continuation of the Black Sea grain corridor. Most punters seem to think it’s a done deal. 2022 has not been a great year to assume anything, but one would tend to think it’s more likely to continue given recent outcomes, possibly with a few amendments.

With Russian forces appearing to be moving towards their own border in some locations, it is giving one a sense of an approaching end to this war.

The big mover overnight, apart from the AUD / USD, was Chicago soybeans, down 29c/bu (AUD$16.17) in the Jan23 slot. The weakness also pushing through the meal market. US weekly soybean export sales were within trade expectation, maybe a little lower than expected, but at 795kt did not include this week’s 927kt of sales announcements to China. One may feel this move lower might be overcooked fundamentally.

Year on year US soybean sales volume is almost identical to last year. Most predictions have China increasing their crush rate by 3mtpa but it may take some kind of retraction in their Covid policy to see a marked improvement in sentiment regarding Chinese demand.

The weaker USD should have helped US grain futures higher last night. It seems the punters who are short futures continue to rule that roost.

Algeria booked 510kt of wheat at US$368 CFR. Saudi Arabia are in for 595kt of 12.5% milling wheat. Egypt are in, out, in….. but have received 75kt of Russian wheat booked through private traders this week. Tunisia are in for wheat, barley and durum for Dec / Jan.

US wheat futures were lower. US sales volume still lacklustre but ahead of this time last year. US physical export prices are still too high.