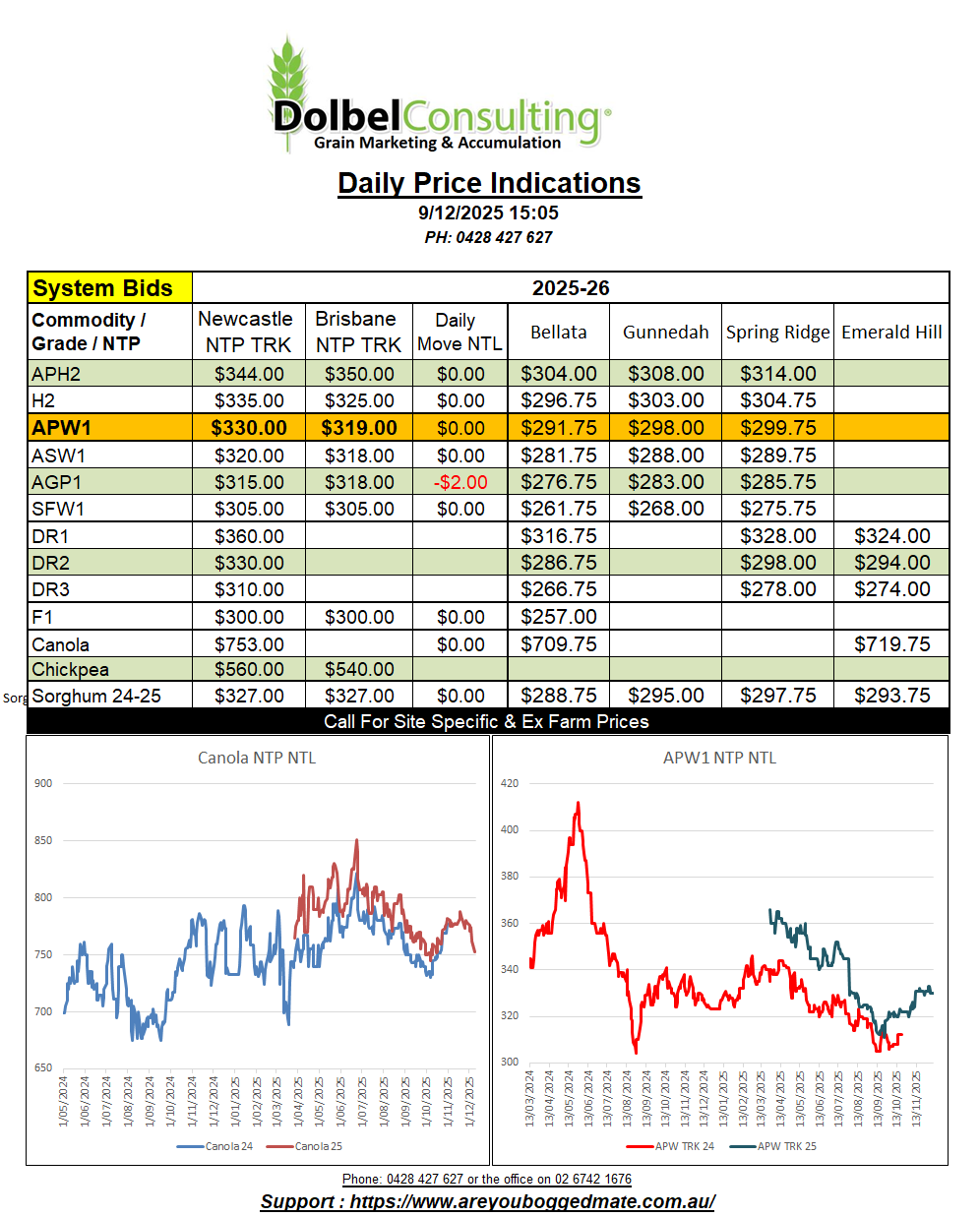

9/12/25 Prices

Delhi mandi chickpea values are at the Minimum Support Price this morning, closing the day trade at 5650Rs/Q. I’m interpreting this as not great news. Historically if the Indian market manages to trade below MSP it is seen as a time that the Indian government may need to step in to support local prices or run the risk of buying a larger than required slice of their production.

I guess it’s a bit like the government liking the idea of an underwritten pool, but once that underwriting is triggered it become more of a financial policy than a publicity policy. In the case of chickpeas we also have a slightly higher MSP for the next crop.

Local prices for chickpeas remain well below the converted Delhi equivalent AUD/t packer price here. The above probably is a good enough reason to sustain that discount. Indian import tariffs are generally implemented to crush the prospects of imports not just impede them a little.

Local chickpeas were bid at $610 delivered Graincorp Newcastle for December yesterday. That is giving the LPP grower a price of $570 XF, a fair bid given the recent values seen at NNSW packers.

Overnight international cash and futures have proven to be a little directionless. Paris rapeseed futures closed higher while Winnipeg canola futures continued to be weighed down by the weaker soybean futures at Chicago. The later struggling between will or won’t China buy enough US soybeans to meet their agreement with the States. Paris milling wheat contracts are weaker in the December slots rolling to March / May, and stronger in the March / May slots. All three US red wheat grades closed lower, HRWW the worst performer.

Argie milling wheat bounced off Fridays low, the day to day conversion gaining roughly AUD$5.50/t, possibly taking some of the pressure off Aussie H2 values today. US weekly export inspections for wheat came in at 393kt, towards the higher side of trade guesses prior. US export inspection @ 13.634mt, +21% y/y.