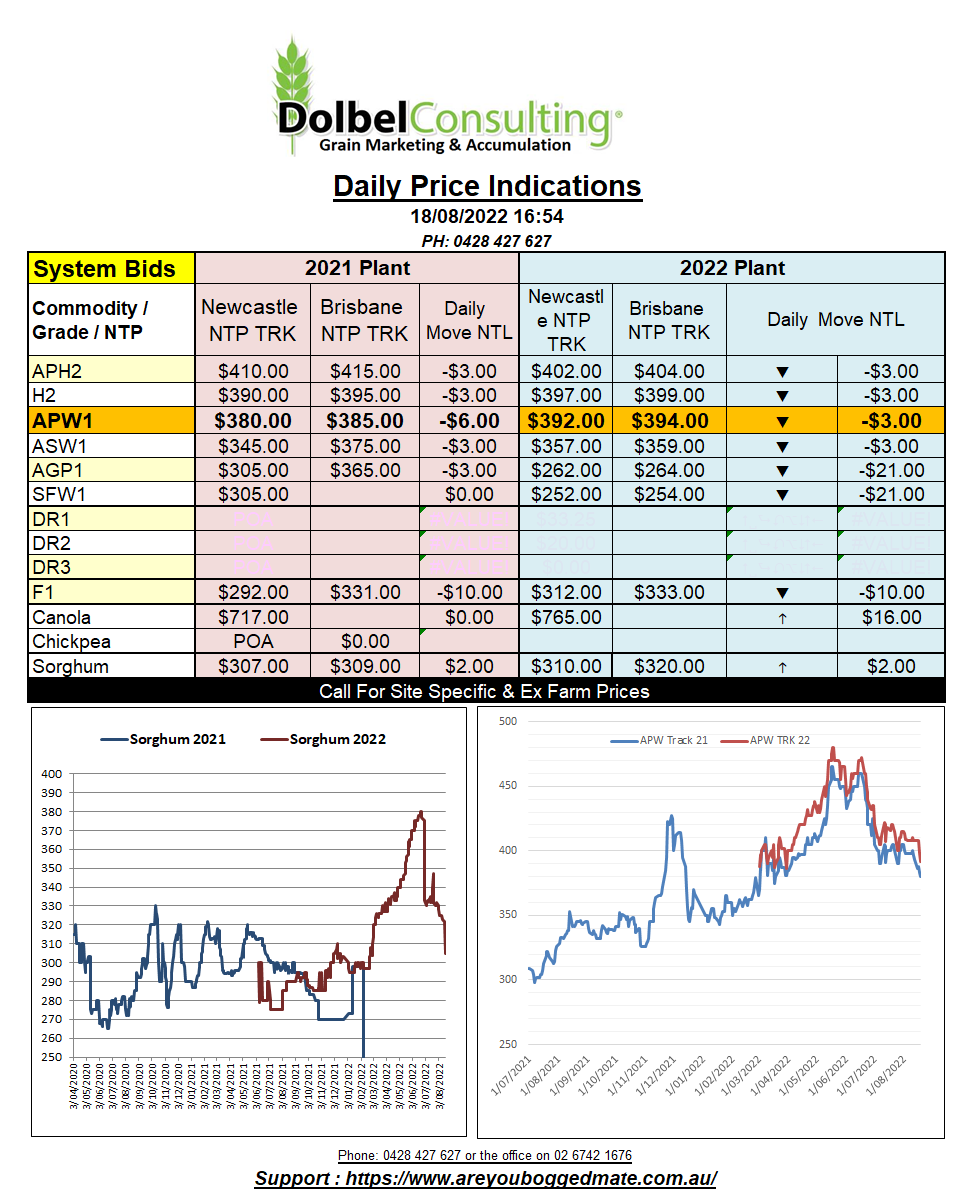

18/8/22 Prices

The bargain hunters were in the corn and soybean pits at Chicago after sharp losses to both earlier in the week pushed prices to technical support levels. In the US corn / bean basis was pretty flat, cash bids reflecting the higher close in futures. Wheat futures in the US did not share the same […]