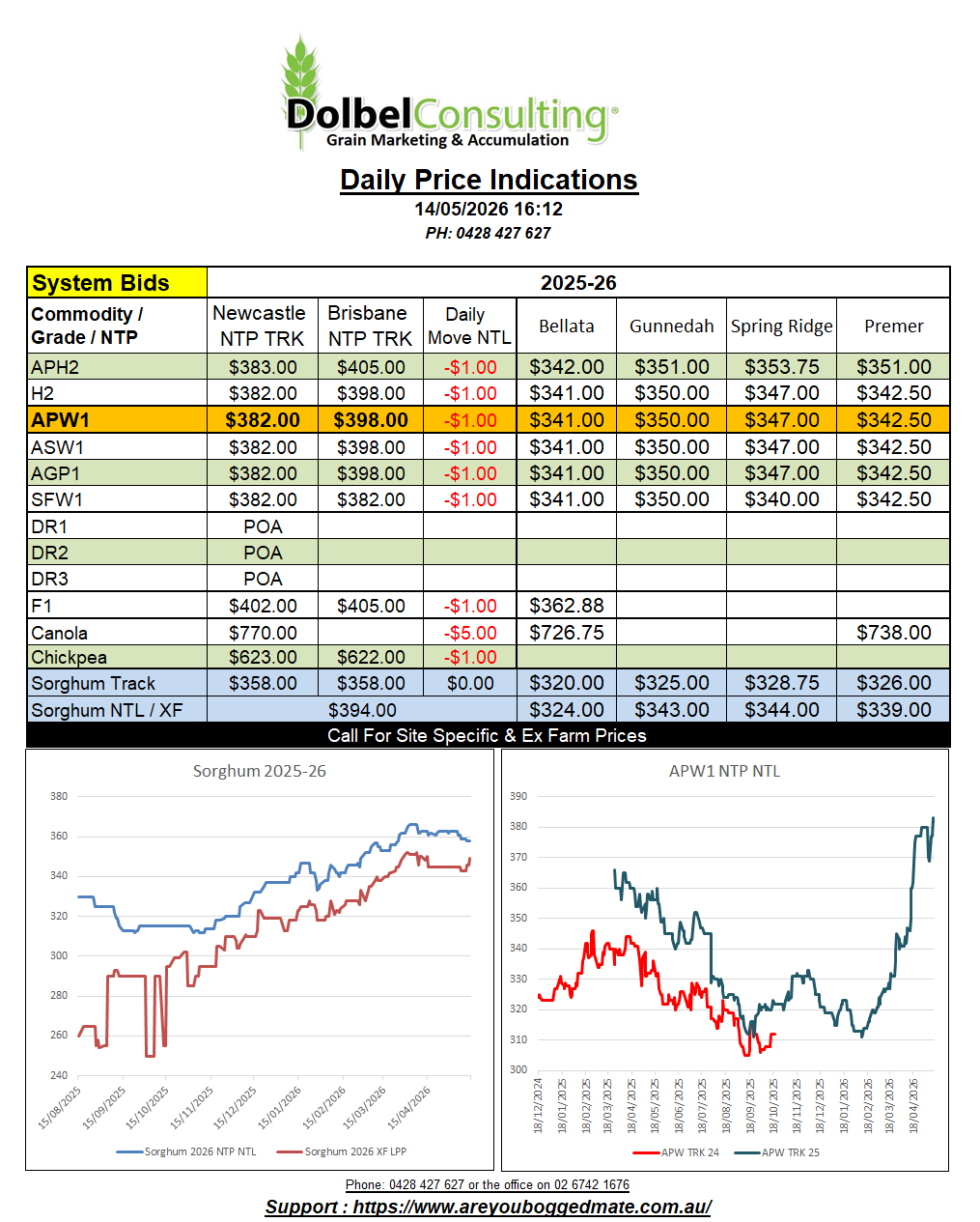

14/5/26 Prices

US grains tried to hold onto the recent rally at Chicago. Corn and soybeans succeeded, but all three major wheat grades gave back some gains. There was talk December futures for hard red winter wheat were going to test 800c/bu, but closed the session at 750c/bu.

The US 2026-27 wheat production estimate in the WASDE took the punters by surprise. Analyst have now had time to absorb and attempt to proof some of the data from international producers, and the consensus is that some of the estimates may be close, and some may be utter rubbish. Sounds like a normal WASDE report to me.

There are a number of things at play this week that could push US wheat futures one way or the other. The most important now that the WASDE is behind us is the results from the US Wheat Associates Hard Red Winter Wheat Crop Tour. Twitter, sorry, X.com, seems to be the place to follow the progress of the participants as they cruise through Kansas taking field samples and posting their reports often. It’s actually very interesting. The hard finish is seeing an increase in disease, frost damage and drought stress, resulting in sharply lower yields in many fields.

Day one results are in with the average yield from 187 stops calculated at 38.3b/ac, or for us living without the assistance of bib and brace overalls, 2.57t/ha. Last year results were closer to 50.5bu/ac, or 3.4t/ha, a decline of 24.4%. Better than the 100% decline many here are currently expecting. The worst hit area appears to be the NW, closer to Nebraska, but results from central, and even north east Kansas, were not encouraging on day one .

Russian milling wheat values are mixed. Port bids were said to have slipped a little but it became evident the trade had to bid up to acquire tonnage. Currently we see milling wheat FOB Black Sea at roughly US$235.25, the same as Ukraine wheat. Black Sea panamax rates to Asia are roughly US$59 for Russian and US$64.00 for Ukrainian bulk wheat.