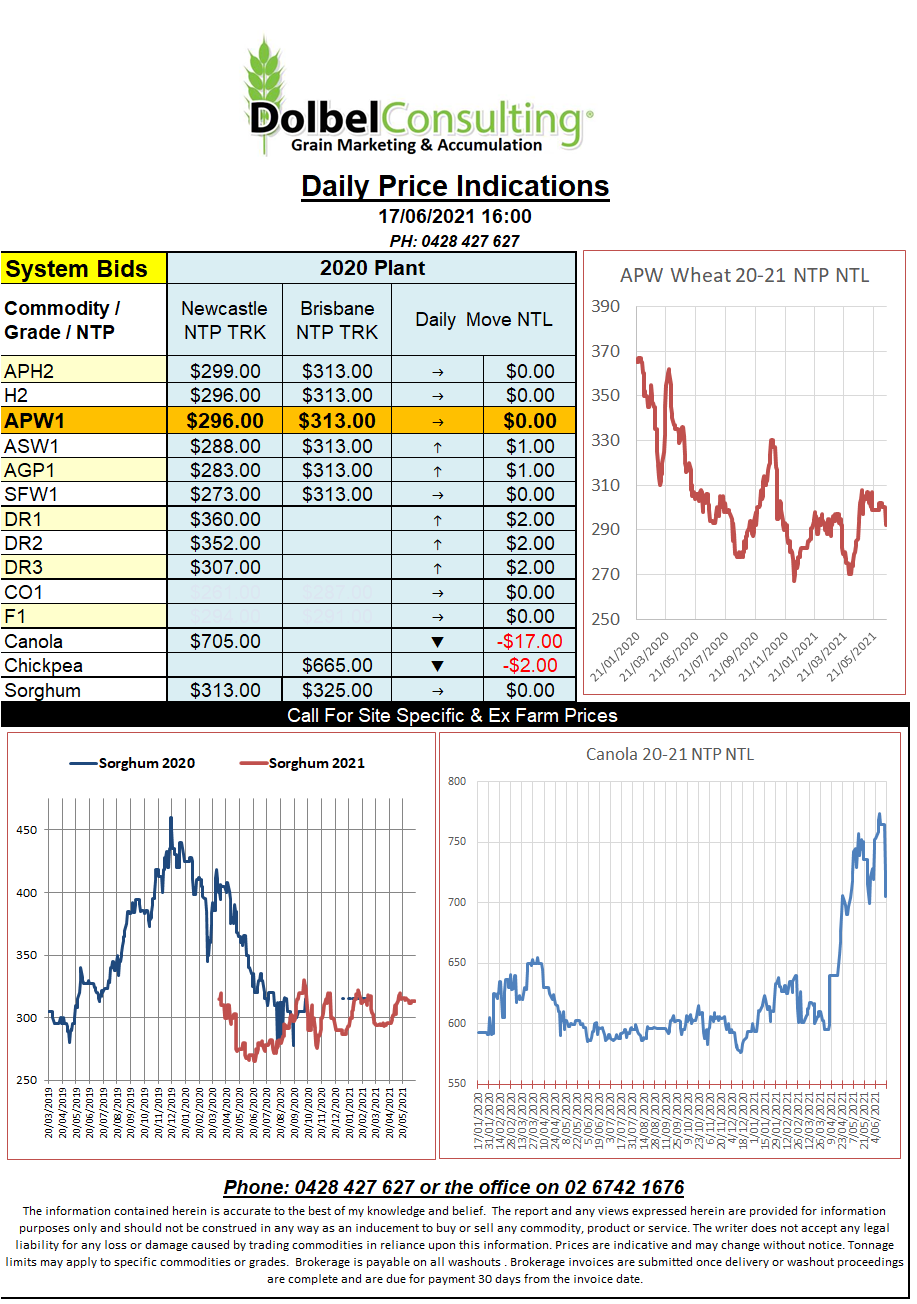

17/6/21 Prices

Chicago soybeans were once again sold off. Technical support is likely to start creeping in soon but the punters live by the saying “the trend is your friend” and at present that trend is down. The weakness spilled into both Paris and Winnipeg oilseeds with canola and rape both pushing sharply lower. Soy oil futures slipped 5%. News that Brazilian soybean exports will increase week on week didn’t help.

The 1 – 7 day rainfall model for the US soybean belt is generally pretty good, possibly a little too wet in the lower Mississippi (cotton guys keep an eye on this). More good falls are predicted for the central corn belt and even another 20-30mm for central N.Dakota. SE Saskatchewan is also expected to see another 25-40mm but a large slice of the Prairies towards central and western Sask is expected to see just trace falls. This may slow the decline in canola futures but there is a lot of momentum in this sell off at present.

Spring wheat was a winner in last night’s US session. The stronger futures market was reflected in the cash market with cash bids across SE Saskatchewan moving around C$4.00 higher for the new crop. At C$302 ex farm SE Sask a back of an envelope conversion would see this equivalent to an AUD$370 port number. Comparing SE Sask values to US DNS wheat out of the PNW we see 14% for a Sept lift equivalent to about AUD$378 if using Japan as a home. Local cash bids for new crop APH1 were closer to AUD$320 port. At this discount to US / Canadian spring wheat and considering our frieght advantage into SE Asia new crop Aussie values are cheap, very cheap.

Club white and soft white wheat values out of the US PNW were unchanged.