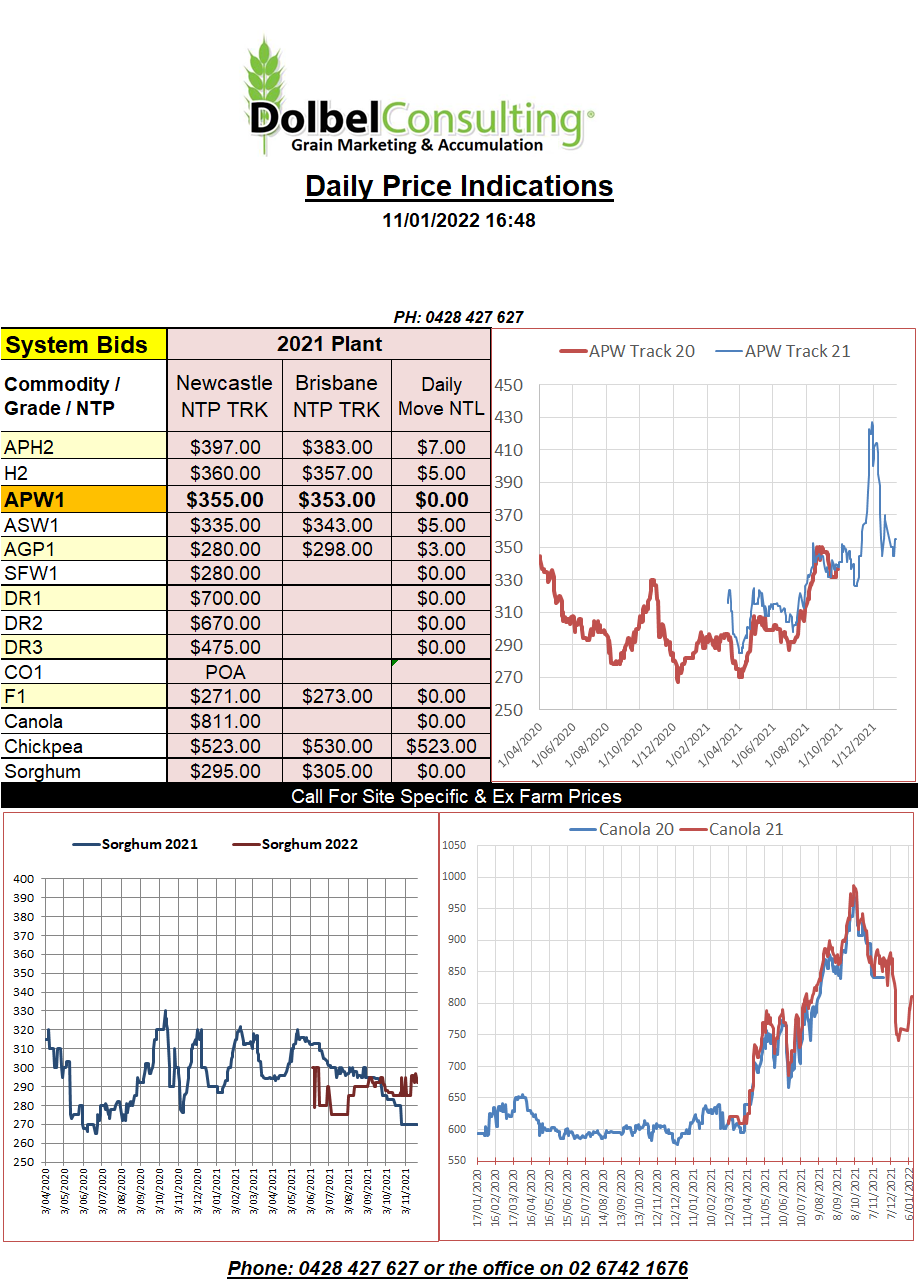

11/1/22 Prices

In the USA we see Chicago soft and hard wheat futures a tad firmer while we see MGEX spring wheat futures continue to slip away, converging with new crop values. Cash bids for spring wheat out of the PNW were flat. Canadian values mixed but generally slipping lower, in line with Minneapolis numbers, late in the day.

Cash canola across SE Saskatchewan was lower, following the weaker Chicago soybeans futures market. Cash bids out of SE Sask were mixed but generally fell away by about C$6.00 to C$8.00 per tonne. Across the Atlantic Paris rapeseed futures were also sharply lower, shedding E19.25 / tonne on the nearby February contract. Paris futures had jumped sharply during the second half of last week, crushing local basis here as the trade were again unwilling to follow futures markets higher dollar for dollar at the local level.

Much of the jostling in US futures this week will be put down to positioning prior to the USDA World Ag Supply & Demand Estimate report due out on the 12th, US time, so Thursday morning here. The punters are expecting higher US wheat stocks after prices pruned export demand. Possible reductions are also pencilled in for S.American soybean and corn crops. So this report could send mixed messages for those marketing feed grain into 2022. Lower corn production in S.America could be viewed as potentially bullish while higher wheat ending stocks could be viewed as potentially bearish but this will be grade dependant. Obviously this quarter the higher grades will continue to sustain a much better margin than usual but mid grades may suffer while feed grades may possibly be supported by lower corn production.