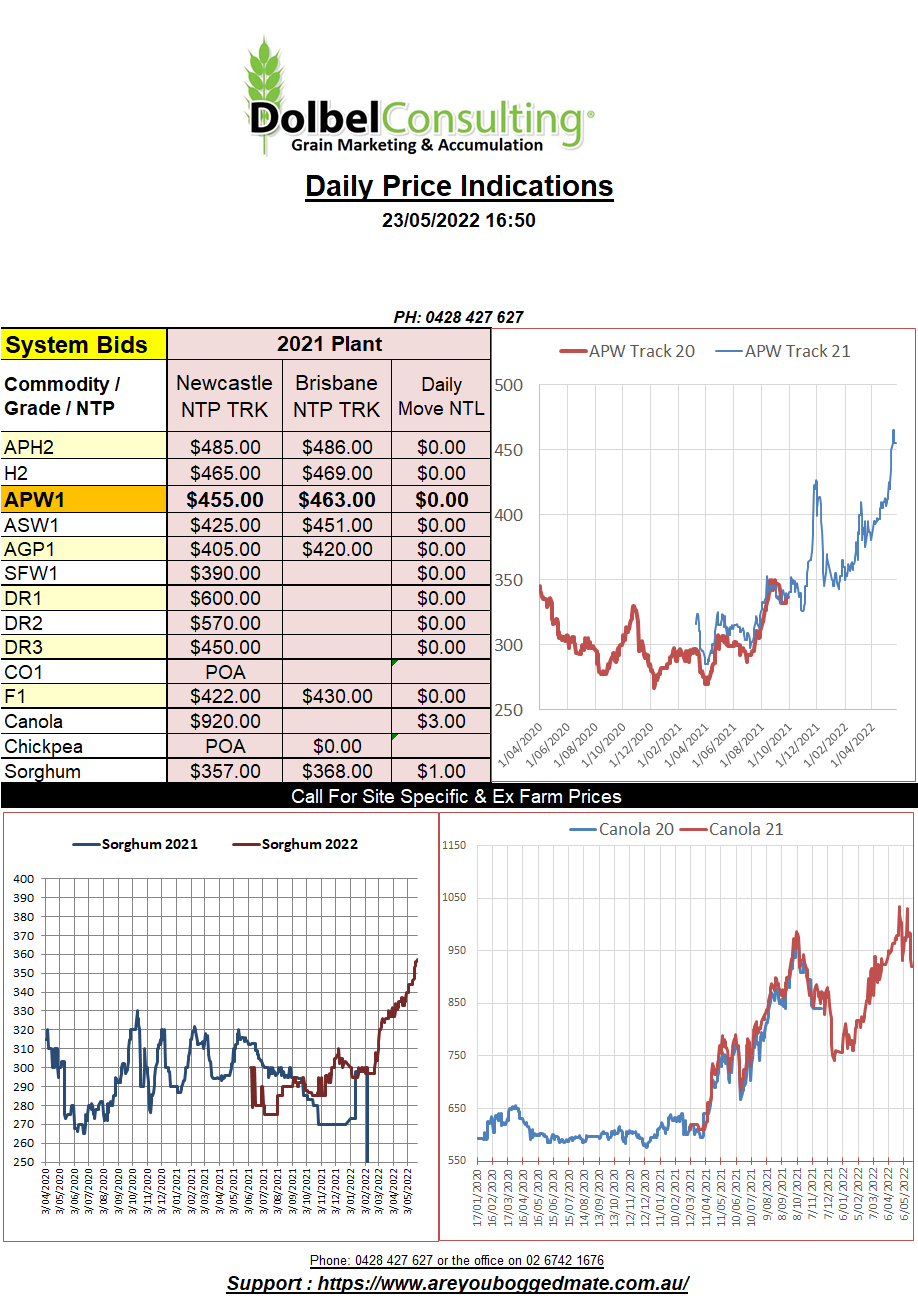

23/5/22 Prices

Wheat futures at Chicago and Minneapolis were sharply lower for the 3rd session in a row. Profit taking was said to be the major influence in price direction but at these levels demand destruction can’t be overlooked.

For instance, spring wheat out of the Pacific North West was priced close to US$510 FOB. That wheat landed in Japan would cost a buyer somewhere around US$548 at the port. Looking at white wheat out of the US PNW, that product would land in Japan for something close to US$476 FOB. A comparable product from Australia could land there for a number closer to US$400.

Comparing apples with apples, i.e. white wheat with white wheat, you can see that US product is still attracting a substantial premium, probably domestically driven from last year’s drought in the PNW, but still a premium over the Australian product. Which readily available from either east or west coast ports. For the sake of the exercise that difference in Australian value and PNW value for 10.5% white wheat is about 206c/bu.

Most analyst would argue that the fundamentals supporting wheat have changed little week on week. Black Sea volume remains well back on average. Although we did see some new crop wheat estimates for Russia come out a little higher than expected.

The Kansas wheat tour confirmed what everyone basically new. Wheat west of Wichita Kansas is doing it tough and abandonment could be at least double the average for west Kansas producers. US and Canadian spring wheat sowing isn’t progressing at the pace they would like to see. The seven-day map for Saskatchewan actually reversing, now predicting little to no rain for the next 7 days after some useful falls across SE Sask this last week. In Europe both France and Germany remain drier than average. The SE of France now showing as little as 20-40% of avg rainfall for the last 14 days.