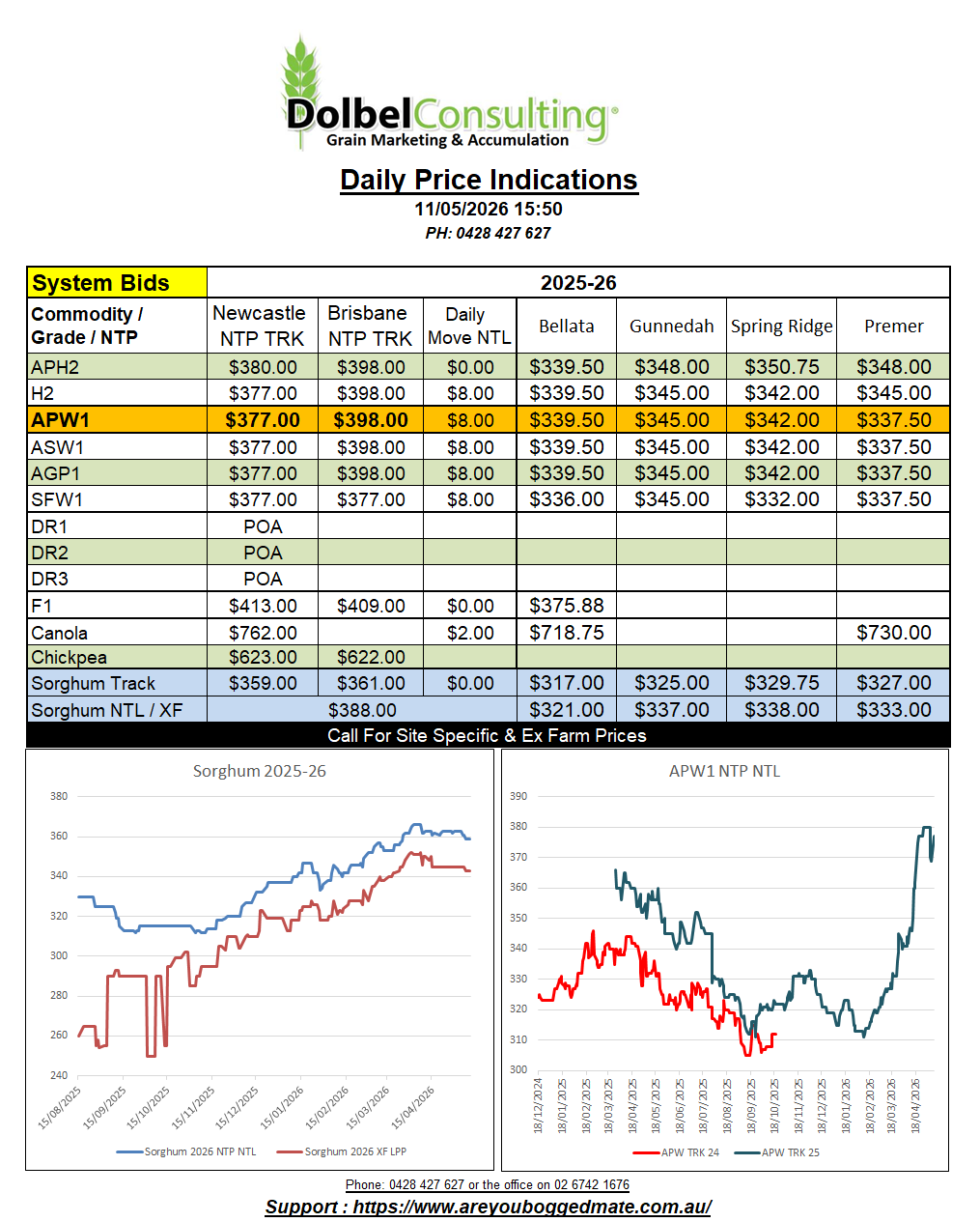

11/5/26 Prices

Algeria picked up approximately 390kt to 420kt of soft wheat during the week. Numbers are estimates for price and volume, due to Algeria not actually confirming their trade data. The trade had expected to see volume closer to 650kt, so 420kt was a little bearish to the market. Prices were estimated to have been around US$268 to US$270 C&F. This would see either EU or Black Sea wheat working into the tender. Russian milling wheat has been indicated at US$234 FOB over the last week or so, leaving US$34 in the pot to cover logistics and margin, lean but probably just enough.

US grain futures closed in the green, corn, wheat and soybeans all posting gains. US beans were strong, up 17.25c/bu nearby and +16c/bu in the Jan27 slot. Strength in Chicago soybeans spilled over into Canadian canola values. Both Winnipeg canola futures and cash prices for ex farm SE Sask canola putting on nice grains overnight. Paris rapeseed futures were less volatile, closing higher but only up E0.75/t in the Feb27 slot. Palm oil was not in the ball park, playing it’s own losing game in the car park, falling AUD$12.31/t by the close. WTI crude oil futures were up just US$0.61/b nearby, Brent up US$1.23/b in the July slot, possibly indicating there are other factors at play with Canadian canola and US soybeans.

Brazil exported a record 16.75mt of soybeans in April, a year on year increase of 9.7%. China is the obvious destination for the majority, 69%, the EU taking 8% and Turkey 4%. April / May is usually when Brazilian soybean exports peak, tapering off for the rest of the year. China potentially picking up more US beans from the second half of the year.

The funds continue to show more of an interest in US HRWW futures over SRWW, increasing their net long for the week ended the 5th of May. This does reflect the condition of each type of wheat in the US at present. SRWW having a good run and HRWW slowly falling apart due to drought and cold weather.