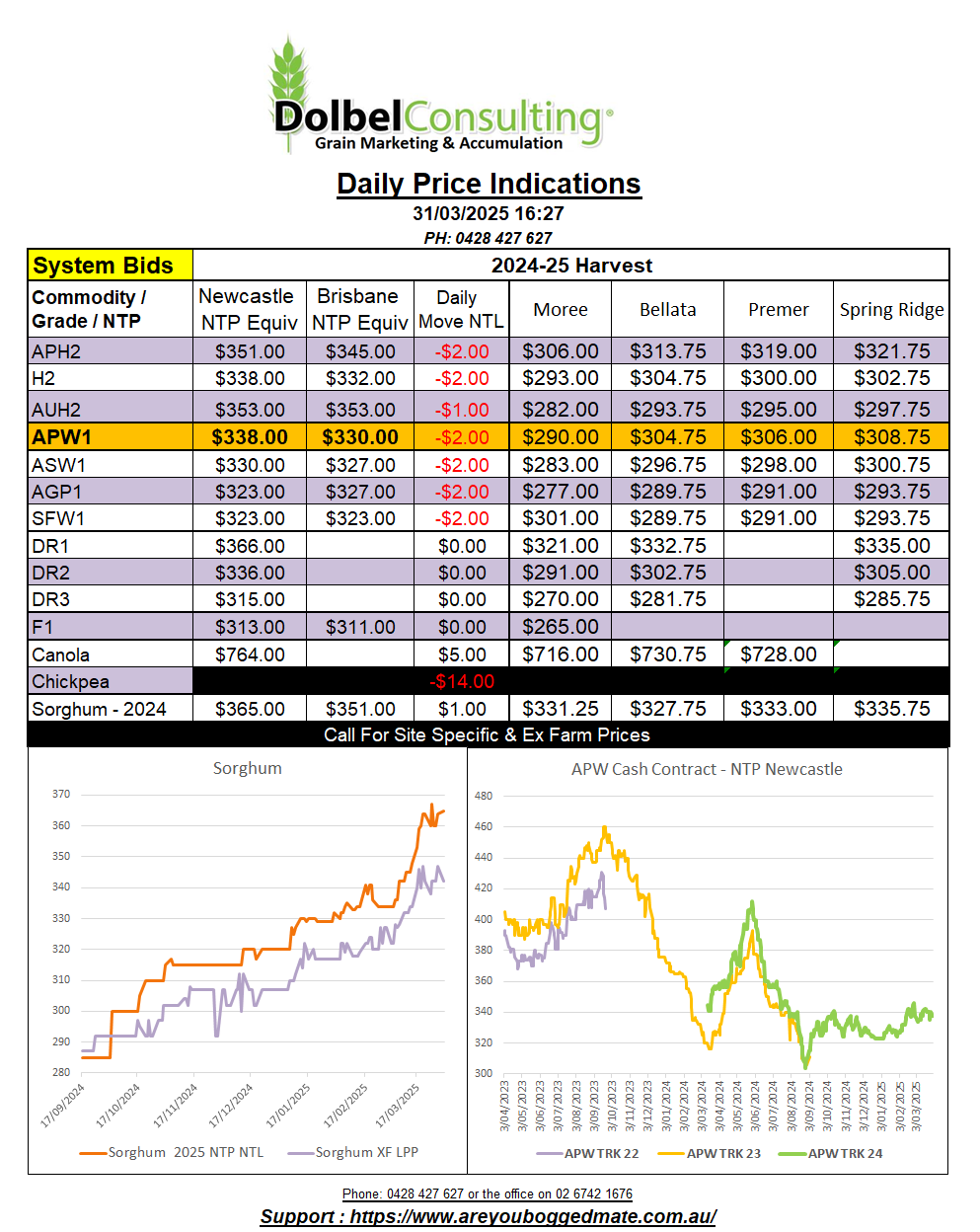

31/3/25 Prices

The oilseeds are the only ray of light in the futures markets this morning. Chicago soybeans closed 6.25c/bu higher nearby and +8c/bu (AUD$4.67/t) in the Sept slot. The strength was across all the oilseeds. Paris rapeseed, Winnipeg canola and palm oil all closed higher. Palm oil impressively so, up 100RM/t, about AUD$35.86 / tonne.

It’s a little perplexing to see so much weakness in US wheat futures. To a degree soft red winter wheat is understandable. The US rainfall model is showing the chance of 30 – 60mm of rain across much of the SRWW states in the US over the next 7 days. This isn’t the case for the bulk of the hard red winter wheat states though. Much of Kansas, the USA No1 wheat producing state, continues to remain very dry and much of the next 7 days forecast for rain is expected to pass to the north and east of Kansas and Oklahoma. A quick look at the US drought monitor and the current weather forecast, is all you need to see to start to question the current sell down in HRWW futures. It’s nothing new for the US futures market to trade opposing views to the fundamentals though.

World cash wheat values were mixed. US values out of the PNW reflected the push lower in futures. The day to day conversion comparison for HRWW was back AUD$7.00 / t. While the US PNW spring wheat conversion comparison was back AUD$3.00 the Canadian conversion was not. CWRS13.5 shed value in C$ / tonne but in the AUD conversion it actually gained a couple of bucks. French milling wheat was also a little higher compared to yesterdays conversion.

International sorghum values were lower. Argie values compared to yesterdays conversion to C&F China and then back to an equivalent price Australia are back AUD$7.61 / tonne. This fall roughly converts Argie sorghum to the same value as we are seeing locally. US values were lower, the day to day conversion comparison for Corpus Christi and FOB NOLA are both lower, shedding roughly AUD$4.00 / tonne. The Chinese index fell a comparable amount.