13/4/26 Prices

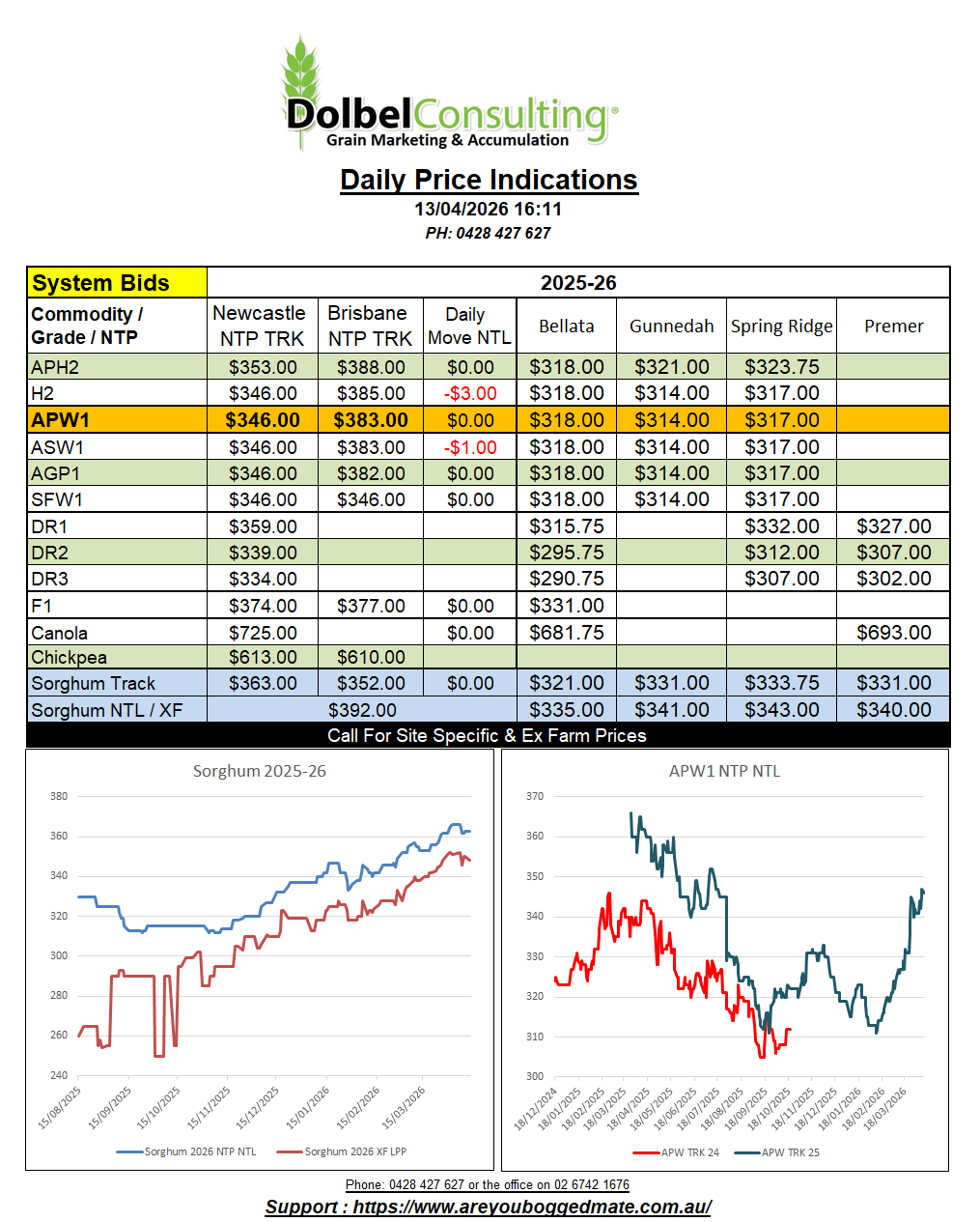

US futures markets continued to focus on ample world and US wheat stocks overnight. Flat to softer wheat futures at Chicago and Minneapolis continues to weight on FOB offers out of the Pacific Northwest, resulting in lower prices for export wheat from both the US and Canada into the Asian markets. The comparison for H2 versus US HRWW into NW Asia now indicates that the US product is some US$23.00 cheaper than Aussie wheat. Not a bad effort from the USA considering Aussie wheat was briefly cheaper no more than 10 days ago.

This emphasises two thing to the international market. Firstly the obvious, how cheap US wheat is, but secondly just how dry the conditions have become across much of NSW and S-QLD, the main premium wheat producing regions of eastern Australia. Domestic markets there are now paying a massive premium over export parity to keep local stocks local.

Soyoil / meal continues to be the golden child in the US futures pit. Managed money now holding the longest long position they have held in these by products in many years. Sales volume of both soybean oil and meal remain solid out of the US. But it’s not only the US enjoying the vegie oil side of the market. Brazil is toying with the idea of increasing the ethanol mix in gasoline to 32% (currently 30%, up from 27% in August last year) by the end of June.

Not to be excluded, this may also have an impact on corn as feed stock demand increases. Very timely too as Argentina confirm a record corn harvest for 2025-26 and the US see projected corn planting for 2026 at somewhere around 94 million acres. Not a US record, but still a substantial area from a historical perspective.

The war in Iran, or more so the delay in ocean traffic out of the region has seen numerous knock on affects to what many might not of assumed were related markets. Take cotton for instance, less oil = less synthetics, less synthetics = higher demand for cotton, will cotton prices go up more.